[UMG, WMG] record labels and the music industry: opportunities and challenges

Posted By

scuttleblurb

On

In

SAMPLE POSTS,[SPOT] Spotify,[UMG] Universal Music,[WMG] Warner Music |

1 Comment

I.

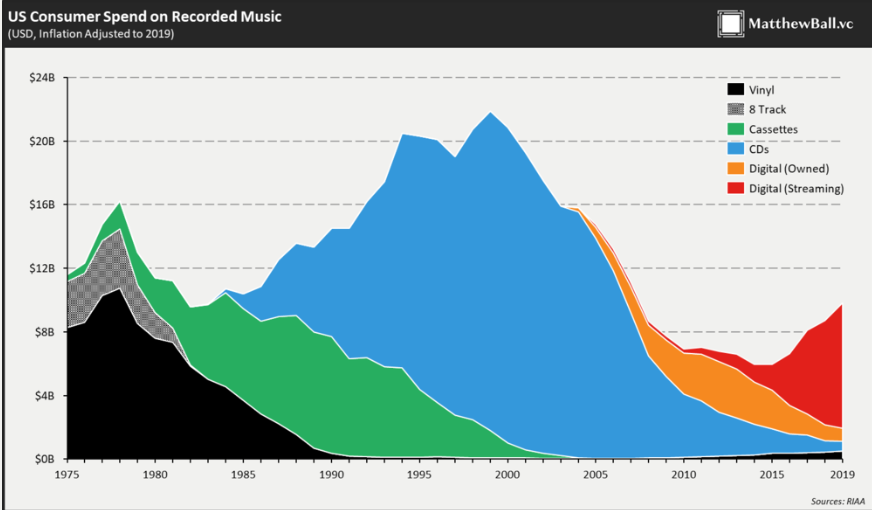

Every few years, this graphic from the Recording Industry Association of America (RIAA), reproduced by Matthew Ball, makes the rounds:

It shows how a 15-year decline in recorded music revenue, precipitated by the cannibalistic effect of free downloads, is being reversed by the rise of subscription fees from digital streaming providers (DSPs). As I detailed in my Spotify/Sirius post[1] from 3 years ago:

See that peak in the chart of recorded music sales below? That’s what it looks like when an oligopoly controls the point of scarcity and bundles tracks together in an album, forcing consumers to pay for the songs they don’t want in order to get the songs that they do. This gave way to a period where tracks were disaggregated from CDs, encoded into mp3’s, and distributed for free on file sharing services like Napster. Given how profitable CD albums were, you will not be surprised to learn that the labels summarily rejected the opportunity to license copy-resistant mp3 technology years before Napster was launched (and then they later refused to partner with Napster). And you’ll notice in the above exhibit that during the 2-to-3 year period after Napster launched but before the ubiquity of portable players allowed consumers to carry mp3s with them, Napster may have actually facilitated discovery and boosted CD sales. But the portable players caught up and the labels, whose production and distribution efficiencies were constrained by the limits of the physical world, proved no match for the network effects and the zero marginal distribution costs of Napster’s P2P model.

Harrowing declines in album sales finally forced the record labels to unbundle CDs. Through iTunes, they offered individual tracks, which hewed more closely to consumer needs than albums but still did not capture variations in a song’s long-term appeal since every track was priced at 99c regardless of how many times it was subsequently played. Per-stream pricing, where the artist/label is paid every time her song is played, is now supplanting owned tracks. Each transition, from album to owned track to streaming, more closely aligns payment with song popularity.

By consolidating and curating the world’s music, Spotify did what record label lawyers and the US court system never could: they made music worth paying for again. For a growing number of consumers, subscribing to Spotify for ~$10/month provided more value than pirating tracks for free. A minor contribution 10 years ago, digital – which includes payments from DSPs like Spotify as well as emerging platforms like TikTok and Roblox – now accounts for between ~60% and 70% of Universal, Sony, and Warner’s recorded music revenue.

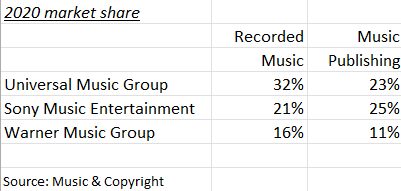

But while the way music is consumed has transformed over the last 10 years, industry profits are still largely captured by the big 3, who following their acquisitions of Polygram, BMG, and EMI, now command nearly 70% and 60% of recorded music and music publishing revenue, respectively:

The incumbents may trade a few points of share from one year to next depending on which artist is topping the charts. Also, independent labels are chipping away at the periphery (more on this). But for the most part the industry operates as a stable oligopoly.

II.

Every music recording carries two separate ownership rights: one covering an artist’s original recording (“Masters”) which falls under the labels’ recorded music segment; the other protecting the songwriting (lyrics and musical composition), which falls under publishing.

The recorded music segment, which comprises around 83% of Universal and Warner’s profits, is in the business of discovering and signing artists who they hope will grow into mega stars like Drake and Taylor Swift. They front capital (”advances”) to promising artists and remit anywhere between 15% and 25%+ of revenue (”royalties”)1[2] to them, with the high end of that range reserved for stars with bargaining power. Royalties are recoupable, meaning that they are paid to the artist only after the record company has recouped its advance.

Just making up numbers here, let’s say Spotify does $1bn of subscription revenue this month. Around 52% of that ($520mn) goes to a royalty pot reserved for Masters rightsholders (the record labels). Assuming Universal accounts for 30% of Spotify streams2[3], they are entitled to 30% of the pot (30% x $520mn = $156mn)3[4].

A top-tier artist who makes up, say, 5% of Universal’s steams on Spotify, will have $7.8mn (5% x $156mn) allocated to its Masters. At a 20% royalty rate, the artist earns $1.6mn (20% x $7.8mn). For CDs and digital downloads, the 20% royalty is applied to the wholesale price of every album sold, so if 200k CDs are sold at a wholesale price of $7, the artist will earn $280k (20% x $7 x 200k). Artists also share in the payments Universal gets for songs played by non-interactive streaming programmers (like Pandora and iHeart Radio, who choose the songs their user hears) and satellite radio providers (Sirius XM) – where rates are set by law and royalties are collected and paid by SoundExchange, a non-profit rights management organization – not to mention TV shows, commercials, motion pictures, and “emerging” platforms like TikTok, YouTube, Roblox, Peloton, etc., which we’ll ignore here4[5].

The artist doesn’t actually receive any of the royalties she earns until Universal has recouped not only its advance but also the cost of recording, ad campaigns, tour equipment, etc., some of which can be negotiated depending on the importance of the artist (most recording contracts today are structured as “funds”, where the artist receives an advance plus a fixed sum to cover recording costs). So assuming a $3mn advance, the artist will still be unrecouped by $1.2mn ($3mn – $280k – $1.6mn) in the above example.

Some analogize record advances to loans, but that’s not exactly right since if the artist flops they are under no obligation to repay. And in fact, failure is the norm. The vast majority of artists do not recoup their advance. That a handful of successful artists compensate for the failure of many many others is sometimes why the artist & repertoire (A&R) business (that is, the business of finding and developing talent) is sometimes compared to venture capital. And like sophisticated venture capitalists, the major record labels are extremely savvy about contract language and have over generations conjured all sorts of ways to minimize risk. Among other measures, most contracts contain cross-collateralization provisions, which means any royalties earned on your second album will first go towards covering deficits on the first, and so on. They also impose a ceiling on advances for subsequent albums5[6] and diversify revenue streams through 360 deals that take a cut on gross proceeds the artist realizes from acting, touring, sponsorships, and other activities. Furthermore, traditional record deals stipulate that after committing to 1 or 2 albums, the label is granted options for another 4 or 5, so they can exercise each incremental option while the artist is hot and cut bait otherwise.

In staking risk capital to develop artists, record labels have decade+ rights to or outright own the Masters, entitling them to long-term annuity-like earnings streams. It’s unlikely that a label generates much of a return in the initial 2-3 year frontline window, where the label is spending significant resources to break a new artist. After that initial investment period, however, when the track moves into catalog, a recorded track’s cash flows can be milked with very little incremental promotion (Sony isn’t putting nearly the same amount of money promoting the Beatles as they are a newer artist). You might think of frontline A&R as a low-margin feeder into catalog, where the real money is made. Catalog music makes up maybe 50% of a major label’s revenue but 70% of its profits6[7]. Universal reported that catalog (3+ years) contributed 58% of its digital and physical recording revenue last year. Not only do the catalogs of major labels make up the bulk of recording profits, they represent a key source of power. According to MRC data from Billboard[8], catalog (18+ months) music accounted for 75% of music consumption in 2021, up from 66% in 2020. The vast majority is owned by Universal, Sony, and Warner. A music steaming service doesn’t work without catalogs from all three.

The other meaningful business segment for the major labels, comprising around ~16% of segment profits, is publishing. A publisher is to songwriters what a record label is to artists: they license song compositions and lyrics to programmers and share the resulting revenue. So when Spotify streams a song, they pay two sets of royalties that sum to around 70% of subscription revenue: one to the recording rights owner, who gets ~52%, and another to publishers and songwriters, who together take another ~15%. Unlike the recorded music segment, which lays out VC-style risk capital to popularize artists, publishers are tasked with the safer, less capital intensive role of administering song copyrights (securing licenses, collecting money, and paying writers). Their cash flows largely piggyback on the investment put in by record labels.

And whereas record labels strike direct bespoke agreements with each programmer that are re-negotiated every 2-3 years, the royalty rates earned by publishers and songwriters are for the most part mandated by statute. That’s because song reproductions in physical and digital formats are covered by a compulsory mechanical license7[9], meaning that under the Copyright Act the rights owner must license the song to anyone who wants it. In addition to mechanical licenses, songs are also protected by public performance rights, meaning any radio station, streaming service, nightclub, etc. that plays a song needs the rightsholder’s permission, which they obtain through a blanket license administered by Performing Rights Societies (aka “Performing Rights Organizations”), who keep track of all the places the music is played using methods that we don’t need to get into here.

In the US, the 3 major PROs are ASCAP, BMI, and SESAC. Publishers will license all their songs to these entities, who turn around and license the songs of all the publishers they represent to users (streaming services, radio stations, etc.) in exchange for a fixed fee that can vary from hundreds of dollars to millions depending on the size of that user’s audience. After subtracting their operating expenses, PROs distribute half the remaining funds to writers (the “writer’s share”) and the other half to publishers (”publisher’s share”). Typically, the publisher will then pay half their share to the songwriter, who thereby ultimately ends up with 75% of the total PRO distributions (50% + 1/2 x 50%)8[10]. Mechanical licenses are issued in the US by the Harry Fox Agency, who takes 11.5% of the associated fees it collects (though some larger publishers, enabled by technology that makes it easier to administer licenses, are reaching deals directly with licensees). HFA passes these fees to the publisher, who in turn passes half to the songwriter.

(you might wonder whether streams and digital downloads, which can be categorized as either public performances or song reproductions, are governed by mechanical or performance licenses, which impacts how artists are paid. In many European countries, downloads are 25/75 performance/mechanical and interactive streaming is 75/25; in the US, interactive streaming is mechanical but the publisher is paid under a complex formula whereby the DSP pays 15% of subscription revenue (a rate set by the Copyright Royalty Board), part of which is allocated to the performance license fee (for reporting purposes, Universal and Warner break out “digital” as a line item that is separate from mechanical, which for reporting purposes only covers only physical media).)

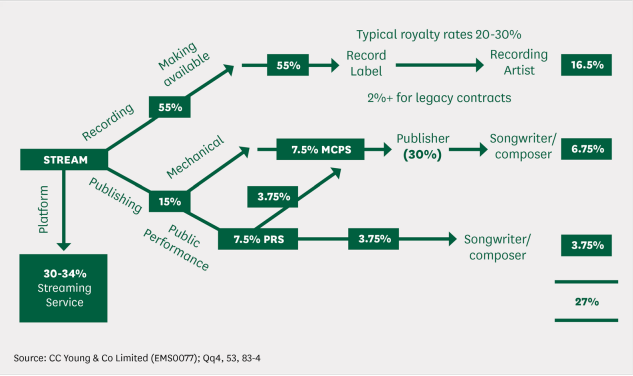

The labyrinthine division of a DSP subscription dollar is summarized below (the percentages below apply to the UK and differ somewhat from the US-biased percentages I used in my examples above):

Using my numbers, it looks like a dollar of subscription revenue realized by an interactive DSP roughly breaks down like this:

Record Label: 44c

Publisher: 6c

DSP: 33c

Artist: 8c

Songwriter(s): 8c

(the numbers don’t add up to $1 due to leakage from PRO and HFA fees)

So around half of every streaming dollar is paid to recording and publishing rightsholders who, in the case of the 3 majors, are housed under the same roof.

Note how the flow of funds in publishing differs from recording. Whereas in recording the labels collect all the money from the DSP and distribute royalties to artists, in publishing the money is intermediated by third parties, with the exception of songs used in TV shows, movies, and commercials, which are covered by direct synchronization (or “sync”) licenses between publisher and programmer.

(before I get “ackshually”-ied, let me state the obvious: for the sake of simplicity, I’m skipping over lots of contingencies and nuances. Revenue share differs by media and geography, and the bargaining power of the various parties involved can alter the distribution of earnings rather significantly. If you are interested in the gritty details, I highly recommend reading Donald Passman’s All You Need to Know About The Music Business, which is where I pulled many of my numbers.)

III.

The bull case for Universal and Warner is easy enough to understand. They own or license exclusive rights to a pool of IP whose value continues to appreciate in value as its presence in our lives becomes ever more ubiquitous. With recorded music consumption shifting from physical sales and downloads to digital streams, music is being monetized as predictable and recurring revenue rather than as one-off sales, in much the same way enterprise software is purchased as SaaS subscriptions rather than perpetual licenses. And whereas the SaaS migration came with a gross margin trade-off for software vendors, the transition to digital music delivers a margin lift for the record labels, who no longer bear the costs of manufacturing and distributing CDs.

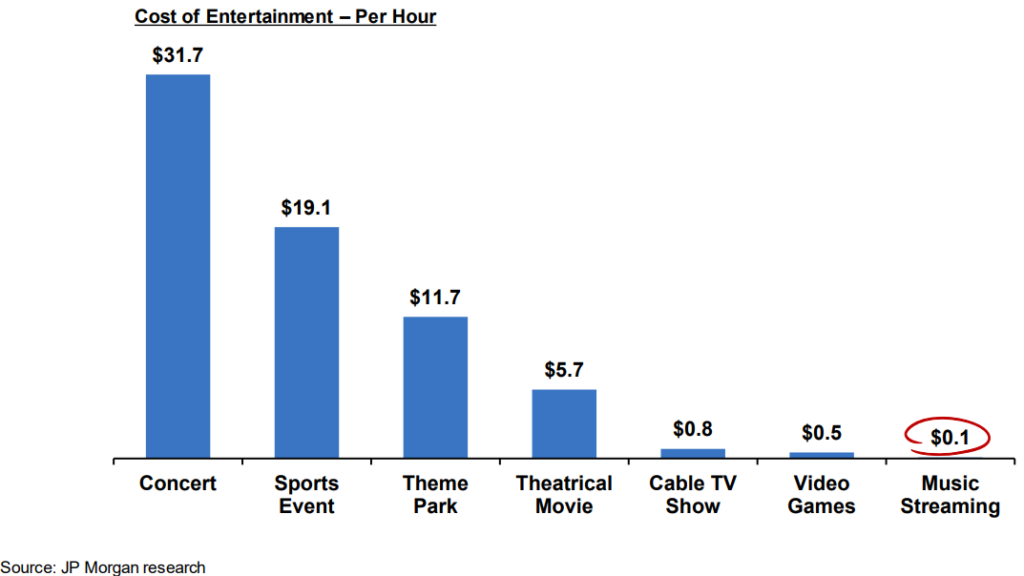

Goldman Sachs sees worldwide streaming subscriptions growing by 10%/year to 1.3bn9[12]. Pershing Square, who owns 10% of Universal, expects more like 14%. In either case, most of the growth will be fueled by emerging markets (Spotify reports 32% MAU/TAM penetration in established markets compared to just 8% in in emerging), where ARPUs are substantially lower (Spotify’s Premium ARPU has declined by around 6%/year since 2016 due to this mix shift). Some of that dilution should be offset by ARPU gains in developed markets, as music remains very under-monetized compared to other forms of entertainment:

Source: Pershing Square presentation

At the 1999 peak of recorded music revenue, the average CD buyer spent around $45 a year on music10[13], so maybe 30 to 40 songs across 3 CDs? Today, a Spotify subscriber pays less than 3x as much for ~70mn tracks, the same as a Rhapsody subscriber paid for 5mn songs[14] in 2008.

In addition to streaming platforms, music is being woven into all kinds of once inconceivable use cases. In the mid-2000s, the labels were partnering with mobile providers to capitalize on ringtones; today, they supply the background soundtrack to Peloton classes, Roblox scenes, and TikTok challenges. Warner’s revenue from these emerging applications have more than tripled over the last 2 years and account for 7% of its recorded music business. Warner, Sony, and Universal sit are both toll booths sitting between artists and the hundreds of digital platforms through which fans access their music.

The big 3 occupy this privileged position because they control most of the rights to the industry’s catalogs, which comprise nearly 3/4 of US streams. This speaks to a unique property of songs: as 3-5 minute snippets of sound that concurrently augment other activities, they are played over and over again. Movies and TV shows, which require more time and dedicated attention are, on the other hand, typically watched just once or twice. Spotify, Apple Music, and Amazon Music can’t differentiate on unique content the way Netflix, HBO, and Hulu might, nor can they source from a fragmented base of owners. Imagine subscribing to a platform that doesn’t carry Taylor Swift, Drake, or The Beatles. It’s a non-starter. A streaming service that doesn’t license the catalogs of all 3 majors is no streaming service at all.

IV.

So on the surface, Universal and Warner check the classic compounder boxes – they are oligopolists in a growing end market with stable demand, monetizing long duration assets as recurring earnings streams with few reinvestment requirements. But some of the factors that have catalyzed the industry’s renaissance also give rise to new challenges.

With technology and social media making it easier to directly reach fans, bargaining power is shifting from the record labels to artists, who are negotiating higher royalties and advances while reducing the number of optionable albums. The deal used to be that in return for assuming the risk of promoting new talent, record labels could bank on owning recording rights into perpetuity. But it’s become more common for artists to own the recording rights and lease them to record labels, as in the case of agreements struck with Drake, Taylor Swift, and Jorja Smith (as Prince once put it[15], “If you don’t own your masters, your master owns you”). In some cases Masters are returning to artists within 10 years. On the publishing side, rather than grant partial control of copyrights to publishers and split the earnings 75/25 under co-publishing agreements, it is becoming more common for songwriters to own the compositions entirely while paying publishers a 10%-15% administrative fee to manage licenses and collect royalties.

To what extent does label sponsorship contribute to stardom? Do record labels turn artists into superstars or do they merely glom rising talent? In the analog days, the answer was cut and dry. Teams of A&R men with honed intuition would scour local clubs and review submissions from managers to discover unknown artists and feed promising talent through labels’ massive distribution machines. As I wrote in my Sirius/Spotify post:

They steered which songs were played in radio stations and controlled distribution by colluding with major retailers like Musicland and Tower Records. In owning production, discovery, and distribution – costly functions that could not be independently undertaken by artists – record labels functioned as kingmakers for a select few, leaving a long tail of artists who toiled in obscurity, with no way of getting their music in front of fans.

But high quality DIY recording tools and free online distribution have obviated some of gatekeeping functions once played by record labels. Billie Eilish and Jorja Smith got their start uploading tracks on SoundCloud. Stormzy came up by posting freestyle raps on YouTube. Lil Nas X’s “Old Town Road” blew up on TikTok before hitting Billboard charts.

TikTok has blossomed into a major discovery engine. By now we’ve all seen the TikTok of 420doggface208 posted skateboarding with a bottle of Ocean Spray Cran-Raspberry juice in hand, lip-syncing to Fleetwood Mac’s “Dreams”, a sensational viral moment that catapulted this 1977 hit to the Rolling Stone Top 100 and led to a surge in digital downloads and streams of the song [16]within days of the post. Music Journalist Elias Leight remarked “TikTok is like a machine gun shooting out viral songs even more than daily”. But TikTok’s influence on the music industry goes beyond one-off cultural moments. Here is a 2021 study from Vox[17] that details how TikTok virality can change the long-term trajectory of a musician’s career. Of the 125 unestablished artists who went viral on TikTok after January 202011[18], 46% went on to sign with a major record label, and of the 367 artists who landed their first record deal, 1/3 cited a viral moment on TikTok as the catalyst.

Nearly every one of the 125 TikTok artists with a viral hit saw a corresponding spike of streams on Spotify (the “TikTok-to-Spotify” pipeline), and almost all then saw their other tracks included on editorial playlists. Of the 332 unestablished artists who made Spotify Top 20 Chart after January 2020, 1/4 caught their big break on TikTok. An artist who goes viral on TikTok is very likely to be approached by every major label, which can lead to a frenzy of bidding activity that results in far more favorable royalty and licensing terms than DIY artists could negotiate 10 years ago. The major labels will insist that their relationships with hundreds digital platforms yield data advantages that can be used to plan tours and guide marketing, but to collect data across online properties they are often relying on third party tools like Chartmetric and Instrumental that are used by other labels and managers. Also, when it comes to discovery I question value of platform relationships as the tracks being discovered originate from viral moments generated by a handful of services – a track goes viral on TikTok before percolating across the hundreds of other DSPs – whose public data everyone more or less has equal access to.

For a flat subscription fee, DistroKid (which raised money at a $1.3bn valuation in Aug 2021), CD Baby, and Believe Digital (slash TuneCore) will distribute across TikTok, YouTube, Spotify, Apple Music, etc.; track streams and downloads; and even collect money for independent artists without taking a cut (CD Baby will even press vinyl records). There are also independent labels who will distribute for a much lower cut of revenue than full service majors while charging separate fees for other services like marketing and promotion. MiDIA Research[19] reports that the major labels continue to lose a bit of share (~30 to 100bps) to independents and self-releasing artists every year. And while the big 3 plus Merlin (who represents hundreds of large independents) still account for 78% of streams on Spotify, this is down from 87% in 2017. Music, like other creative pursuits, has and always will generate a disproportionate share of revenue from a small percent of artists, but the distribution isn’t as skewed as it was in the 1990s12[20], when literally the only way to get in front of a big audience was to be sponsored by a major label.

I don’t think this is such a big deal though as the incumbents have long operated independent label subsidiaries, with Sony Music’s recent $430mn acquisition of AWAL a salient accent on their long-standing practice of rolling up competitors. Universal, Sony, and Warner are often thought of as monolithic entities, but it’s more accurate to think of them as holding companies for a bunch of genre and region-specific labels. Besides maybe some differences in genre mix and leadership (Universal’s Lucian Grainge is a legendary A&R talent while Warner’s Stephen Cooper is more of a nuts-and-bolts financial guy), they all basically have the same operational setup, compete vigorously for the same artists, and fast follow each others’ strategies.

And for all the anecdata about artists throwing it back in labels’ faces, mega-stars, who you’d think would be in the best position to disintermediate labels, continue to depend on them. Taylor Swift famously re-recorded and released covers of her first 5 albums to devalue her original Masters, which came to be owned by Ithaca Holdings, whose founder/CEO Scoot Braun was publicly called out by Taylor as a “bully”, before being sold to private equity. This re-recording gambit was so successful, with the new covers outperforming the originals, that in recent contracts Universal Music has been “effectively doubling the amount of time that the contracts restrict an artist from rerecording their work[21]”. But though Swift – an 11-time Grammy winning dynamo with 183mn Instagram followers – now owns her Masters, she relies on Universal-owned Republic Records to promote and distribute her work. And after gaining organic traction, Billie Eilish signed with Darkroom/Interscope (owned by Universal), Jorja Smith with Sony/ATV, Lil Nas X with Columbia Records (Sony Music) and Stormzy with Atlantic (Warner Music). I don’t think there is a single top 50 artist that isn’t represented by a major record label, either through long-term licensing terms, during which most of the IP value is extracted, or outright copyright ownership.

I’m reminded of this anecdote relayed by Arman Gokgol-Kline, a partner at Ruane, Cunniff & Goldfarb in his Business Breakdowns interview[22]:

I spoke to a professor at Berkeley College of Music, which one of creme-de-la-creme music schools in the country, about various aspects of this business. And one of my favorite stories he told me is every year I ask my students to raise their hand when I say to them, “Who likes labels and wants to work with a label?” And nobody raises their hand. And then he says, “Okay, now imagine one of the major labels comes to you and gives you an upfront and wants to sign you. Who would sign on with them?” And everyone raises their hand.

At the end of the day, every musician dreams of stardom and getting there takes more than mere integrations with DSPs. There are 60k tracks uploaded to Spotify every day. How does an artist stand out? The major record labels may no longer have as tight a grip on discovery, but through large advances, promotion, and creative support; relationships with radio stations, movie studios, and global distributors; and the market share to exert soft influence on streaming services to promote their artists, they in a better position than anyone to supercharge talent that has broken out of obscurity. Labels can provide a menu of services tailored to the varying needs of stardom-bound talent, with mid-tier artists availing themselves of short-term distribution deals with independent subsidiaries before then graduating to full record deals as they become more popular.

For the few artists who do manage to become superstars, often the best way to capitalize on popularity is through live concerts. From Business Insider[23]:

Consider, for example, U2[24], which made $54.4 million and was the highest-paid musical act of the year in 2017, according to Billboard[25]‘s annual Money Makers report. Of their total earnings, about 95%, or $52 million, came from touring, while less than 4% came from streaming and album sales. Garth Brooks (who came in second on the list), owed about 89% of his earnings to touring, while Metallica (ranked third) raked in 71% of their earnings in the same way.

The labels take a healthy cut of streaming revenue but they also raise a superstar’s profile, which helps maximize the value of live appearances.

V.

While record labels are best characterized as service businesses, those services are preceded by up front advances, and the capital requirements have gotten bulkier as competition for publishing catalogs has intensified.

As I mentioned earlier, whereas the revenue split between recorded music rightsholders and the programmers who license those rights are individually negotiated and determined by the relative bargaining power of the two parties, the share of revenue paid by licensees to publishers and songwriters is set by the CRB. While the CRB’s rate rulings can seem unfair to whichever party finds itself on the wrong side of them – to the consternation of DSPs like Spotify, a 2018 CRB ruling raised the payouts on mechanical streaming from 10.5% to 15.1%[26]13[27] – it seems they also come with concessions so that no side decisively wins. And so, because payout terms are set by law rather than by unpredictable market forces and because cash flows largely ride on the investment that record labels put in to popularize artists, publishing is seen as a very long-lived14[28] and low-variance annuity.

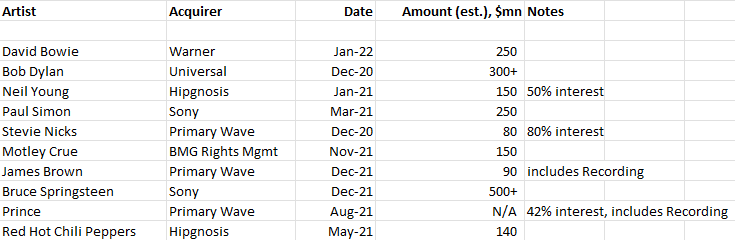

The last 5 years have seen heightening bidding for song catalogs, with much of this activity fueled by financial buyers. Last October, Blackstone partnered with Hipgnosis Song Management[29] (a music IP investment company), providing $1bn of funds. The same month, Apollo backed HarbourView Equity Partners[30] with $1bn. In February, KKR and Dundee Partners acquired a catalog from Kobalt Capital (which includes songs from the Weeknd and Lorde, among others) for $1.1bn and securitized the portfolio of rights. Last June, Oaktree Capital invested $375mn[31] in independent publisher Primary Wave. A few months after acquiring a majority stake in the publishing and recorded music rights of OneRepublic and the band’s lead vocalist and songwriter Ryan Tedder, valued at $200mn, KKR announced a joint venture with former portfolio company BMG[32], which has since acquired more than 250k copyrights from more than 1k artists and songwriters, including Billy Idol and ZZ Top. This JV is similar to a partnership that Providence Equity Partners struck with Warner Music in 2019.

Here is a sample of some notable catalog acquisitions over the last 1.5 years, some of which include other IP rights besides:

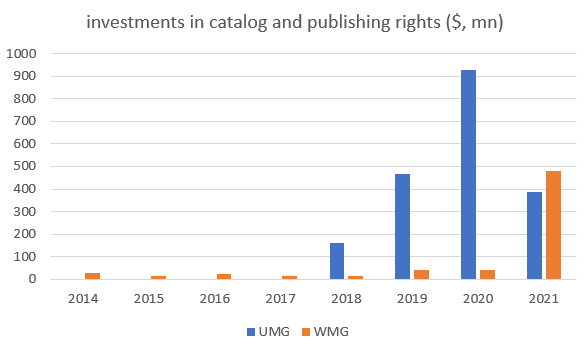

Since its 2018 IPO, Hipgnosis has spent $2bn on IP rights. Warner and Universal have followed suit, investing more in catalogs than they have in years:

(Warner’s fiscal year ends September)

All this frenzied biding has driven deal multiples from a historic valuation of 8x-12x net publisher’s share [34](revenue minus royalties paid to songwriters) to 25x-30x, raising understandable bubble concerns. The enthusiasm is especially concerning to investors because this is the entertainment industry, where creative egos loom large and vanity and empire building often trump financial considerations. On earnings calls and annual reports, Universal and Warner will, with puffed chests, brag about the marquee catalogs they’ve acquired and how many of Top 10 artists they represent (Warner Music has none of the Billboard top 10; they’re doing just fine), while offering no details whatsoever on deal terms or the returns they expect to earn on those investments. With more market share, labels can exert influence on streaming platforms and perhaps also signal credibility to new promising talent – “if a 360 deal with Universal is good enough for Drake, it’s good enough for me” – but separate from those commercial factors, it also confers bragging rights.

A more charitable take on this phenomenon is that the economics of streaming make up for higher deal multiples. I mean, sure, 10-15 years ago catalogs were being sold at 10x, but with the industry crushed by piracy and no proven business model in sight, their earnings streams were also subject to a lot more risk. Moreover, in the 2000 peak, nearly all recorded music revenue came from CDs that were sold in stores, whose shelves could not accommodate a popular artist from 20 years ago. In the streaming era, all the music is available all the time, so one might argue that the useful life of content is longer than it used to be and, when paired with a user-generated content engine like TikTok, is also more discoverable. 420doggface208 skateboards to “Dreams” and a rock band from the ‘70s is resuscitated back into relevance.

Also, the major labels can do more with publishing assets than private equity can. When financial players buy music catalogs, most of the time they are just interested in passively milking bond-like cash flows and levering them up to hit return bogeys. They might do a somewhat better job administering publishing assets better than the previous owner, but I doubt there’s much incremental return from that. Universal, Sony, and Warner, on the other hand, are operators who often own or license the rights to both the publishing catalog and catalog’s associated recordings, which gives them more flexibility to grow and maintain song catalogs by pursuing sync deals with movie studios and licensing arrangements with fitness, gaming and social media apps, or creating biopics, music films (like Rocketman and Bohemian Rhapsody), remixes, and other derivative fare, all of which requires the okay of both the recording and publishing rightsholders. So although they are paying double or triple what they used to for catalogs and accepting somewhat worse commercial terms from artists, the labels might still nonetheless realize more value on a risk adjusted basis than they did in the past. I don’t know that that’s true, but it seems plausible?

I’m eyeballing things a bit as disclosure isn’t great, but the returns on content (EBITA / gross content assets) in Warner and Universal’s publishing businesses look close to respectable at around 9% to 12%. The recording side, comprising over 80% of profits for both companies, has enjoyed phenomenal returns – Warner’s recording segment assets have grown ~$700mn from fy16 to fy20 while EBITA is up ~$500mn; Universal’s recording content assets + goodwill have grown by €1.3bn from 2018 to 2021 while EBITA is up maybe €700mn over that time – which makes sense given the streaming tailwinds and the fact that the majority of recording profits come from catalogs that don’t require much incremental investment.

The management teams at Universal and Warner pinky swear that they’re focused on returns and now both companies have public investors holding them to that promise. Their business models seem to be less about high variance artist discovery and development than about making more assured, educated financial bets on things that seem to be working, whether that means signing record deals with breakout TikTok sensations or acquiring song catalogs with demonstrated longevity. The increasing speed with which tracks mushroom into popularity (”TikTok-to-Spotify” pipeline) may accelerate the recoupment of advances and improve IRRs. Anecdotal concerns that artist royalties are growing more generous and that whatever cost savings realized in the shift from physical to digital will be offset by higher promotion costs aren’t apparent in the numbers – as a % of recording revenue, Warner’s A&R costs have declined since fy16. Warner and Universal have enjoyed consistent EBITDA margin expansion in recent years.15[35]

But what about the next 5 or 10 years? That the pool of recorded music revenue will continue to expand as music pervades more digital experiences seems like a pretty safe bet, but an industry structure characterized by concentrated pockets of power in different parts of the value chain – superstar artists, record labels, and digital steamers – puts some checks on surplus accrual. The degree to which new modes of discovery and consumption have neutralized the value proposition of the major labels and the power they wield in the music ecosystem, has up to now been more than offset by the radical turnaround in industry prospects that those modes have enabled. I don’t think the big 3 face material existential risk, as they effectively control the key ingredients to every viable streaming service and signing with them is still the best way for a superstar to reach the widest audience. Still, it wouldn’t surprise me to see the combined squeeze of higher artist royalties, a mix shift from full service to modular arrangements, and unfavorable commercial agreements with Spotify hinder margin expansion plans.

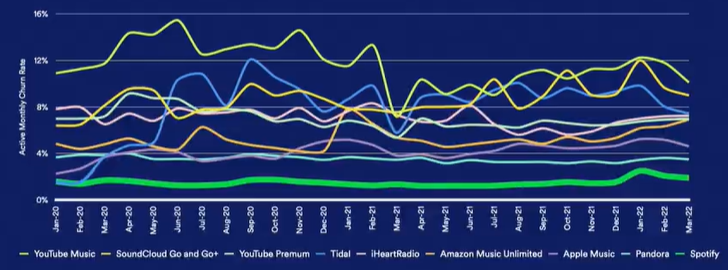

Remember when Spotify bulls looked to Netflix as an aspirational comp? By paying fixed sums for content, Netflix could drop most of the incremental revenue to EBITDA and wouldn’t it be great if Spotify could do that too instead of passing 70c of every subscription dollar to rights owners. But one of the downsides to video streaming is that it requires differentiated content, which puts streamers on a never-ending spend treadmill to retain existing subs and acquire new ones. In music, because every streaming platform must license all the songs from all the majors to be even minimally viable, the basis of competition shifts from content to user experience. A consumer has no reason to switch from Spotify to Apple or Amazon to access original content since they all carry the same stuff, so they opt for whoever provides the best curation and build personalized playlists on that service, locking themselves in over time:

Source: Spotify Investor Day Presentation (Jun 2022)

Benedict Evans has this line about how all the questions that matter for Netflix are about Hollywood, not technology. But in music streaming, where content is a shared commodity, technology drives differentiation.

Streaming music isn’t such a great business in isolation but it creates a captive base on which Spotify can layer low marginal cost revenue streams. The idea that Spotify could leverage its users to disintermediate labels was a popular bear thesis for Warner 3 years ago. But investors have come to see that the game theory of mutual assured destruction prevents either party from bypassing the other (a streaming service isn’t competitive without labels’ catalogs and artists won’t put up with a label that doesn’t distribute on the market leading streaming service). I think this is the right take. But that doesn’t mean Spotify can’t extract value from the labels in other ways. For instance, with all the first party engagement data they have on an audience that is primed to discover new tracks, Spotify has spun up a marketplace that labels can use to promote their artists’ music to new fans. Rather than attempt to disintermediate labels or fight for greater share of subscription revenue, Spotify can grab margin by charging them for access to its subscriber base. Wary of tying their fortunes to a single, ever dominant platform and keenly aware that marketing can be an easy stream acquisition tool when used by one player but an industry tax when used by all, the labels might be reluctant to spend too heavily on Spotify. But they all care about stream share and it only takes one defector to break the dam. There are signs of traction. Marketplace revenue has grown from €20mn to €160mn in just 3 years and has been the primary driver of Spotify’s music gross margin gains.

Podcasting is the other hopeful money maker. Since getting into podcasts in 2018, Spotify has spent $1bn on content, with just $200mn of annual revenue and enormous losses to show for it. But while podcast industry ad revenue is a small ($2bn) ,it is growing rapidly (500%+ since 2018) industry and with Original and Exclusive content representing a disproportionate share of the Top 100 podcasts on its service, Spotify is taking share. So management thinks that by growing ad revenue on a largely fixed cost base they can eventually get podcasting gross margins to 40%-50% (vs. 27% for the overall company today). Podcasting, like music, is audio but the useful life of content is shorter and the business model has more in common with video streaming, where content is once again a vector of differentiation and the usual perpetual inflated bidding concerns apply. But augmenting music with exclusive podcast content should better retain existing users and also draw new ones, some of whom will convert to Premium subscribers, emboldening Spotify to demand a greater share of revenue. Of course, the matter of who has more bargaining isn’t specific to Spotify but pertains to any service that commands a massive audience, including (no, especially) TikTok, where discovery plays such a central role and I imagine labels’ mature catalogs have far less value. Though then again, the labels will argue that they are getting a growing share of revenue from emerging channels like social media, fitness tech, and gaming, making them less reliant on Spotify. I don’t have a strong intuition about who will find themselves in a better position to demand better economics 5-10 years from now.

Owning the consumer relationships gives Spotify options on new sources of value creation (podcasts, audiobooks, NFTs??), but getting those options in the money means spending boatloads to acquire subscribers and content. The music labels more or less just free ride off that. While Spotify YOLOs into new TAM, their 3 largest suppliers clip low variance cash flows.

The labels pitch themselves as tech savvy, forward looking operators with a firm pulse on the trends. But let’s be real. When P2P sharing heaved the industry into existential crisis, the best the incumbent labels could do was fight back with lawsuits. It fell upon Apple and then Spotify to push the industry to its current profitable equilibrium. That’s not to say the record labels aren’t more attentive to new ways of capitalizing on talent (with all monumental changes over the last 10 years, how could you not?) but for the most part I see them as gold mines of IP protected by sharp legal teams, managed by A&R folks whose art for discovering talent is increasingly subsumed by the technicalities of scrapping engagement data that is concentrated in a handful of streaming platforms. This isn’t necessarily a bad thing! That the big 3 absorb most of the industry’s profits despite contributing the least to its innovation tempo is maybe the most compelling testimony of how durable their legacy advantages may be. It’s hard for me to gain that much conviction in any single consumer facing app that monetizes through fickle and scare attention (Netflix isn’t just competing against linear TV but Fortnite, TikTok, Instagram, etc. TikTok was born just 5 years ago and today has Facebook quaking in fear). The record labels are a safer bet that whatever the next big social experience turns out to be, music will play an important role.

Disclosure: At the time this report was posted, accounts managed by Compound Insight LLC owned shares of AMZN. This may have changed at any time since.

scuttleblurb 2024 content review

Posted By

scuttleblurb

On

In

SAMPLE POSTS |

No Comments

Happy holidays everyone,

This post will kick off an annual tradition where I provide brief summaries of blog posts published during the year. As always, I’ll discuss my thoughts on the business of scuttleblurb in my annual interview with LibertyRPF[36]. Most of the text in the summaries below is extracted directly from the write-ups and all commentary reflects my views at the time they were written. These summaries in no way do justice to the actual posts. They are meant to be teasers that I hope will convert some free subs into paying subs and encourage paying subs to take a second look posts they may have passed over for lack of immediate interest. This will be the last post of 2024. I will begin the new year with writeups on AppFolio and Maravai.

A few other announcements:

First, on a personal note, I recently launched a gofundme for Boulder Crest Foundation[37] in honor of my brother, Rich, a veteran of the Iraq and Afghanistan wars who struggled with combat stress for many years before taking his own life this past March. Boulder Crest has helped more than 100,000 veterans, servicemembers, and first responders transform their struggle with trauma into strength. Their Warrior PATHH[38] program includes a 7-day in-person initiation retreat, followed by 90 days of dedicated support and accountability. It is offered to participants at no cost. Please join me in supporting the brave men and women who have made enormous sacrifices on our behalf. To those of you who have already donated, I am incredibly grateful. So far, we’ve raised more than $36k (including my match contribution), blowing past the original $10k goal.

Third, I’m excited to announce that MBI[41] and I launched a podcast, where we casually chat about companies we’ve written-up once a month. The first episode is a discussion on AppFolio (Spotify[42], Apple[43], RSS feed[44]). MBI writes a terrific blog[45] and if you aren’t already a subscriber, well, you should consider becoming one!

Finally, thank you all so much for the support and feedback you’ve given me over the years. It is a joy and privilege to write this blog for you. See you in the new year!

On the differences in serial acquisition programs, from [AME] AMETEK[46]

“As a serial acquirer grows, so too does the amount of M&A required to move the needle. But because, as a general rule, the larger the deal size the loftier the valuation, it’s not just how much capital gets deployed that matters but over how many acquisitions.

….Vertical market software disaggregates across countless pockets, but software is alike enough that you might treat VMS as a giant, homogenous mass. Constellation can do 100+ deals a year because the playbook applied to running a software business that sells to restaurants also mostly applies to running a software business that sells to spas or auto repair shops. Constellation Software is less a bet on technology or product or even end market than it is a bet on a system for efficiently researching and acquiring small software companies at scale, and the more companies they buy the larger the database against which to hone base rates on future acquisitions.

So my point is: when the angle to M&A is less about technical sophistication than it is offering a permanent home for sellers plus superior execution against a sticky customer base, the particulars of product and end market seem almost beside the point. Competent managers with pride of P&L ownership, supported by the right incentives to drive value, are the critical drivers.

Teledyne is governed by a different dynamic. They do in fact acquire for differentiated technology, technology that tends to be concentrated in just a handful of companies, companies that become increasingly scarce as they become big enough to absorb the growing sums of capital that Teledyne needs to deploy every year. Also, Teledyne doesn’t want technology that is too far outside their existing competencies, which further limits where they can hunt. These constraints force them to accept lower returns as they put more capital to work. So unlike Constellation, Teledyne has deployed larger amounts of capital by buying bigger, not more.”

“…while BFS’ share repurchases are optically accretive (”share count go down”), they are extremely concentrated during periods when share prices are elevated. Why? Because BFS returns cash to shareholders when they have lots of it to spare, which happens to coincide with cyclical peaks, which also happens to be when the stock is soaring.

Buybacks = dividends. That’s Finance 101. Management can repurchase shares or pay a dividend to shareholders, who use that cash to buy shares themselves. No value is lost or gained. Same-same. But that equivalency assumes that the company is no better at repurchasing its own shares than shareholders themselves.

Buybacks generally fall into two buckets:

opportunistic: management has a better sense than shareholders do of whether their company trades at less than intrinsic value per share. They can buy their stock better than shareholders can. In this case, repurchases are preferable to special dividends paid to shareholders.

programmatic: management uses cash flow to buy shares, without any assessment of intrinsic value. The cash comes in, they turn around and buy shares with it. Assuming cash flows are reasonably stable from one year to the next, management will find itself sometimes buying stock when it is cheap (below IV) and sometimes when it is not. The company has no better or worse sense than shareholders of when the stock is cheap or expensive, so it makes no difference whether they repurchase shares or shareholders buy shares with dividends they receive from the company.

An investor would prefer 1) over 2), but 2) isn’t necessarily value destructive so long as cash flows are somewhat consistent from one year to the next and intrinsic value grows at a reasonably measured pace. An analogy here would be an investor who auto-invests her steady paycheck in an equity ETF without any regard to valuation or market timing. Some of those purchases will turn out poorly, others great, but on balance things should turn out all right so long as the diverse collection of businesses constituting the ETF create value over time.

But now imagine a business that implements a programmatic buyback butalso generates the vast majority of its cash at cyclical peaks. A special dividend would be better in those cases because even an investor who uses that dividend to buy more shares but does so at random will outperform management, who systematically invests at the top and at no other point.”

Garbage collection and disposal is one of the few businesses that you can be sure will still be around in 20 years. Its recurring necessity gives rise to predictable and stable cash flows. Residential collections are locked in under 3 to 10 year exclusive agreements that are very hard to lose, as city officials don’t want to risk pissing off voters by re-bidding contracts, a lengthy and onerous process that could disrupt garbage pickup. Commercial (retailers, restaurants) and Industrial (manufacturers, contractors) customers are secured under 3-5 year contracts that are tough to profitably steal away from incumbents who have established route density (the more customers a collector has along its route, the more cost effectively it can serve an incremental customer). They will accept hike prices without much resistance because trash collection is a necessary but small enough[49] component of their overall operating costs.

In its May ‘22 Investor Day, GFL projected C$1bn of free cash flow by 2024, a target that they were soon forced to walk back after being hit with soaring fuel costs and interest expense (~28% of its debt floats). These headwinds would prove manageable. Throughout 2023, management recovered underlying margins by pushing through fuel surcharges and higher base rates, and improved the balance sheet by using proceeds from the sale of certain non-core assets. But even absent the divestiture, with GFL pricing 100bps+ above cost inflation, I can see EBITDA growing by 8%/year, outpacing the 6% growth in cash interest expense and bringing leverage in line with a best in-class peer like WCN. Including incremental profits from renewable natural gas and Extended Producer Responsibility (EPR) fees takes free cash flow to C$1bn by 2025, growing to C$1.3bn by 2027, which capitalized at 25x implied a mid-teens return. In short, I see this as a low brain damage stock with a credible path to mid/high-teens returns so long as GFL manages the business responsibly and pushes prices above cost inflation. The harrowing economic climate of the last few years offered sound evidence that they can do just that.

Uniforming employees is an important but non-core activity. For safety and presentation reasons, healthcare professionals need to be outfitted with clean scrubs, electricians with flame-resistant gear, used car salesmen with matching polo shirts, etc. Companies could manage garment programs internally, but this entails various complexities they’d rather not spend time on. You could order a dozen maroon polo shirts from Amazon, but there’s no guarantee that Amazon will have in stock the same shade of maroon in a given size to outfit new employees as your business grows. If a plus-sized employee is replaced by someone with smaller dimensions, you’ll need to buy a brand new uniform while the XXL shirt and pants sit on the shelf. Over time, you will find yourself tying up more and more cash in garment inventory and volatizing cash flows with unpredictable garment purchases. By assuming inventory on their own balance sheet, a uniform rental provider can help dampen the swings and ensure you get exactly the right uniform when it is needed.

The business of buying and renting uniforms is operationally complex (not only are rental providers collecting shirts, they are cleaning and returning them to customers as well), vulnerable to alternatives (customers can always just buy shirts and pants for their employees) and, outside of enterprise accounts, isn’t protected by high switching costs, which limits pricing power. And yet, Cintas has created enormous value for shareholders, its stock compounding by 15% over the last 20 years and 27% over the last 10 (before dividends). Over the last decade, they’ve outgrown primary competitors Unifirst and Vestis on an organic basis and realize far more revenue per employee and facility than either. They’ve done so through a combination of better route density and superior execution, the latter evidenced through ERP modernization, vertical-specific offerings, and smart M&A.

Vestis recently spun-off from Aramark, an inattentive owner who mismanaged the company for many years. The turnaround story involves margin expansion and accelerating organic growth, powered by cross-selling and route optimization. I have concerns about the practical difficulties of dual-purposing unionized truck drivers as salesmen and question whether Vestis’ antiquated systems can support the logistical complexity required to compete head on with Cintas, who spent a decade modernizing its ERP.

At the time it was spun-off of Allegheny in 1991, Teledyne was primarily in the business of selling electrical components and subsystems – devices that amplified microwave signals, transmitters and receivers that send signals from aircraft to ground equipment, sensors and software that stored telematics data, etc. Starting in the early 2000s, they made a series of margin accretive acquisitions that expanded their presence in Instrumentation, which you can think of as things that measure hard-to-see physical phenomena (sonar systems that map ocean floors; gyroscopes and accelerometers that measure location and speed; instruments that precisely measure gas flows and monitor air quality); and Digital Imaging, sensors that convert light waves into digital representations. These acquisitions transformed Teledyne. In 2004, the company got 80% its revenue from selling aerospace electronics and serving as a prime contractor for the US government. Ten years later, those businesses were whittled down to just 35%. The balance came from Digital Imaging and Instrumentation products used mostly in commercial applications, which has remained Teledyne’s primary focus since.

The next 7 years were characterized by progressively larger deal sizes in instrumentation and digital imaging that ultimately culminated in the whopping $8bn purchase of FLIR (short for “forward-looking infrared”), which made sensors to identify heat emissions from industrial gases, greenhouse gases, enemy combatants (night vision goggles), and overheating factory machines. At the time it was announced, the deal represented 54% of Teledyne’s total enterprise value and more than twice the $3.7bn spent on all previous acquisitions combined.

The FLIR acquisition was consistent with Teledyne’s pattern of buying adjacent technology. But the valuation was surprising. As late as 2019, they expressed bewilderment that anyone would pay 17x. Then, just a few years later, Teledyne announced they would be buying FLIR for…17x EBITDA! (more like 20x excluding the one-time COVID sales). And it’s not like FLIR was a fast growing gem of business. It had been mismanaged for some time and was growing by just 1%-2% when FLIR bought them. Even with optimistic growth assumptions and full credit for cost synergies, Teledyne paid 11x year-5 EBITDA, still a far cry from the 10% after-tax returns within 2-3 years that they’ve historically targeted.

But the collection of businesses Teledyne has rolled up over the years generally seem like good ones. Most of the high-end imaging and instrumentation niches where Teledyne plays are rational oligopolies. Their products are designed into systems with long development cycles and lengthy qualification processes, making them tough to displace. They are sold to customers who care far more about performance than price, insulating them from low-end Chinse competition.

The businesses don’t generate much growth, though. On a consolidated basis, organic revenue has grown by just 1.5% over the last decade. Adjusting for the mix shift toward Digital Imaging, forward growth is maybe more like 4%, but that does get you much more than 5%-6% organic earnings growth. You probably aren’t paying any more than 16x-17x earnings for something like that. If they can re-invest all their earnings into acquisitions at 10% after-tax returns, as they’ve done historically, you might justify the low-20s multiple that they trade at today. But can they? Will they?

AMETEK reminds me of Teledyne in several ways. It began its life in industrial machinery before acquiring its way to higher margin, more technically differentiated and less capital intensive areas. This includes instruments that measure and test things that are very close and very far away, stuff like: mass spectrometers and electron microscopes used by scientists to understand the structure of compounds and by semi manufacturers to detect impurities in silicon wafers; optical assemblies (lenses and mirrors that manipulate light) used by astronomers to study the planets; rheometers used by consumer goods manufacturers and coatings companies to assess how fluid-like materials behave under different stresses.

Alongside that is a smaller division that sells instruments that capture aircraft telematics, ruggedizes off-the-shelf components from other tech vendors (FPGAs from Xilinx, routers from Juniper) for aerospace and defense platforms exposed to extreme environmental conditions, supplies utilities with simulation tools to test the integrity of their grids. More recently, they’ve made a big splash in healthcare, now their single largest end market at 20% of revenue, with the acquisitions of Rauland-Borg (call stations, mandated by regulation, that patients use to call for help and that nurses use to receive those calls) and Paragon Medical (surgical instruments, bone screws, hip implants, rods, springs, wires, etc.). The acquisitions seem all over the place when viewed through the lens of end market exposure. But what they generally share in common are #1 or #2 positions in $200mn-$500mn oligopolistic niches, products with high switching costs, and, under AMETEK’s ownership, the rigorous application of kaizen values (AMETEK once referred to itself as a “mini-Danaher”). Revenue is wildly cyclical, geared as it is to a long tail of industrial markets, and organic growth through the cycle looks similar to Teledyne’s.

AMETEK has paid progressively higher multiples for higher quality, faster growing businesses (7x-8x in the early/mid-2000s to 15x for Paragon). The days of buying undermanaged companies for high-single digit multiples and doubling margins over 3-5 years are over. Compared to 10-20 years ago, they are leaning more so on growth than profitability improvements to hit their 10% after-tax return bogey within 3 years.

Of the 3 serial acquirers I covered this year, Roper has undergone the most extreme business transformation. From its starting point in capital intensive industrial equipment, Roper acquired its way into test and measurement instruments during the ‘90s, then software throughout the ‘00s. Management was intentionally targeting capital light businesses with high margins, recurring revenue, and modest macro sensitivity, with the directive that each new acquisition should be better on those dimensions than the portfolio average. If the bar is ratcheted higher every year, then whether you originally meant to or not, you will eventually end up buying software companies.

Roper’s software acquisitions covers a wide range of verticals and are grouped into 2 divisions: Network Software that, for instance, matches shippers with truck drivers (DAT), pairs general contractors with subcontractors (ConstructConnect), and consolidates purchase activity across long-term care facilities (MHA); and Application Software, which you can think of as industry-specific ERP software that customers use to run their operations. A prominent example of the latter is Vertafore, which P&C insurance agencies and brokers use to manage sales pipelines, renew state licenses, and track agent commissions, among many other things. Given how mission critical these products are to day-to-day operations, it comes as not surprise that Roper’s software divisions retain 95%+ of customers and consistently push through price hikes.

Roper is organized in a decentralized fashion, with 28 business units, each run by a manager with near full discretion to make strategic and operational decisions, though they do so within tight governance constraints that prevent financial metrics from veering off track. Capital allocation, meanwhile, falls in the hands of a handful of executives at headquarters, who work with third party professional services firms to diligence transactions. Nearly everything Roper buys comes from a private equity, Thoma Bravo and Vista in particular. Whereas a private equity firm will cost cut their way greater profitability over a 5-year time horizon, Roper, as a “forever” home, has the luxury of optimizing for growth and creating value over long time horizons. And thanks to their investment grade rating, they can borrow a much lower rates than a private equity sponsor.

Owners in both parts of the lifecycle can realize respectable returns. A PE sponsor who pays 27x depressed EBITDA for a 5% grower, funds the purchase with 8 turns of leverage, doubles margins over 5 years, and flips to Roper at 18x, will generate a 19% levered IRR. By taking organic growth up to 7%, funding with 4 turns, and expanding margins by ~30bps a year, Roper in theory might expect ~12%-13% levered IRRs, assuming a 15-year time horizon and a terminal EBITDA multiple of 13x

This is not to say that Roper has a dominant advantage when it comes to winning deals. They can’t outbid a strategic for a target with easy synergies, or even a private equity firm for a mismanaged target with a broken cost structure. But for well-run companies with full margins competing in modestly sized markets, a long time horizon, low funding costs, and competency at accelerating organic growth allow Roper to create value to an extent that neither strategics nor private equity can.

Most of Xpel’s revenue comes from selling a product that you may not even know exists. And that’s kind of the point. When installed right, paint protection film is hard to see. But its invisibility belies its utility. A thin and transparent wrap, comprised mostly of a versatile material called thermoplastic polyurethane, PPF protects a vehicle’s paint from scratches, bird droppings, acid rain, bug splatter, UV rays, and gravel strikes, with “self-healing” properties that allow the film to reconstitute itself after minor assaults.

In 2023, a widely circulated short report on Xpel[55] made two central claims: first, that Xpel gets much more of its revenue than it disclosed from Tesla, who was bringing PPF installation in house; and second, that PPG Advanced Surface Technologies (PPG AT), a joint venture between PPG and entrotech, “have developed a way to integrate entrotech’s paint protection technology directly into PPG’s paints” and that “the JV will set to integrate this technology directly with OEMs, straight from the production line, hence virtually eliminating the need for Xpel’s clunky aftermarket wraps”, obviating XPEL’s entire business.

As my conversations with PPG and Ford (the OEM supposedly integrating this supposed PPF-paint hybrid) made absolutely clear in no uncertain terms, the existential claim about PPF technology being integrated into PPG’s paint was fabricated. The Telsa concern had a bit more teeth to it. I called a bunch of dealers and, indeed, a disproportionate number of vehicles they wrapped were Teslas. But on the whole, they were not seeing much, if any, impact from Tesla in-sourcing. Moreover, a week prior to the short report’s publication, Xpel explicitly disclosed that its “paint protection film-related revenue (including product and service) with respect to Tesla vehicles is approximately 5% of its total year to date revenues”. The short seller interpreted this announcement as a desperate attempt to support the stock, which doesn’t make a whole lot of sense.

Consider what it means for the short seller’s claim to be right. Xpel dealers must enter into DAP the car model whose templates they want to cut from film, meaning management almost certainly knows how much film revenue is tied to each car model with a very high degree of accuracy. So by privileging survey results over Xpel’s disclosure what you’re essentially saying is that management, knowing the real percent of revenue coming from PPF installation on Teslas, deliberately published a fake number instead. So, after rescuing Xpel from near ruin and methodically building it over 15 years to a profitable market leader that is firing on all cylinders, Ryan Pape just decides “screw it, time to commit blatant securities fraud and risk career, personal reputation, and financial consequences that are bound to be far more disastrous than just saying the real Tesla number?” That’s a pretty bold claim, in my opinion.

Imagine you are General Counsel of a F1000 company and want to sue a competitor for violating your company’s intellectual property. While you have strong case, litigation is an inherently speculative undertaking. You don’t know whether the defendant will settle or fight and, in the latter case, whether a judge or jury will rule in your favor or even how long it will take for them to do so. Rather than run ongoing litigation expenses through the income statement, crimping the reported earnings that investors capitalize, in return for an uncertain payoff, which investors dismiss as a one-time event, you would much prefer the law firm you’ve hired to work on contingency, bearing the expense of litigation and sharing the spoils of a successful outcome. But the law firm, culturally and financially ill-suited to assume such risk, prefers the assurance of hourly fees.

This is where a commercial litigation funder like Burford steps in. Burford will commit to paying the law firm’s fees up to a certain amount and in turn take a percentage of any resulting settlement or damages paid. The client gets a free option on litigation; the law firm gets fixed hourly fees to pursue damages even as it serves the client on a contingent fee basis; and Burford, who pays fixed hourly fees to the law firm or corporate client, gets a piece of any resulting payoff.

In what seems like ages ago now Fintwit darling, Burford Capital, was flamboyantly attacked by Muddy Waters. The prominent short seller claimed that Burford “misleadingly boosted its IRR numbers”, rendering ROIC and IRR metrics “meaningless”; misled investors through the “egregiousness of its fair value accounting”; and was “arguably insolvent”, raising outside capital as a matter of survival rather than growth. These charges followed on the heels of a Canaccord Genuity analysis from Apr ‘19 that found Burford’s reported ROIC “confusing and significantly above reality”.

For most of this post, I once again provided a long-winded rebuttal of that bear case. My argument largely resolves to:

contrary to common perception that Burford’s historical returns are the result of one-off windfalls that we can’t bank on going forward, I would argue that settlements provide an engine for repeatable outcomes – outcomes that deliver, if not spectacular, at least solid returns – for approximately 70% of Burford’s invested capital. Moreover, Burford boasts an enviable track record outside of settlements. Just over 70% of capital deployed on adjudications from inception to 2023 has generated gains, up from 65% from inception to 2019.

and…

it appears much harder to compete away returns than many bears imagine. There is only so much capital that can be put to work in any given deal, the underwriting process doesn’t scale well, and its accuracy is aided by proprietary data that takes years to acquire. Given the resources, time, and lack of scalability, not to mention the added complication of suing enterprises that you’d like to maybe have business relationships with, I somehow doubt that someone like Blackstone is taking this market all that seriously.

But the lack of scale also pushes back against the bull case. Sure, Burford might generate strong asset level returns. But lawyer salaries (litigation finance deals don’t scale), finance costs, and taxes consume a lot of this. Consider that Burford’s tangible book value per share ex. YPF (a one-off windfall that we can’t really expect to repeat) has only grown by between 8% and 11% over various 7, 10, and 12 years. And from 2010 to 2015, before YPF was even in the picture, TBV/share grew by just 5%/year. While the YPF proceeds alone, should they be paid (a big “if”), account for more than all of Burford’s enterprise value, the most committed bulls seem to believe the stock is only pricing in the value of Burford’s non-YPF business (i.e. “you are getting YPF for free”). I don’t agree. Ex. YPF, Burford’s stock trades at 4x TBV. Having grown TBV by just 8%-10% historically, why should they be valued at such a lofty multiple?

Lamb Weston is the largest frozen potato processor in North America, with 40% share of a market dominated by 3 players, all of whom have origins dating back to the early 1900s. More than 80% of its production is concentrated in Oregon, Washington, and Idaho, giving it more exposure to the highest quality crops than Simplot and especially McCain, who compared to Lamb are more heavily skewed to the Midwest and East Coast.

Over the last decade, Lamb Weston has generated ~high-20s pre-tax returns on capital. Why couldn’t a new entrant compete these mammoth returns away? Well, what management and industry folks will often say is that even assuming a new entrant had access to the ~$500mn+ required to build a processing plant, they’d have to somehow dislodge the decades-long relationships that the big 3 have cultivated with farmers and customers. In 2016, Lamb disclosed the average duration of its customer relationship to be 28 years, with its longest going back 45 years. Meanwhile, Lamb’s average farmer had been growing for them for 15 years, 35% of them for 20 years. Also, new plant builds are usually anchored by volumes from a major QSR. For McDonald’s, french fries are a menu item they absolutely can’t screw up, so why roll the dice on a new processor? In securing QSR volumes, the big 3 enjoy scale production economies and procurement savings on key processing inputs that a newcomer does not.

Of course, this doesn’t immunize Lamb’s earnings from volatility. The abnormally hot summer in fy21 produced potatoes with unusually low starch content, which on a largely fixed cost manufacturing base, resulted in higher per pound processing costs, and forced Lamb to buy potatoes in open market at huge premiums to meet volume commitments to customers. Rising potato prices, along with labor shortages and double-digit inflation in transportation and oil costs, caused Lamb’s margins to contract significantly in fy22.

Lamb successfully pushed price through to its customers, recouping incremental costs from the heat wave and supply chain shortages. It was able to do so because frozen potato processing capacity in North America has been very tight over the last 7 years, well above the historical range of 93% to 97%. The 5.6bn incremental capacity that the industry is expected to add through 2027 supports strong utilization assuming demand grows between 2% and 4%. But that’s hardly a given. USDA data shows several 5-year stretches where per capita demand was flat-to-down 1%. In that scenario, capacity utilization would fall all the way down to 89%. By my estimate, it appears we are looking at ~10% more capacity in North America, outpacing lsd demand growth. Lamb Weston would be more exposed than others because its idiosyncratic volume challenges – the purposeful shedding of 4 low-margin contracts and a botched ERP rollout resulting in unfulfilled orders, which exacerbate headwinds from deteriorating restaurant traffic – suggest its capacity utilization is likely starting below that of peers.

I bought some XPEL shares in March and wrote some nice things about them. Naturally, soon after, the company reported an awful quarter and the stock cratered. Management cited broad aftermarket weakness in the US – “it was not uncommon to see dealers who were down 10%, 15% in the first quarter from the prior year period” – and a horrendous 78% revenue collapse in China.

But there were some silver linings: 1) port delays in the US caused a ~20% reduction in sales of Porsche’s and Audi’s, two of Xpel’s top brands for film coverage, and this disruption was resolved toward the end of the quarter, perhaps explaining Xpel’s atypically strong m/m growth in April; 2) outside of the US and China, Xpel continued to grow at an impressive clip, as did 3) revenue from Installation Services, where Xpel realizes revenue from selling and installing film itself.

IS growing 35% despite double-digit declines in retail implies really strong growth from the new car dealerships and OEMs that make up the rest of this segment. I think this is an important point, one that is easy to overlook. A key unresolved matter for the bull case is whether PPF adoption can spread beyond enthusiasts. That Xpel continues to report strong growth at auto dealerships and OEMs, two critical channels for reaching mainstream car buyers, is evidence that it might.

CEO Ryan Pape again directly addressed the allegation that a disproportionate amount of revenue comes from Tesla:

“There’s this idea that all of the revenue is concentrated in one brand or 2 brands or something. And that’s really not the case. I mean, I think we talked about the type of make related concentration last year, like 5% or less…I really just can’t stress enough that there isn’t a single point concentration risk into any one vehicle in this business”

I later followed up with Ryan. One key point from my conversation with him: about 30% of Xpel’s revenue comes directly from dealerships or from aftermarket installers who work only with new car dealerships. None of these installers or dealerships work on Tesla’s and none of them will be found on Xpel’s “Find An Authorized XPEL Installer” tool that both the short seller and I used to source leads. So, if your diligence consists of calling aftermarket installers listed by Xpel and asking “what percent of your installations are Tesla’s”, you are missing 30% of revenue for which the answer is “0”.

The market for fixed income trading platforms has consolidated into an oligopoly, with MarketAxess, Tradeweb, and Bloomberg at its center. A number of other competitors have emerged over the years, some are still around (Trumid), others have failed (Bondcube, Algomi). But, for the most part, when an asset manager like PIMCO buys Treasuries or corporate bonds from a sell-side dealer or even another buyside participant without picking up the phone, more likely than not they are doing so through one of those 3 platforms

When I first wrote up MTKX and TW in November ‘20, both companies looked like inevitable winners as bond traders flocked to their electronic platforms in search of liquidity. Since then, their results have diverged starkly. Through net spotting, Tradeweb successfully leveraged its Treasury franchise to claim significant volume in high-grade credit. It was also early to market with Portfolio Trading, a protocol that allows a large collection of bonds to be bought and sold at a single net portfolio-level price. PT’s growing popularity has coincided with the ascent of fixed income ETFs, as the ability to efficiently trade large bundles of securities in one go is especially useful for market makers involved in the creation/redemption process, where ETF shares are exchanged for the cash bonds underlying them.

MarketAxess also began offering its own version of Portfolio Trading but never took it as seriously as Tradeweb, fixated as it’s long been on pushing Open Trading, which allows all market participants to anonymously trade with one another. Since launching in 2013, OT has become the central point of differentiation for MarketAxess, intermediating ~34% of its volumes. It is their ambitious attempt to create a new market structure, one that they hope will come subsume all major protocols and fixed income asset categories. OT tends to thrive in high vol environments, when liquidity is scarce. But if the last decade is any indication, low volatility appears more the norm than management would like to admit.

That MarketAxess has fallen so far behind Tradeweb in PT and so aggressively pushes OT also points to a philosophical difference between how the two platforms approach the broader ecosystem. Perhaps as a result of its origins as a dealer-backed consortium and its substantial dealer-to-dealer activities, Tradeweb has always worked more in harmony with the existing, dealer and phone-dominated ecosystem. MarketAxess, on the other hand, has never never been shy about placing themselves at the center of the ecosystem, with dealers and investors serving as spokes around the Open Trading hub. I suspect that by pushing OT so doggedly, MarketAxess alienated broker-dealers and neglected protocols, like Portfolio Trading, that depend on them, creating an opening for Tradeweb, who has always maintained a less revolutionary, more cooperative posture.

This multi-part series concerns the building materials (BM) industry, specifically the layer downstream of timber growers and upstream of home builders, home centers, and remodelers. Investors applaud canonical compounders like NVR and Home Depot and have in recent years been losing their minds over Floor & Decor. But beneath that strata of the value chain is a thriving ecosystem of manufacturers and distributors that is rarely discussed by generalists or even dismissed as unworthy of study.

With lumber prices soaring during COVID, the last few years have been pretty wild for those – like BLDR, BXC, BCC, and LPX – most geared to the vicissitudes of commodity wood pricing. BLDR and BXC free cash flow’ed 1.6x and 3.8x their 2019 year-end market caps, respectively, in just 2 years!

A big chunk of the post explores the causes of soaring lumber prices during COVID and quantifies the extent to which the US housing market remains in deficit. Towards the end, I discuss BlueLinx, a “two-step” distributor that sources wood products from mills and distributes them to lumber yards and home centers, who in turn re-sell to builders and contractors. BlueLinx has had a long and troubled history since it was taken public by Cerberus in 2004. With 4 turns of leverage on peak earnings, the company spiraled into near oblivion when the housing crisis hit.