[TripAdvisor, Trivago, OTAs] Thoughts on the Carnage

Posted By

scuttleblurb

On

In

SAMPLE POSTS,[TRIP] Tripadvisor,[TRVG] Trivago |

1 Comment

Trivago’s “relevance assessment dimension”, implemented in late 2016, is an algorithmic adjustment that compels hotel advertisers to improve their landing sites and booking engines if they want to rank higher in trivago’s search results. The idea is that while the user experience starts with a room search on trivago, it extends to when she clicks off to actually book the room on the advertiser’s site…so if the advertiser screws up that last step (according to trivago), it will have to pay more for each referral. One consequence of this change was that trivago penalized OTAs whose links sent users to yet another page of search results on OTA.com rather than directly to the property that the OTA listed on trivago.

While trivago technically has 200+ advertisers competing for placement in its marketplace, two of them, Expedia and Priceline, respectively comprise 36% and 43% of the company’s revenue. [Expedia acquired 63% of trivago from early investors in 2013 and continues to own 60% of the company post its December 2016 IPO]. It’s usually not a good idea to behave like a powerful aggregator towards two dominant customers who actually are powerful aggregators when you, actually, are not…but that’s essentially what trivago did, tasking its algorithm to extract the most value from advertisers in zero-sum fashion while providing CRM, bidding, and booking tools for smaller hotels – including “express booking” where trivago actually hosts the booking site on behalf of the advertiser – to compete more effectively against the OTA giants with the aim of stoking greater bid density and pushing the agencies, in trivago’s own words, towards “the pain points of their profitability targets.”

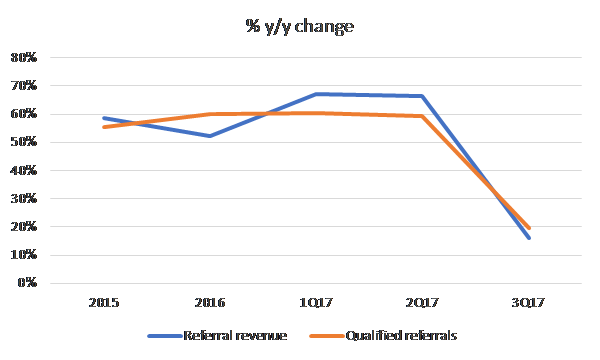

In the first several quarters after implementing relevance assessment, trivago saw qualified referrals ~+60% y/y and revenue per qualified referral (RPQR) growth of +4%-4.5%. The company admonished that RPQR would be lower (or, euphemistically, “normalized”) in the second half of 2017 since as advertisers adapted their sites to trivago’s relevance assessment standards, they would be not be required to bid as much for traffic. No big deal. But then things took a turn for the worse. On 9/6/17, trivago announced that revenue growth for the full year would be more like 40% instead of 50% and EBITDA would be lower than guided too, as the RPQR hit turned out to be worse than expected.

The charitable interpretation to this bleak outcome, the line that management continuously parrots to investors, is that by optimizing the user experience, trivago is nobly sacrificing near-term profits for the sake of long-term gain. Management understands that having loyal users is the key to spinning up a platform that gives you license to marginalize suppliers (advertisers, in this case), and so trivago is splurging on TV advertising [over 90% of the company’s revenue is dedicated to sales and marketing], assiduously monitoring the results, and iteratively tweaking campaigns towards the aim of building brand value. At the same time, by adjusting its bidding algorithm and forcing suppliers to play ball, it is ensuring that users have the most seamless search and booking experiences possible.

But it’s not clear to me why Trivago feels uniquely positioned to accomplish the task of creating memorable ads or whatever it is that they think drives persistent site visits. Because unlike, say, a SaaS model, where the journey from site visits to free trials to paid subscriptions sucks the user into ever deeper states of captivity that can, in theory, generate sticky, layered recurring revenue streams, what is the lock-in mechanism here? At least TripAdvisor can claim authentic and current user-generated reviews. Google began with a superior mousetrap and didn’t need to spend gobs on advertising to attract users (plus, because general search is so frequently used, it is habit-forming in a way that travel-specific search is not). Trivago’s vertical search has, well…what exactly…to keep users continuously coming back once they have clicked off the site? And furthermore, what can’t be replicated? Expedia offers its own version of relevance assessment, its Accelerator program encouraging hotel properties to graduate up the Expedia listings page by paying extra commissions or by improving quality scores.

Growth in qualified referrals and referral revenue have decelerated in dramatic fashion. No bueno:

[Definition of qualified referrals from the F-1: “We define a qualified referral as a unique visitor per day that generates at least one referral. For example, if a single visitor clicks on multiple hotel offers in our search results in a given day, they count as multiple referrals, but as only one qualified referral. While we charge advertisers for every referral, we believe that the qualified referral metric is a helpful proxy for the number of unique visitors to our site with booking intent, which is the type of visitor our advertisers are interested in and which we believe supports bidding levels in our marketplace.”]

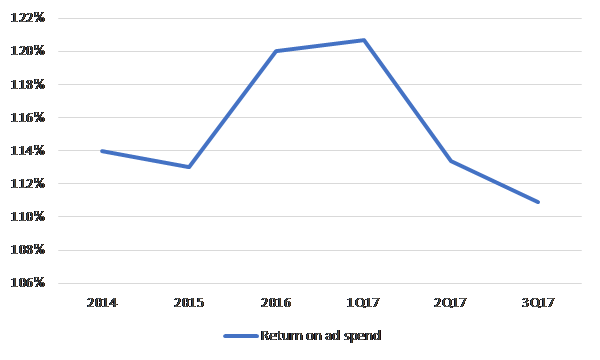

And with that, the potency of trivago’s brand advertising also appears to have waned, as the company experienced significant y/y de-leverage on sales and marketing in the latest quarter and declining returns on ad spend over the last 2 quarters:

ROAS weakness also happens to coincide with TripAdvisor’s renewed commitment to brand advertising this year, so on top of volume weakness, perhaps TRVG is also witnessing pricing pressure on ad units? [After spending $51mn on TV advertising in 2015, TripAdvisor reallocated marketing dollars to online search and spent nothing at all on TV in 2016. They’re committing $70mn-$80mn this year as part of a multi-year brand ad campaign].

If online travel were fragmented up and down the value chain, then being the first to spend aggressively on brand advertising for the sake of creating a liquid marketplace that then itself becomes the value proposition, might just work. The numbers are tempting. Global online hotel bookings of ~$145bn comprise around 1/3 of the total offline + online hotel bookings and are taking share from the offline channel. At a 15% take rate, that’s a $22bn addressable market growing low double-digits annually. On its current revenue base of $1bn, claiming even a small share of that could drastically move the dial. But the question of course is, can you grab share at compelling economics? I don’t understand the fundamental value proposition offered by trivago that cannot be offered equally well by many other top-of-funnel peers or even further down-funnel for that matter.

This is why I find I Trivago’s competitive positioning so precarious: it doesn’t possess the bargaining power to procure traffic at advantaged cost nor an irreplicable process to transform that traffic into value so compelling and unique that even their powerful customers will cede economic ground. Online travel is increasingly dominated by aggregators further downstream who have myriad acquisition channels – including Facebook, Google, and direct brand advertising – through which to lure travelers. And as in any highly competitive market, attempting to generate sustainable value off brand advertising is an unwinnable game unless there is a differentiating resource at the core.

At the Citi Tech Conference last month, when asked about competitors recently copying trivago’s strategy, the company could offer only the following effete non-statement:

“I think the only sustainable competitive advantage that you can have is to continue to be ahead of your competition. And so, the competitive response is to continue to innovate in marketing and in product and make sure that there is always a gap between yourself and competitors that are copying what has worked very well for you. I think that sounds generic, but I think that’s the only thing you can do.”

TRVG’s management maintains that its can sustain 25% EBITDA margins at some point (better than Expedia’s high-teens EBITDA margins). I doubt it.

TripAdvisor is the Twitter of online travel: a unique, hard-to-replicate asset that eludes monetization but has significant strategic value. There’s clearly a double marginalization problem to be solved via vertical acquisition, which TRIP Chairman Greg Maffei seems open to. And that might really be the primary reason to hold on to the stock. Well, that, plus the non-hotel side of the business (attractions + restaurants) is killing it, growing revenue by 25%-30% over the last year and solidly profitability. That business is probably worth ~$1.5bn (4.5x revenue), leaving $2.4bn in enterprise value for a hotel business, one facing revenue and cost pressures, doing around $200mn in EBITDA (after stock comp). By comparison, trivago’s enterprise value is $1.8bn, and they’re doing only $13mn in EBITDA. The value disparity makes little sense.

[Re: “hard-to-replicate”, as I previous wrote:

“Over 360mn people visit the company’s site every month to plan their trips because they trust its deep fount of nearly 500mn authentic and current user-generated reviews and 90mn photos on 7mn hotels, attractions, and restaurants. Those travelers, upon completing their trips, post their own reviews, contributing to a burgeoning body of shared knowledge that drives traffic through better search engine rankings and compels still more potential travelers to visit Tripadvisor at the start of their research process. The company further stokes participation by offering badges and other marks of distinction to particularly helpful and active reviewers. Hoteliers, well aware of Tripadvisor’s critical top-of-funnel role, make a special effort to respond to consumer reviews. If you’ve stayed at a hotel boutique, you will have no doubt been encouraged at some point to leave a review on Tripadvisor by the hotel manager, who often proudly plasters the property’s Tripadvisor rating on the front window as a point of differentiation. It would be monstrously difficult to recreate the breadth and depth of TRIP’s reviews.”]

[“Monstrously difficult”? A bit hyperbolic on my part. In theory, I guess I don’t really see why the Priceline, which already has over 135mn hotel reviews, couldn’t expand its share as it garners more direct traffic through brand advertising]

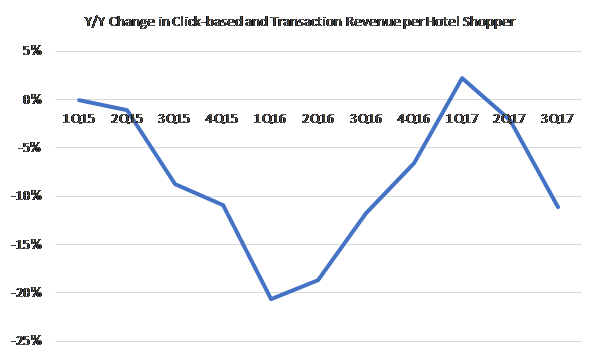

In prior quarters, the y/y decline in TRIP’s revenue per hotel shopper was largely attributed to a mix shift from desktop to mobile, a concern alleviated by the hope that mobile monetization improvement would eventually overcome such dilution. But now, bid-downs by Priceline, which is shifting ad dollars to brand advertising after years of diminishing ROI on performance marketing, have whacked monetization on the desktop side and confounded several quarters of positively inflecting trends.

After a two-year hiatus, TripAdvisor also recently began splurging on TV advertising…so, on top of getting hosed by its largest customer on the revenue side, TripAdvisor is now competing with Priceline for TV ad spots as both pursue a common goal of driving more direct traffic to their own sites. It’s hard not to be cynical about TripAdvisor’s standalone role in the value chain.

So, with trivago implicitly raising bid prices and both trivago and TripAdvisor trying (and, in the latter case, failing) to encroach directly upon bookings, it appears that Priceline is finally saying “nuh-uh” and using bid downs as part of a bargaining tactic to keep suppliers in check. Whether the shift from performance to branded advertising is structural seems inconclusive. Recent comments from Priceline CEO Glenn Fogel:

“I think one of the things very important to recognize is the dynamic nature of how the performance marketing works. So while we can make change in terms of how much money we want to spend and we where we want to spend it, our partners are also making changes all the time, and other people and auctions are making changes. So, this is dynamic and interactive, so it’s difficult to project long term what’s going to happen.”

Still, Priceline has been talking about pressure on performance ad returns for some time and even as Expedia professes loyalty towards trivago as an acquisition channel, it admits that meta search generates lower “repeat propensity” than search engine marketing. In any case, what seems abundantly clear is that TripAdvisor and trivago, who derive 46% and 79% of revenue, respectively, from Priceline and Expedia, are really in no place to dictate terms. Generating extra-normal profits as standalone entities, like the kind implied by the obligatory “small x% of big $TAM” exhibit that these guys all like to use, requires TRIP and TRVG either claiming a fair share of extraordinary surplus or an unfair share of modest surplus. The absence of a uniquely compelling value proposition impedes the former; industry structure constrains the latter.

Implicit in my TRVG/TRIP bashing, however, is that value in the this industry accrues a level below and in that spirit, Expedia could be interesting. EXPE sold off last week as the company noted that its cost structure would be larded with investments related to accelerated hotel on-boarding [3 years ago, EXPE was adding 25k-30k hotels / year, this year it’ll be 80k, and will “step change” in future years], cloud computing [a 2-3 year transition. $100mn this year, much greater than management’s guidance a year ago, growing by over 50% next year], and marketing [as management turns its attention to deepening local marketplace liquidity after years of broad-based acquisition].

Expedia isn’t the cleanest company with the strongest moat – the core OTA is dependent on Google for traffic and faces competition from a consolidating supplier base, HomeAway is up against AirBnB, tech stack integration across a slew of acquisitions appears to have been sloppy – but as the second largest OTA by bookable properties next to Priceline, the company has certainly crossed the threshold of critical scale and fostered a sustainably profitable two-sided marketplace. Disintermediation concerns stemming from an increasingly consolidated supplier base and worries about Google/Facebook aggressively moving into the space, have plagued OTAs for years…but Priceline and Expedia have done just fine as continuous investment in technology, marketing, hotel relationships, and vigorous A/B testing have congealed into a hard-to-replicate value proposition for suppliers looking to offload inherently perishable inventory and travel shoppers looking to dependably source the broadest, most relevant selection at the lowest price, with increasing participation on each side of the platform begetting buy-in from the other.

When I strip out trivago and stock comp (see below), it looks like Expedia is trading for around 11x EBITDA and 17x FCFE, which seems reasonable to me even if we grant that EBITDA growth will slow to the bottom end of the +10%-20% range (or even somewhat below) for the next few years on accelerated spending…and it looks quite cheap if we think that by weaning itself off acquisitions, dedicating itself to organically deepening engagement, broadening the platform through aggressive on-boarding, and boosting overall productivity by partly shifting its tech infrastructure to the cloud, Expedia can drive accelerated bookings growth and margin expansion 3 years out. At the very least, I think we can be far more confident that Expedia’s investments offer a reasonable return than that trivago’s continuous spending on TV commercials will ignite sustainable platform activity.

($ millions except per share data)

EXPE TEV ex. TRVG cash

19,159

TRVG stock price

$ 7.17

x # TRVG shares owned by EXPE

209

=

1,499

Adj. EXPE TEV

17,661

EBITDA ex. TRVG

1,589

multiple

11.1x

FCFE ex. TRVG

1,249

Stock comp ex. TRVG

135

EXPE FCFE ex. TRVG ex. stock comp

1,114

/share

$ 7.06

multiple

17.4x

You can also own Expedia through Liberty Expedia (LEXEA), which owns 15.5% of Expedia’s common stock representing a 51.9% voting interest in Expedia…but, I don’t think there’s a compelling “arb” here. LEXEA split off from Liberty Ventures a year ago for the purpose of Expedia eventually purchasing LEXEA’s EXPE shares. Liberty Expedia also owns an internet retailer of health and dietary supplements called Vitalize (formerly known as Bodybuilding.com), which, based on declining revenue and profits, isn’t doing so hot, and has deteriorated to such an extent that it is small enough to be unceremoniously lumped into “corporate and other”. It does around $316mn in trailing revenue with negligible OIBDA.

You are getting 0.41 shares of EXPE for every 1 share of LEXEA that you own. LEXEA also has around $5.40 in net debt / share. So the NAV breaks down like this…

NAV

Expedia

$ 50.43

Net debt

$ (5.36)

Vitalize

???

Total

$ 45.07

…vs. LEXEA’s current share price of $46. The delta between NAV and the LEXEA share price values Vitalize at around 0.2x trailing revenue. Seems fair. Whatever.

Priceline’s stock also sold off post-earnings on decelerating bookings (from ~mid-20s y/y ex. fx growth over the last 4 quarters to 16% in the latest quarter). While size constraints may translate into slower growth relative to the past, there’s plenty of runway ahead. Its largest online property, Booking.com, has an insurmountable moat in a fragmented European market [in Europe, independent lodging comprises 67% of total rooms vs. 30% in the US] where I estimate it claims around 40% of European online accommodation bookings, or about 20% of total European bookings. Globally, Priceline’s ~$80bn of total gross bookings is just 20% of online hotel bookings, or about 6%-7% of total online + offline. Room nights +19%, the number of bookable properties +41% (including vacation rentals +58%) during the most recent quarter, and the meta properties, Kayak and (more recently) Momondo, are growing and profitable. OpenTable, on which the company took a huge impairment charge last year, has sucked, but I think we’re past that. I don’t see any meaningful impediments to Priceline continuing to grow its cash earnings per share by mid-teens+ for the foreseeable future.

So yea, setting aside the takeout aspect for TripAdvisor and just evaluating these companies on their standalone long-term value creation potential, I would rather own Priceline (17x EBITDA backing out long-term investments, including Ctrip) or Expedia (11x), respectively, than either Trivago (NM) or TripAdvisor (17x).

[MTCH] Match Group

Posted By

scuttleblurb

On

In

SAMPLE POSTS,[MTCH] Match Group |

No Comments

Online dating has easy parallels to other online social experiences that if taken too seriously can lead to dubious outcomes. A dating app is like social media in that there are lots of people broadcasting themselves, making connections, and seeking validation. You might “like” a photo on Instagram as you might right-swipe on a photo in Tinder or Bumble. So as Tinder, Match Group’s largest property – accounting for 66% of paying users (”payers”), 60% of revenue, and 80% of EBITDA – ballooned to ~75mn monthly active users, it must have seemed only natural to consider human relationships in a more abstract, all-encompassing way. They could not only mediate romance but “social discovery”, “interest groups”, and eventually, “social entertainment”. They could foster connections that “span geographies, demographics, relationship status and genders in ways that dating services cannot, effectively providing a much larger addressable market than dating”.

Source: Match Group; 1q21 Investor Letter

When Meta began to push entertainment over friend graph content and talk a storm about the metaverse, Match maybe felt that that was something they should think about too. Those thoughts eventually crescendo’ed into the $1.7bn acquisition (8x revenue) of Hyperconnect in 2021, the largest in its history. Hyperconnect got 75% of its revenue from Asia and operated through 2 brands: Azar, which enables one-to-one live video chat, and Hakuna, a multi-party live streaming app. Its advanced video technology could, Match believed, create a “metaverse-based experience” for social discovery and be integrated into its portfolio of apps. Meetic, a European dating app owned by Match, used the technology to launch “Live Rooms”, where small groups of people could hang out and shoot the shit. In Hyperconnect’s “Single Town”, user avatars ambled from one virtual location to the next. We now know that these metaverse ambitions, which may have seemed reasonable in the disco fog of the post-COVID orgy, were a massive overreach.

The expansion never made much strategic sense. Match was trading off a dominant position in the growing niche of online dating for a subscale position in the amorphous expanse of social media, where it was pitted against impossibly strong competitors. And you can see how an app with a reputation for facilitating hookups, when combined with a virtual goods economy and video streaming, could degenerate into a pretty unsavory place.

More than that though, people appear to want to represent different selves in different platforms. The stuff one feels comfortable sharing with potential mates on Hinge will differ from stuff they share with friends on Facebook or with colleagues on LinkedIn. Facebook Dating, which can pull in Instagram Stories and add Instagram followers and Facebook friends to “Secret Crush” lists, has famously flopped since launching in 2018. Hinge, the second largest Match property, contributing 8% of payers and 11% of revenue, soared even after it stopped leveraging Facebook’s social graph to match singles. Bumble’s derivative offerings – Bumble BFF for discovering platonic friends and Bubble Bizz for developing professional relationships – don’t appear to have gotten much traction.

In short, dating apps have failed to compete with other social graphs on their own terms and IRL friend graphs don’t appear to bring meaningful advantages to online dating. This doesn’t mean certain social media mechanics can’t be carried over to dating apps. Tinder’s “Explore” tab, where users are organized by shared interests and relationship intent, seemed like a reasonable idea: a low risk way to efficiently sort matches on an app where users typically don’t provide any profile information beyond photos. But it was designed in the spirit of casual virtual hangs and hasn’t made any lasting impact on Tinder’s flagging user growth.

Dating apps are a utility. Where they go wrong is in positioning themselves as social hubs rather than as tools that take the burden off tired swipe thumbs. The functional orientation of dating apps is reflected in the way they monetize. Facebook is concerned with remaining relevant to younger audiences only in the sense that engagement drives ad revenue, so they’d rather have more of it than less. They aren’t thinking about demographic mix through a zero sum lens. Because Meta can personalize what it injects into a user’s feed, it is the amount of relevant content that matters, not the relative mix of men vs. women or young vs. old on the platform per se. So the two-sided network effects of social media are instantiated as engaged users on one side and advertisers on the other.

By contrast, the two-sided network effects in dating apps are expressed within the user base itself. The vast majority of revenue that any dating app realizes comes from men, who outnumber women by ~2x-3x1[2] and pay in order to improve their odds of securing dates with them. While engagement matters, where that engagement comes from is just as important. Dating apps try so hard to create compelling experiences for women for the same reason that bars offer them free drinks and bouncers block you and your boys even as they wave in a large bachelorette party. Single men will swipe right on just about anyone. There is no need to cater to them. If anything, barriers are required to keep them from upsetting the gender balance too much and bumming out women, who are not only fewer in number but tend to be far more parsimonious with right-swipes besides.

Tinder popularized a number of features that catalyzed its explosive rise just as smartphone adoption was taking off. Sparse profiles requiring nothing but photos made it easy to onboard. A freemium revenue model made it easy to trial. The “swipe” was suited to casually filling interstices of time throughout the day. But just as critical to Tinder’s success was the double opt-in feature, where both parties had to swipe right on each other before private messaging could commence, a feature that helped dam the deluge of unwanted messages from random guys, which was a big problem for women on Gen 1 desktop dating sites like Match.com[3] and OkCupid (though this continues to be a major issue, with ~2/3 of women under 50 on dating apps experiencing harassment[4] in one form or another).

So with online dating, we have a setup where men, fueled by the dopamine release triggered by the variable rewards that come from the unpredictable timing of matches, compete with one another for the prize of securing dates with a scarce supply of women. This looks an awful lot like gaming. In this Time article[5] from 2014, Tinder’s co-founder Sean Rad explains “We always saw Tinder, the interface, as a game….What you’re doing, the motion, the reaction.” You might even hypothesize that gaming is an outgrowth of the same competitive instinct, honed through evolutionary pressure, required to win mates. It then seems natural that Match’s latest CEO, Bernard Kim, spent 6 years at Zynga and close to a decade at Electronic Arts, and that before Bernard came on board, Match was replicating monetization dynamics pioneered by online gaming.

There was a time when online games made money through a “play to win” model where players had to purchase expansion packs and fancy gear to stand a realistic shot of advancing. But buying your way to victory seemed unfair and today most monetize through a combination of advertising and cosmetic in-game purchases that enhance a player’s experience without improving their chances of winning. Advertising never took hold in online dating. It’s a tiny part of Tinder’s revenue. I guess there’s not much data to target against. On the other hand, a la carte (”in app”) products are a meaningful source of revenue for Tinder, comprising ~25%-30% of its total. But unlike skins purchased in an online game, Boosts (which allows you to be one of the top profiles in your area for 30 minutes) and Super Likes (a blue star you can tap on someone’s profile that lets the other person know you really like them and prioritizes your profile on their card stack) in Tinder are purely functional.

The most enduring gaming franchises have avoided the hit driven paradigm that used to characterize the space by fostering communities. A gamer can earn status in those communities by procuring badges with skilled play or even by purchasing expensive skins that signal commitment or whatever. Dating apps aren’t like that. These are utilities, not communities. There is no signaling value or bragging rights to securing dates. The rewards from doing so are private. And I’ve got to imagine that spending boatloads of real money on Tinder Coins that you use to acquire virtual collectibles and buy your way to the top of card stacks could backfire? You don’t want to appear desperate or mark yourself as someone who takes online dating too seriously. That’s a turn off for women. There’s a reason your subscription status isn’t displayed on your Tinder profile and I can imagine that Boosts and Super Likes might dilute your prospects if women know you purchased them. I suppose part of the reason everyone on Tinder has a quota of Super Likes, regardless of whether they buy them or not, is so it’s not obvious to someone who receives one that the sender paid for it.

The analogy to gaming breaks down in a more fundamental and obvious way. There are no skills to master. Interesting photos that highlight facets of your personality can move the needle a bit, but whether you are right-swiped or not is primarily a function of your physical attractiveness relative to that of the swiper. In real life, where there are opportunities to flex other assets besides looks – intelligence, sense of humor, kindness, social status – over a sustained period, whether that be at school, with friends, or in the workplace, you will find plenty of couples who are mismatched on attractiveness. But in raw stranger-to-stranger encounters, particularly on Tinder where pictures are pretty much all you have to go on, physical appearance will be the dominant filter.

It used to be that Tinder assigned you a desirability score based on the mix of right and left swipes you received relative the scores of users swiping you, among many other factors. Users with similar scores made their way to each others’ card decks. Eventually, as Tinder scaled and accrued more user data, that competitive ranking system gave way to one where users in your card stack are similar to those who were right-swiped by people who tend to right-swipe the same profiles as you, which is apparently how Hinge matches users[6] too. In either case, though, you more or less end up in a matching pool with people who are comparably desirable. And that’s a good thing. If you’re a 2 in the looks department, you do not want a card stack of Margot Robbie’s. You may think you do, but you don’t. You may as well spend your time rating photos on “Hot or Not” because you will almost never get right-swiped. Online dating is nice in that it conveniently introduces you to mates while removing the embarrassment of in-person rejection. It also creates a rather efficient market that kills the dream a little for everyone.

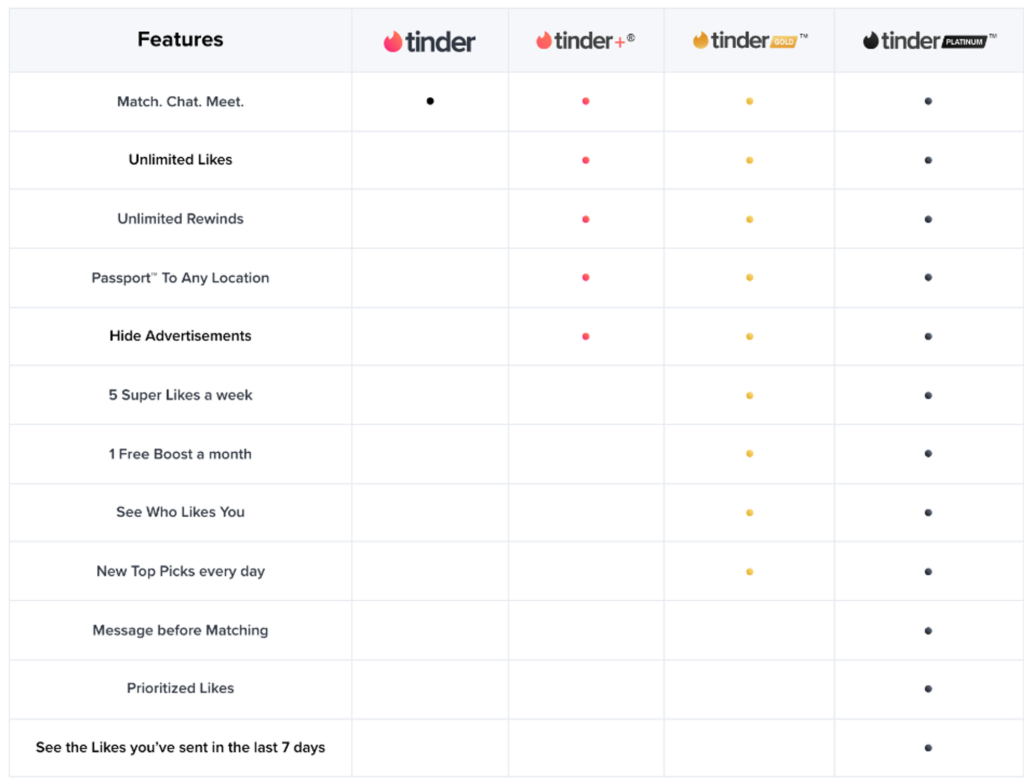

Within algorithmically determined matching constraints, Tinder is still monetizing off similar “pay to play” tactics that gaming companies abandoned due to the deleterious effects on the broader ecosystem. The analogy here isn’t great, as ~3/4 of Tinder’s revenue comes from subscriptions, whose benefits include things like “unlimited rewinds”, “see who likes you”, “passport” (where you can match with users in other cities), and “hide ads” that shouldn’t degrade the experience for other users:

But Super Likes, Boosts, and Unlimited Swipes – which are bundled into subscriptions, with Superlikes and Boosts available as a la carte purchases to boot – crowd out consideration for non-paying users and disrupt the match order that Tinder’s algorithm might otherwise find optimal.

Of course, social media also wrestles with an inherent tension between monetization and user experience. But compared to Instagram, which has as many ways to keep users engaged as there are varieties of entertaining content (not to mention, a relevant ad can be as compelling as organic content), a dating app has far fewer moves on a far smaller surface area. There are this many singles in a 10-20 mile radius and the job is to match those singles as efficiently as possible. That’s pretty much it. The post-matching experience is unpredictable and entirely outside Tinder’s control. There is no date rating system. You can understand why Tinder and others were tempted by metaverse experiences. And monetization is confined to short-term subscriptions and boosts because users don’t expect to spend a year or even months on a dating app, even if they ultimately do. This goes hand in hand with the classic tension of online dating as a business. The better the service is, the sooner you’ll be off it, and so subscribing on an annual basis feels like paying more for a worse product. That’s why “churn”, while almost certainly through the roof, isn’t relevant in the way we traditionally think about it. Even Tinder subscriptions feel less like subscriptions than they do product sales.

The other challenge is that while match liquidity begot by network effects is the governing moat for a dating app, it doesn’t lead to winner take all outcomes as there are many vectors along which network effects can be spun. While Tinder may be the largest dating app on the market, with 8x as many payers as Hinge and 4x as many as Bumble, it co-exists alongside a very long tail that encompasses a wide variety of apps catering to different races, religions, sexual orientations, and sensibilities. Even mainstream competitors like Hinge and Bumble successfully counter-positioned against Tinder by emphasizing serious relationships. Hinge (”designed to be deleted”) requires responses to prompts and demands 5 times the 3-4 minutes it takes to sign up for Tinder. Bumble is like Hinge but with strong brand messaging around women’s safety and empowerment that is reinforced by product mechanics (women are required to send the first message).

Dating apps inspire no brand loyalty. They aren’t held together by friend or interest graphs that keep users from experimenting with competing apps. People will typically multi-home across 3 or 4 apps at once, re-creating network liquidity across them to some degree. Features like voice texts, video, badges signaling seriousness of intent are easily replicable. All this has created the conditions for an unstable industry structure, with market shares radically shifting every few years, as chronicled in this video[8] from Data is Beautiful.

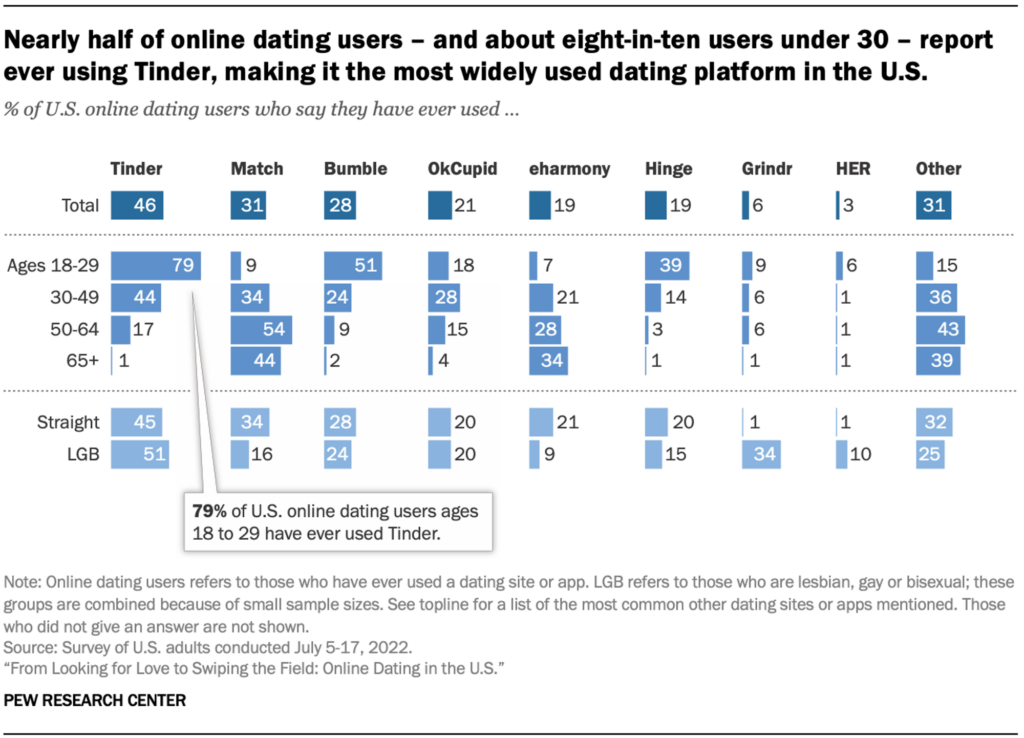

Since it was incubated within IAC in 2012, Tinder has gone on to become the most popular global dating platform, with around 75mn monthly active users (to put this in perspective, in the year of the iPhone’s debut, the largest dating site, Plenty of Fish, had about 8mn MAUs). According to Pew Research, 46% of US online dating users, including 79% of those between the ages of 18 and 29, report having used Tinder at some point:

But like so many apps before it, Tinder too is now wrestling with stagnant user growth. They are trying to combat this headwind by appealing to Gen Z users and women who might otherwise be drawn to more substantive connections on Hinge and Bumble, with marketing campaigns that de-emphasize its reputation as a casual hook-up app. But brand marketing that tells users what you hope to be known for will not work if the product is still grounded in low-friction onboarding and shallow swipes, and altering the core product or requiring users to invest more time on profiles upfront risks alienating existing users and further constricting top-of-funnel growth.

With a series of CEOs and product managers arriving with a plan to revitalize what they correctly recognized as a stale user experience and then resigning after failing to do so, it’s hard to escape the feeling that Tinder may just be out of moves when it comes to user growth, that Match’s most significant cash cow is now in senescence, following the all too familiar path of every other dating app that exploded in popularity only to slip into irrelevance. Management has long talked about optimizing for revenue rather than either payers or revenue-per-payer per month (RPP). Even so, bears will point to the mix of revenue growth increasingly coming from RPP at the expense of payers as evidence that top-of-funnel expansion and payer conversion have gotten much harder to come by. They will say that Tinder has matured to point where a greater mix of revenue growth must now come from extracting more value from the payers it already has.

A salient example of this is Tinder Select, a $500/month membership tier that was rolled out to the most active 1% of users in September. By now, we’re all familiar with the extreme tail in mobile monetization. In gaming, a small fraction of users will spend boatloads on cosmetic features for status and social connectedness. The top 1% accounts for half a publisher’s revenue or whatever. But I’m not sure think Tinder is amenable to nearly the extreme monetization tails you see in gaming. There are no status awards to win, no community to impress, and limits on how much Tinder can improve your matching prospects or date experiences. And if Tinder Select is that good at matching you with the right mate, well, you’re not going to be paying for very long. From an avid payer base of ~104k (1% of 10.4mn total payers), how many actually go for this and over what stretch of time? Do you get to, say, $50mn (5% of LTM EBITDA) by assuming 10k members at $500/month for 10 months? 20k members at $500/month for 5? My intuitions fail me here.

The concern is not that the online dating market is tapped out but that the subset of users drawn to casual swipe mechanics largely is, and management’s range of motion is constrained by the casual, low friction on boarding that made Tinder such a viral sensation in the first place. Over the years, they’ve introduced all sorts of initiatives (Swipe Night[9], Explore, Hot Takes[10], Vibes[11], video chat, the “Starts with a Swipe[12]” marketing campaign) whose impact on engagement, while promising at first, ultimately proved ephemeral. Tinder can play around with different monetization tactics on a given set of product features, but this only goes so far. At some point they’ll need to find durable, product-led ways to expand the efficient frontier, improving match quality and swipe efficiency across the board, expanding the top-of-funnel by appealing to Gen Z users, and attracting more women so payers can enjoy higher hit rates without unduly damaging the experience for non-paying users. They’ve announced a few so-so sounding things, like quizzes and prompts designed to add texture to profiles and more curated profiles for women, but I’m not sure why these rollouts should work when so many others like it have failed.

I’ve viewed Match’s prospects through a pessimistic lens thus far. But the company has several things going for it too.

First, while historically even once leading online dating sites abruptly lost significant share in a matter of years, that share loss occurred in the context of a rapidly expanding market. Share loss does not necessarily imply an imploding user base (consider that between 2014 and 2019, Tinder lost several points of market share even as its MAUs grew 44%2[13]). Match Group consolidates its atrophying legacy brands (namely, Match, Meetic, OkCupid, and Plenty of Fish) and its nascent ones (namely, BLK, Chispa, and The League) in a single segment (”Emerging & Evergreen”) that is declining low-single digits. Its non-Tinder revenue in 2016 – which basically reflects all the old stuff, including a full year of Plenty of Fish – was about $950mn. Based on management’s limited disclosures, it looks like those brands did around ~$650mn in 2022 and maybe ~$590mn this year, implying ~6%-7% annual contraction over the last 7 years. So while Match’s musty brands have declined, they’ve done so at a more measured pace than one might think, especially considering that, as desktop native apps, they were on the wrong side of a generational platform shift. I don’t want to minimize the structural challenges. Those legacy properties saw revenue declines accelerate to 11% over the last 2 years. I only mean to point out that just because a dating app fades out of conversation does not mean it step-functions to zero.

It’s also worth setting aside historical comparisons to just consider whether it would even make sense to launch a new mainstream dating app today. How would you do it? Tinder found product-market fit with swipes in 2012. Hinge was founded at about the same time, Bumble just a few years later, both counter-positioning against Tinder with serious relationship intent. There are and will continue to be countless niche dating apps but I feel like Tinder, Hinge, and Bumble pretty much have the mainstream segment covered. I’m not sure what new product innovation you’d launch from scratch today on mobile that hasn’t already been tried to draw the marginal user away from the liquid networks spun up by those established brands. That all three are all successfully pushing price testifies to the absence of viable alternatives.

Second, while bears will interpret Tinder’s emphasis on RPP gains at the expense of payer growth as evidence that Tinder has saturated its market and is now resorting to value extraction, a more charitable interpretation – the one management obviously encourages analysts to take – is that Tinder’s past payer count was inflated by sub-optimal monetization. With aggressive pricing having now shaken out the weak hands, Tinder is building off a somewhat lower, reset base and can deliver a more even contribution from payers and RPP going forward. There is some early evidence of this, with payer losses attributable to US price hikes dissipating in 3q23, even with RPP growing by 8% q/q.

In 2q23 management launched weekly subscriptions in the US, which had the predictable impact of immediately juicing payer numbers, some of whom then churned off. But those declines should also settle over the next few quarters. We’ll see!

Third, to some extent Tinder’s durability is born out by the instability of its management. Tinder is now on its 6th CEO since 2015, Match Group is on its 4th. Various product managers and marketing officers have come and gone along the way. Former employees consistently complain about abrupt shifts in product strategy brought about by crazy turnover in the executive ranks. And yet, amidst that chaos, Tinder has 11x’ed revenue and 6x’ed payers.

On the back of Tinder’s vertiginous rise and with Hinge following in Tinder’s wake, Match Group’s EBITDA and free cash flow (including stock-based compensation and excluding a significant litigation settlement in 2022) have grown by 22% and 20% per year, respectively.

So on the one hand, you could characterize Match as a directionless company plagued by years of inconsistent product direction and mismanagement. On the other hand, what better demonstration of product-market fit than Tinder sextupling payers despite said mismanagement, to say nothing of the stunning traction at Hinge? Match and Tinder’s current CEO, Bernard Kim, has been in place for almost 18 months. It has yet to be seen whether this ex-gaming executive proves a good fit for a dating app. But so far he’s made what I think are sensible moves in retiring Tinder Coins, swearing off big-ticket M&A, dropping the metaverse blatherskite pushed by his predecessor, and pursuing less radical blocking and tackling maneuvers around monetization and product experience.

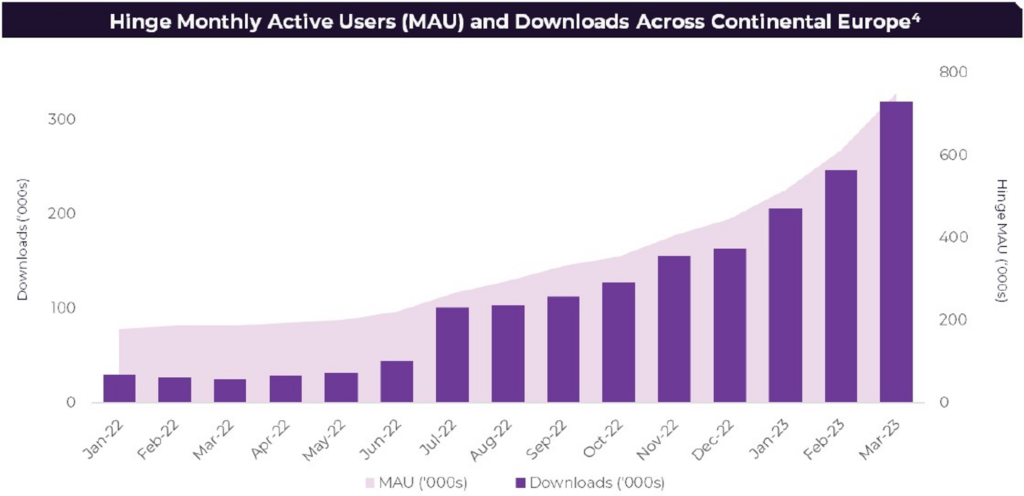

Fourth, Hinge is one of the fastest growing mainstream dating apps on the market and Match owns it. They paid somewhere around $25mn in 2018 for an asset whose revenue is today run-rating at $400mn, having grown by 43% from a year ago.

In the 5 years since Match acquired a majority stake, Hinge has gone from the 13th most downloaded app in the US to the 3rd[14]3[15]. It has exploded in popularity across continental Europe – its download rank improving from #21 to #3 from May ‘22 to Mar ‘23 in Germany and surging to #2 in France, behind Tinder, just 3 months after launch – and is among the top 3 most downloaded dating apps in 14 countries.

Hinge caters to those with serious relationship intent and demands more time of users upfront, so I doubt its user base will ever catch up to Tinder’s. But by virtue of drawing serious daters, Hinge should have more pricing power. I estimate Tinder’s US RPP to be ~$26, implying that Hinge, which does $27 from a user base heavily concentrated in rich Western countries, probably has a lot more room to grow (by comparison, The League, another dating app owned by Match Group, which admits members based on social status, educational attainment, and professional accomplishments, does more than $100).

Hinge’s unexpected success segues to another key point. While Tinder is by far its most significant banner, it is buttressed by a long tail of apps in Match’s portfolio, each catering to a different user base – snobs (The League), African Americans (BLK), Latinos (Chispa), Christians (Upward), single parents (Stir), serious daters (Hinge), gay men (Archer). Within the mainstream apps, there is even a plausible “lifecycle” narrative where users engage most on Tinder in their early-20s, then age into more “serious” apps like Hinge and Bumble in the late-20s and early-30s. Alongside those are apps targeting Asian markets (Pairs, Hakuna, Azar) and old school properties like match[3].com, Plenty Of Fish, and OkCupid that are being gracefully harvested for cash. Most of these properties will amount to nothing, but it’s hard to say which ones. Success in online dating business is hard to predict. Match spent $575mn on Plenty of Fish, which ultimately went nowhere, and $25mn for Hinge, which has become a top 3 dating app by revenue.

But thinking of Match Group as a portfolio of call options with random, binary outcomes is probably too simplistic. Despite chaos in the executive ranks, the company seems to have a knack for profitably growing brands. Match.com[3] was for years the leading dating site in desktop. Tinder was incubated at IAC and grew to become the dominant dating app globally under Match’s ownership. Hinge did just $5mn in revenue the year it was acquired by Match and now, less than 5 years later, is run-rating at $400mn. Archer was built in-house and is close to rivaling Grinder’s US weekly downloads just months after its limited rollout.

A skeptic might retort that we don’t know the counterfactual, that Match is just riding the wave of colossal success that these banners would have experienced as standalone companies anyways. Fair! While there are some lesson and tactics shared across them, Match’s properties generally operate independent of one another (their flagship apps have different code bases and even different headquarters), which stokes the perennial concern that another app could launch out of left field today and steal Tinder’s users. But again, the highest-revenue generating dating apps in the US today (as far as I know) – Tinder, Hinge, Bumble, Grinder – were all founded more than 10 years ago, in the early days of smartphones. As long as mobile remains the dominant platform, it’s hard to see a startup introducing a novel angle of attack that siphons users away (AI girlfriends maybe?).

Given that dynamic, the natural exit strategy for a pre-revenue dating app that is starting to gain traction in some niche is to sell to Match. Even if you are of the opinion that Match isn’t operationally responsible for the success of its apps, they’ve at least put resources behind the right ones. Consider that, what, hundreds of US dating apps have launched since the mid-‘90s? Is it just coincidence, having nothing to do with resource allocation or execution, that 2 of the 4 highest monetizing ones in the US happen to be part of the ~45 that Match owns? Maybe, but I doubt it.

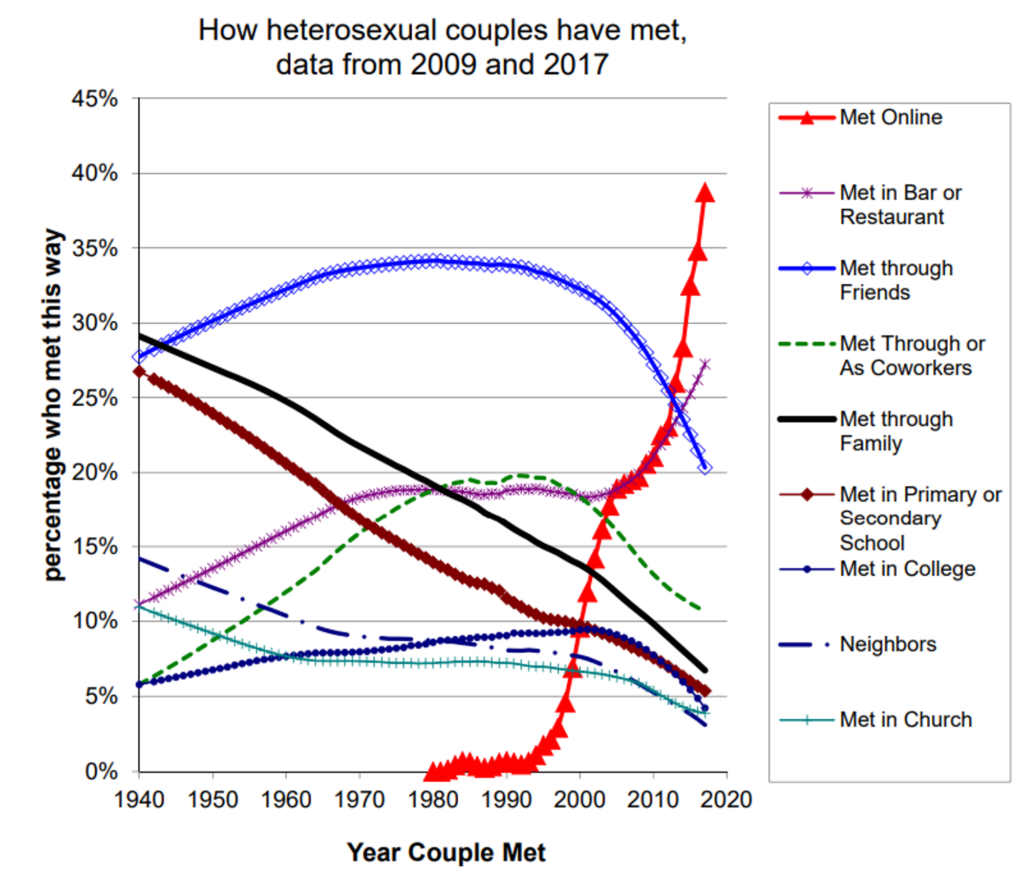

Match Group is for now a bet on Tinder. But as a vehicle of diverse apps catering to a broad swath of niches, managed by a group with a strong track record of acquiring and profitably nurturing the industry leaders, it is also a bet on the online dating category as a whole. I think you can feel good about the latter. In the Western world, the cultural taboos around online dating have more or less fallen away. By 2017, more heterosexual couples in the US met online than through any other channel, with a new S-curve for online dating forming at around the time smartphones took off.

Source: Disintermediating your friends[16]: How Online Dating in the United States displaces other ways of meeting (Michael Rosenfeld, Stanford University, 2019)

In the Middle East and Asia, online dating is far more stigmatized (in Japan, for instance, Tinder users will commonly post pictures of flowers and landscapes instead of their faces) and monetizes at lower rates to boot. But even if adoption is never as widespread there as in the US, I suspect it will continue to trend the same way.

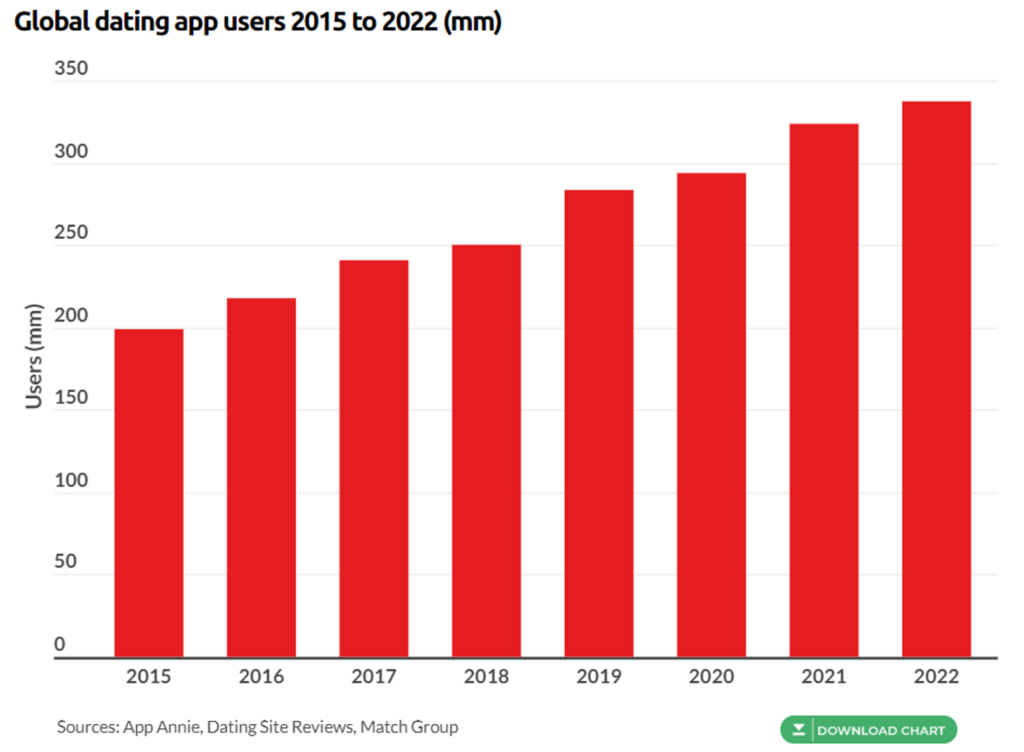

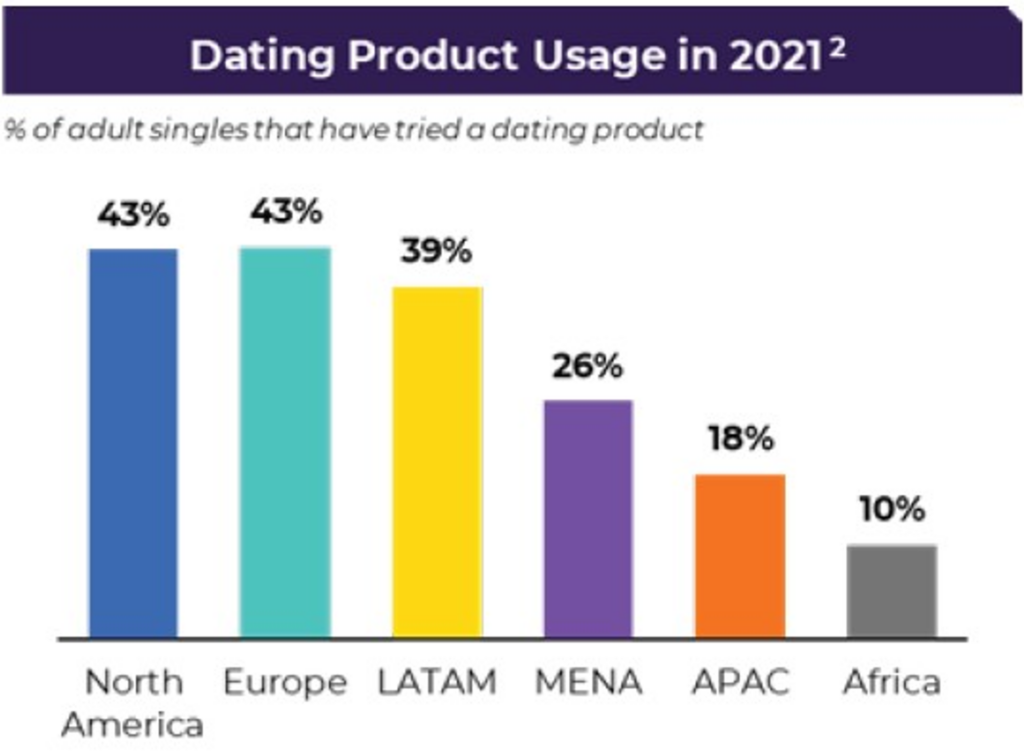

The number of dating app users globally grew by ~8% a year from 2015 to 2022 and I see no reason why growth should meaningfully slow.

Even in “mature” markets like North America and Europe, 57% of adult singles have yet to try a dating product.

Source: Match Group (1q22 shareholder letter)

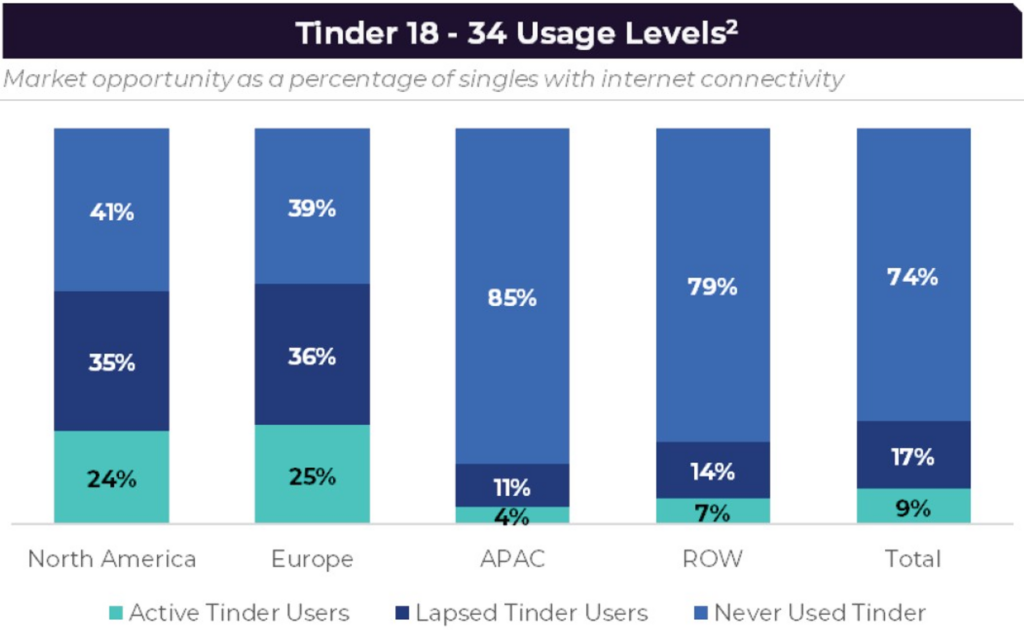

In theory, Tinder also has room to grow, with only 24% of single 18-34 year-olds counting themselves active users. Another 35% are lapsed users and another 41% have never used Tinder at all.

Source: Match Group (8/2/22 investor letter). 2021 surveys and research. Percent of respondents that have ever used a dating app or site (single, and not in a relationship), excluding China.

All dating platforms must contend with success translating into users pairing off and leaving the platform. But this headwind is offset by new, larger cohorts of 18-year old’s who are going to be pulled to the most liquid network like the cohort before them, and lapsed users who reactivate their accounts when those relationships don’t work out.

In summary, Match Group is a vivarium of dating sites targeting a broad swath of interests and demographics. Its marquee brand, Tinder, is showing signs of user stagnation, but revenue growth has accelerated from 4% to 10% over the last 2 quarters on the back of significant price hikes and the introduction of weekly subscriptions, a rate of growth that it expects to maintain next year. Payer declines are moderating as users adjust to the changes, with management expecting a return to sequential growth by the middle of next year. Whether they can pull this off, let alone return to mid/high-single digit growth will depend on top-of-funnel growth, which they are trying to improve with product and marketing initiatives. I think they’re in a tough spot here for reasons I discussed. Hinge, meanwhile, is on fire. Last quarter they grew payers by 33% even as RPP advanced 8%. With just half the number of payers as Bumble and RPP at US Tinder levels, I suspect there is lots of runway for both metrics.

The msd revenue declines at Evergreen and Emerging (22% of revenue) should moderate somewhat as the segment continues to mix toward the fast growing Emerging concepts, which growing 40%-50% a year, partially offsetting the declines of legacy banners. Match Group Asia (9% of revenue) has reversed its y/y contraction and is now growing low-single digits as Azar, 2/3 of Hyperconnect’s revenue, is now growing 20%/year on the back of “AI-enabled” algorithmic matching (whatever that means), offsetting the continued weakness at Pairs (the largest dating app in Japan) and Hakuna. Meanwhile, operating margins have expanded from flat at the time of acquisition to around 10%. While Hyperconnect did not live up to Match’s metaverse ambitions and management would probably take back the acquisition if they could, it brought some advanced technology that can be leveraged across Match’s other brands and it doesn’t hurt to own a platform that is tuned to the cultural sensitivities of what could prove the largest addressable region for online dating.

Finally, last year Match paid $623mn to app stores, a huge sum compared to its $965mn of EBITDA. I wouldn’t buy shares on the expectation of massive fee relief, but maybe keep this option in your back pocket for a rainy day.

All things considered, I can appreciate how many think the stock looks attractive here at 18x trailing free cash flow, 14x EBITDA. To put things in perspective, Match has around the same market cap and only 25% more enterprise value than it did at the end of 2017, when Tinder was doing just 1/5 the revenue and Hinge wasn’t even part of its complex. At 40x free cash flow it was arguably overvalued back then but at less than half that multiple today I think you can make a reasonable case that the stock has overshot to the downside. Assuming 8% growth at Tinder (0% payer growth / 8% RPP growth), 27% at Hinge (18% / 7%) growth, 3% at Match Group Asia, 15% contraction at established brands, and 25% growth from emerging ones, blends out to ~9% revenue growth over the next 5 years. With so much of that growth fueled by pricing at Tinder, we could see a doubling of EBITDA that drops down to ~$4.5 in per share cash earnings (including stock comp). At 15x-20x + accumulated cash, the stock compounds between ~19% and 25%.

At the same time, that’s all just playing with numbers. I can’t say I’ve got strong opinions one way or another about the extent of Match’s pricing power, its ability to drive user growth, the efficacy of its marketing initiatives or pending product refreshes or really anything! Hinge is often pitched as a “hidden” asset that will become more appreciated as it makes up a larger part of Match, but I’m not sure how much long-term signal we can confidently glean from current results. Fade rates can be much steeper than investors appreciate. Tinder was growing by more than 40% just 4 short years ago, about as fast as Hinge is growing today. But then again, singles need to go somewhere to find dates and where else if not Tinder, Hinge, or any one of the dozens of apps in Match’s complex?

Disclosure: none of the accounts I manage own shares of Match Group

IAC and MGM

Posted By

scuttleblurb

On

In

SAMPLE POSTS,[IAC] IAC,[MGM] MGM |

3 Comments

There was a time, not too long ago, when an investor could treat IAC as a collection of binary early stage bets anchored by a few more mature and profitable entities. To most, IAC’s 12% passive minority stake in MGM, acquired near the COVID lows, was a weird one-off opportunistic gambit that could be marked to market. The real diligence was saved for Angi’s, DotDash, and Vimeo. I don’t think many felt compelled to deep dive into casinos because like, whatever, the $1bn MGM investment comprised just ~9% of IAC’s market cap at the time and it felt like most of the upside was going to come from IAC’s digital assets, not a passive minority stake in a mature brick-and-mortar casino operator. Psych!! Now Angi’s is melting away as its fixed price offering, launched to great fanfare 2-3 years ago, struggles to find product-market fit. DotDash no longer expects to hit its $450mn EBITDA target next year given the weakness in brand advertising. Vimeo has lost ~90% of its market cap since being spun off last May, as losses have widened, growth has dramatically decelerated off tough COVID comps, and investors have soured on unprofitable growth concepts. Meanwhile, MGM shares have nearly doubled from the ~$17 price at which IAC first accumulated shares in 2q and 3q 2020. IAC has since added to its MGM stake, first at $45 and more recently in the low-$30s. With valuations in digital growth assets wrecked and its own stock price sliced in half, IAC could have opportunistically acquired another digital lottery ticket or more aggressively repurchased (more of) their own shares. But no. They increased exposure to MGM instead. Today, the $2.1bn MGM position accounts for 35% of IAC’s market cap, making it the second most valuable asset in the IAC complex after DotDash.

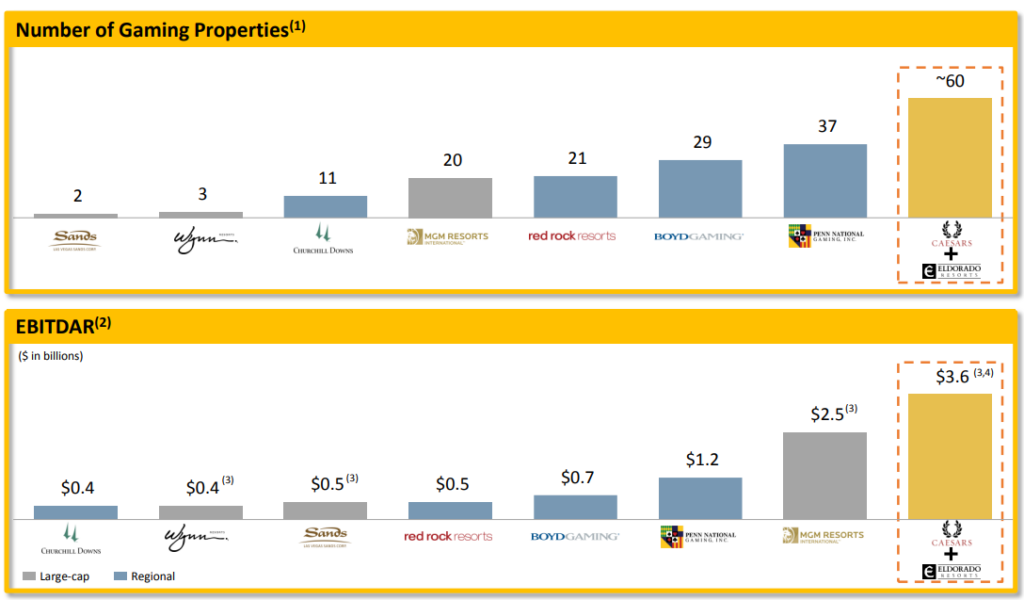

MGM is a set of cash flowing retail casino properties plus a call option on a nascent but potentially massive online sports betting and iGaming opportunity through its 50% ownership of BetMGM. Through its Las Vegas Strip (LVS) segment, MGM operates 9 casino resorts, with Aria4[17], Bellagio, MGM Grand, Mandalay Bay, and The Cosmopolitan the most notable and profitable among them. The Regional segment consists of 8 casinos, with The Borgata (Atlantic City, NJ), MGM Grand Detroit (Detroit, MI), and MGM National Harbor (Prince George’s County, MD) contributing more than 60% of Regional’s pre-COVID segment EBITDA.

Las Vegas has come a long way from the mob-run cesspool portrayed in the 1995 classic Casino. In his concluding monologue, Sam Rothstein, head of the (fictitious) Tangiers casino, laments:

The town will never be the same. After the Tangiers, the big corporations took it all over. Today it looks like Disneyland….After the Teamsters got knocked out of the box, the corporations tore down practically every one of the old casinos. And where did the money come from to rebuild the pyramids? Junk bonds.

Today’s Las Vegas is an entertainment destination, host to an NFL team, dozens of industry trade shows, megastar concerts, and Michelin Star Restaurants. Profits have migrated away from low and mid-tier casinos like Circus Circus and Westward Ho, toward properties that resemble luxury cities, with high end retail spaces, restaurants, and other posh amenities enveloping conference attendees, high rollers, and Asian tourists, a favorable development for MGM and Wynn, whose Vegas portfolios tilt fancy.

Regional properties are more for the dead-eyed locals. Atlantic City and certain high-end 100k+ square foot casinos like MGM’s Borgata and National Harbor have a regional “destination” feel to them I suppose, but there are hundreds of others – like the Ameristar and Hollywood branded locations run by Penn Entertainment or the Isle of Capri and Harrah’s casinos run by El Dorado (now Caesar’s) – that attract middle-income gambling-oriented clientele in a ~100 mile radius.

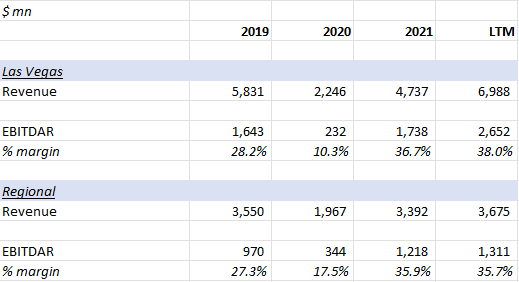

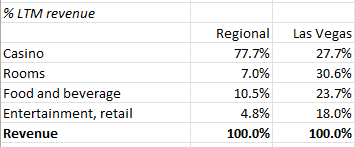

So while MGM’s LV segment gets nearly 3/4 of revenue from non-gaming sources – hotel rooms, food, beverage, entertainment, and retail – close to 80% of Regional revenue comes from gaming.

You’ll notice a similar disparity at Wynn and, to a lesser degree, at Caesar’s, which latter operates shabbier Vegas properties like Flamingo (will probably be sold soon), Bally’s, and Paris that don’t attract as much food and retail traffic.

The gaming industry has consolidated over time, with acquirers binding disparate casino properties together through loyalty programs, keep players engaged in an ecosystem. Through the MGM Rewards – the second largest gaming rewards program after Caesar’s, with ~35mn members – regional casinos can feed traffic to destination resorts, as the rewards earned by gambling at Beau Rivage can be redeemed for concerts or room discounts at the Bellagio or Aria.

Here’s a pre-COVID summary of the top casino operators in the US:

Source: Caesar’s/El Dorado merger presentation

MGM is in the middle of the pack in terms of property count, but generates the most EBITDAR per property with 3 of the 5 most profitable Vegas assets, and commands leading ~50% share of the Vegas gaming market, which is in a much better state today than it was heading into the last recession. Back then, Vegas was flooded with supply, with MGM, in partnership with Dubai World, breaking ground on City Center, an 18mn square foot hotel-casino-retail-residential colossus5[18] whose development costs exploded from $4bn to $9bn just as the economy tipped into recession. Exacerbating matters, another luxury casino resort, The Cosmopolitan, opened its doors just a year later in 2010. Since then, with the exception of Resorts World last year, there haven’t been any notable capacity additions and by most accounts there won’t be for at least the next 5 to 10 years. The returns just aren’t as compelling as they used to be. The Bellagio, the most profitable casino in Vegas, generated ~$500mn of EBITDAR at its pre-COVID peak on a development base of just over $2bn. If Resorts World is any guide, a comparable property would cost more than twice as much to develop today.

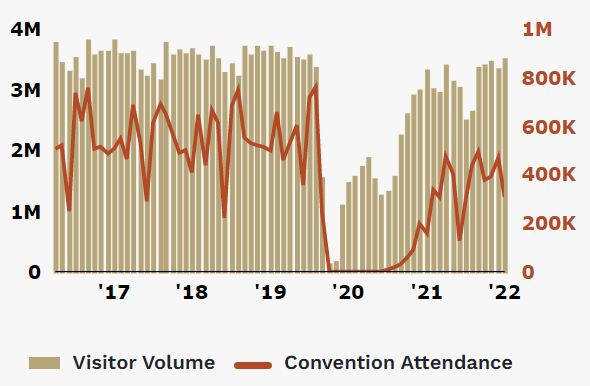

Following a brief COVID blip in 2020, Vegas is booming again. MGM’s LVS EBITDAR margins, at 38%, are 7-8 points above their pre-COVID peak on record revenue, even with cross-border travel restrictions deterring high-spending Asian gamblers and traffic from convention attendees, who are among the most profitable customers, ~1/3 below pre-COVID levels.

Source: Las Vegas Convention and Visitors Authority (link[19])

MGM isn’t alone. Caesar’s and Wynn have also reported record Vegas profits. Some of the margin gains are due to sustainable cost cutting and efficiency gains – things like self-service check-ins and the cessation of daytime entertainment and buffets and whatnot. But I think most of it can probably be attributed to temporary COVID spasms. Operators haven’t had to invest as much in promotions and marketing to lure pent-up demand and Average Daily Room rates are 36% above 2019 levels.

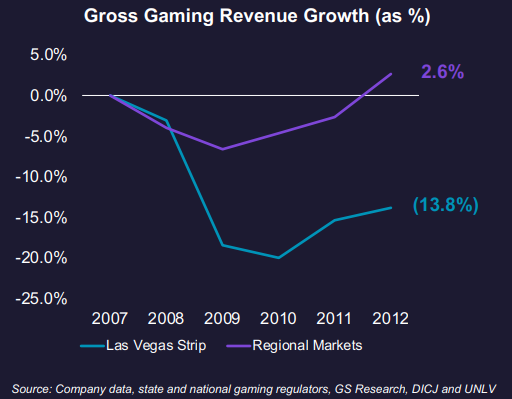

The Regional properties are also enjoying record margins but facing tough comps as locals apparently dumped their stimulus checks on slots and blackjack last year. But if the last recession was any guide, gaming revenue at regional properties tend to be relatively resilient.

Source: PENN Entertainment presentation (8/2/22)

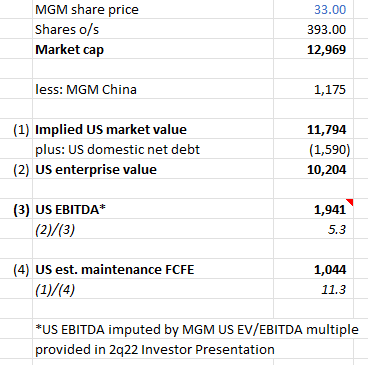

In addition to its US properties, MGM also owns a 56% stake in MGM China, which operates two casinos in Macau that derives ~80% of revenue from gaming. The Macau gaming market, once the world’s largest, has been decimated by draconian COVID restrictions that include occupancy limitations, temperature checks, quarantines for mainland Chinese residents. The Chinese and Hong Kong governments suspended group tour travel and ferry service. The consequences have been predictable. MGM China did -$66mn of EBITDAR over the last 12 months, down from $735mn in 2019. The Hong Kong listed stock has lost ~80% of its value since the start of 2018. With Macau and China lifting some restrictions in recent months, I’m inclined to think the worst has past. But even if I’m wrong MGM still looks pretty dang cheap:

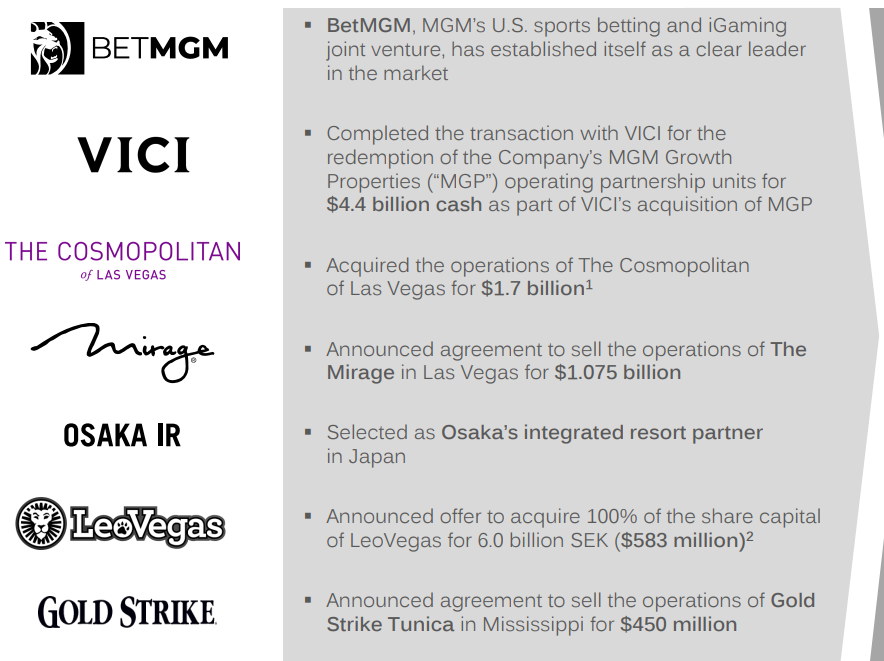

And I guess MGM’s management thinks so too as they’ve raised capital through a series of transactions (see below), including the sale of the operations of The Mirage and Gold Strike for 17x and 11x EBITDA, respectively, to retire 31% of its shares since early 2021 at ~5.5x EBITDA.

(the most significant source of cash has come from the sale of MGM’s operating partnership units of MGM Growth Properties (MGP) – an umbrella partnership REIT[20] that owned 7 of MGM’s LVS properties – to VICI Properties, another REIT formed in 2017 as part of Caesar’s bankruptcy restructuring, who is leasing back the properties to MGM. The real estate of MGM’s other 2 properties, Aria and Bellagio, is owned by Blackstone. Today, all of MGM’s domestic properties are owned by either VICI or Blackstone-affiliated entities. Sale-leasebacks have become a common way for casino operators to raise cash. El Dorado funded part of its $17bn merger with Caesar’s by selling casino real estate to VICI).

MGM’s profit margins are probably somewhat inflated and who knows if convention traffic ever reverts to pre-COVID levels. Compressing MGM’s property margins by 5 points and assuming no MGM China appreciation results in a valuation of 7.6x US EBITDA / 20x mFCF, which still seems reasonable for a collection of high-end casino resorts, bound together by a huge loyalty program, that gush cash as part of a consolidated industry structure. Admittedly, the US retail gaming industry is saturated, with few avenues for organic growth. But MGM has a few aces up its sleeve ;).

First, 15 years after it first actively explored development in Japan, MGM, together with its local JV partner ORIX, was finally selected by Osaka to build one of the country’s first integrated resorts. Several other US operators have tried to crack the Japanese market over the last 20 years, to no avail. Las Vegas Sands withdrew its bid in Osaka[21] to pursue development in Tokyo or Yokohama before pulling out of those cities as well in May 2020. Wynn also dropped out of Osaka in 2019 after a decade of “working on Japan quietly behind the scenes”6[22]. They claimed to be pursuing something in the Tokyo region, but haven’t followed up on this for years. Caesars withdrew from Japan following its merger with Eldorado, with Eldorado CEO Thomas Reeg cautioning analysts that they had “not made firm decisions on the international front”. But then soon after MGM won over Osaka, the company announced it was back in the game[23], working with Clairvest, former Las Vegas Sands executives, and a consortium of developers to build something in Wakayama.

Should the MGM-ORIX bid be approved by Japan’s central government sometime in the next few months, the consortium expects to break ground in late 2023 and open in 2029. This is a big deal. At an expected cost of $10bn, Osaka will quite possibly be the most expensive casino ever built. The project will likely be funded 50/50 between MGM and ORIX (or 40/40/20, with the 20% stub funded claimed by a yet-to-be-determined group of Japanese companies). Assuming its 50% share is 55% debt-funded, MGM will contribute around $2.25bn. I think the most expensive casino resort built so far in Asia is Wynn’s Marina Bay Sands (Singapore), which opened in 2010 at a cost of $5.8bn and did $1.7bn peak EBITDA on a $3bn revenue base. At 30% of gross gaming revenue (or “GGR”, amounts wagered minus amounts won by gamblers), Japan’s gaming tax rate is considerably higher than Singapore’s, which ranges between 8% and 22%[24]. So maybe on a $10bn investment, the Osaka mega-resort delivers something like ~$6bn of revenue and ~$2bn of EBITDA. At 8x EBITDA, MGM’s 50% stake is worth $8bn, the equity portion ~$5bn, translating into ~$1.2bn of incremental equity value when discounted back 8 years at 12% (compared to MGM’s present ex. MGM China market cap of $12bn).

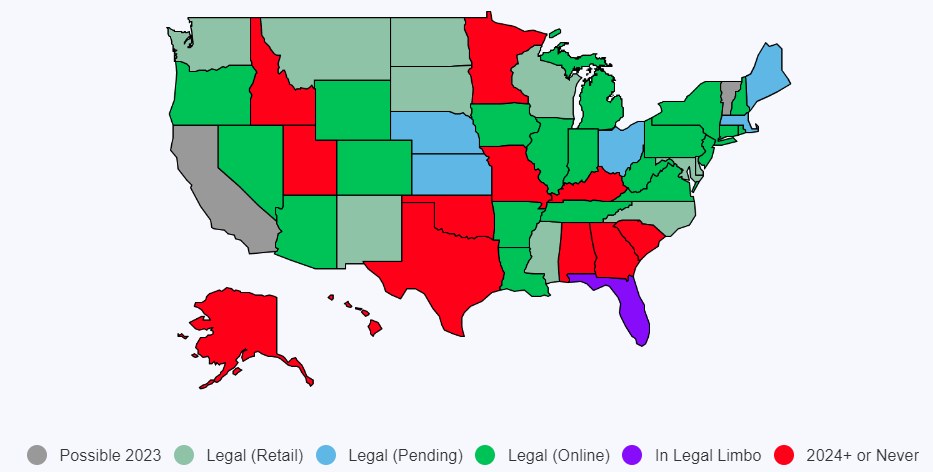

Possibly more significant is the latent value in MGM’s 50% ownership of BetMGM, an iGaming (online casino) and online sports betting joint venture with UK-based online gaming operator Entain7[25]. Since the Professional and Amateur Sports Protection Act (PASPA) of 1992, which prohibited online gaming activity in most states, was overturned by the Supreme Court in May 2018, online sports betting has been legalized in 25 states. To the degree that Daily Fantasy Sports, which is regulated in 43 states, is a leading indicator for OSB we may see more states follow suit.

Online sports betting is now accessible to ~44% of the US population. Should Proposition 27 pass in California this November – which seems probable given that 58% of Californians supported the ballot measure, as reported by BetMGM management in May – penetration will ratchet to ~56%. This should be particularly good for BetMGM as Vegas traffic and MGM Reward’s membership over-indexes to California.

Without the cultural entrenchment of sports, iGaming acceptance has been harder to come by, legalized in just 7 states8[27].

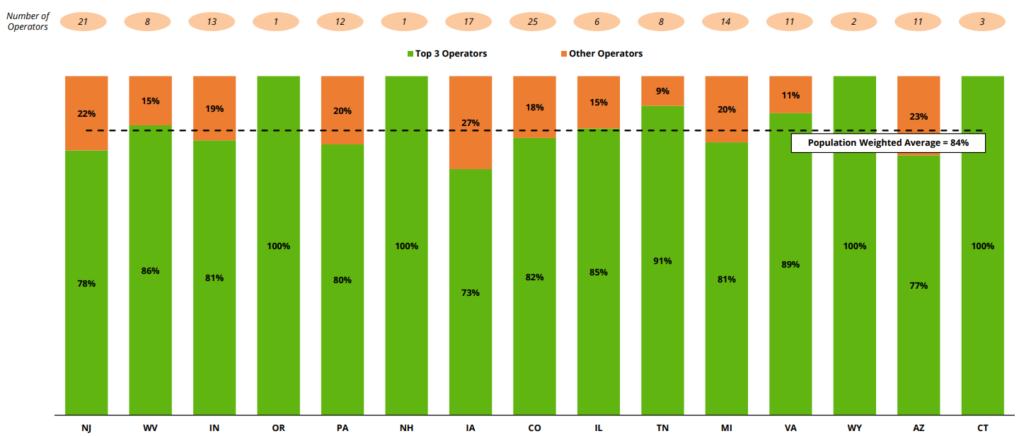

Wynn tried to offload its OSB/iGaming division last year to a SPAC run by Bill Foley (of Fidelity National fame), but the deal was called off months later. At the moment, Wynn Interactive is run-rating at just $80mn in revenue (compared to $1.6bn of LTM revenue at DraftKings and $1.3bn of expected 2022 revenue at BetMGM) and isn’t losing nearly enough money to make me believe management is taking things all that seriously. Caesars claims around low-teens share of national sports betting measured by handle (the $ amount of wagers placed) but MGM has some exhibits that suggest Caesars’ share is much lower by GGR. PENN Entertainment, with $547mn of LTM digital revenue and its insistence on responsible growth, hasn’t engaged in promotional land grabs to nearly the same degree as peers, generating -$17mn of cumulative EBITDA on $889mn of revenue since the start of 2019 compared to -$2.9bn of EBITDA on $3.1bn of revenue at DraftKings. There are a dozen others getting after it but by most accounts FanDuel, DraftKings, and BetMGM are so far the primary contenders, with ~75%-80% combined GGR share in OSB and 70%+ share across OSB and iGaming.

Here is Online Sports Betting GGR share by state:

Source: DraftKings Investor Day (March 2022)

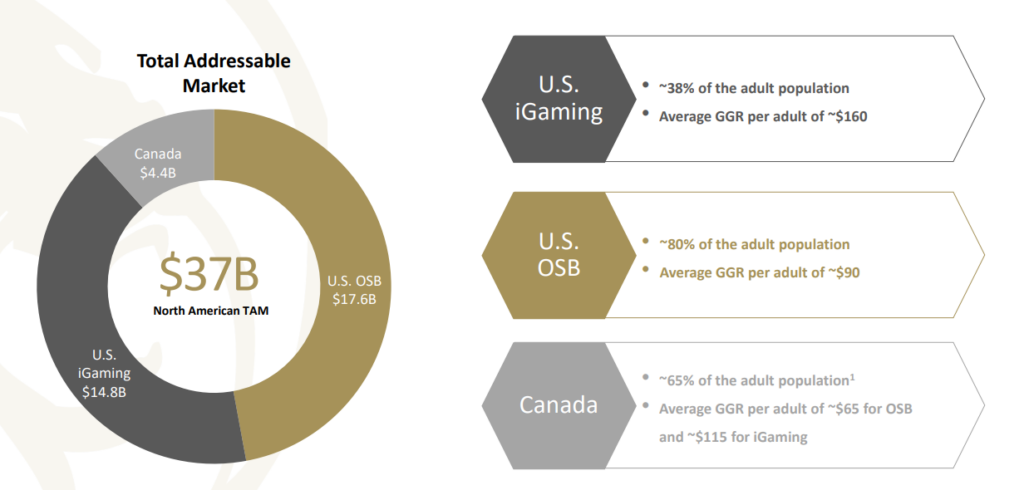

Just 4 years since PASPA was overturned, the $32bn addressable US market is fueling vertiginous growth for the leading participants. BetMGM is on pace to deliver $1.3bn of revenue this year, up from less than $200mn in 2020. FanDuel and Draftkings have likewise produced explosive triple digit annual growth.

Source: BetMGM

(DraftKings estimates $26bn of US TAM by applying the OSB and iGaming gross revenue per adult in New Jersey, the most mature online gaming market, to the US adult population and adjusting for differences in per capita GDP).

The growth is not without controversy. The primary bear case is that in their rush to grab share, online operators are spending exorbitant sums on marketing and promotions that can’t be justified by the lifetime value of acquired gamblers. This past January, my friend Andrew Walker called attention to the frenzy of promotions in the newly authorized New York market, observing in his article What the fudge is happening with NY sports betting promos[28]?

But I don’t understand how businesses can create positive value from the amount of free money that’s being given away. Consider Caesar’s, since they’re the outlier in terms of over quality. They’re givign away free bets; if you assume those bets are ~50/50, they’re effectively giving away $1.65k for a $3k deposit. Now, it’s not quite that bad, since you do need to do some betting to unlock all of that money, so Caesar’s will pick a little bit back in spread fees and everything…. but I just having trouble believing that the average customer Caesar’s is grabbing has a life time value of more than $1.65k.

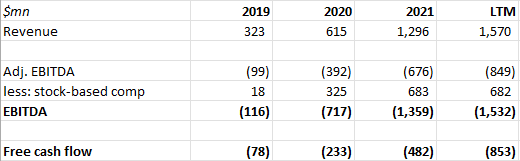

With sales and marketing expenses more than double its gross profits, DraftKings has been burning cash hand over fist:

(check out the stock-based compensation running at 44% of revenue!)

These financials are a horror show.

DraftKings will retort that 83% of acquired customers retain after 1 year, 70% after 3; that a given cohort, including churned customers, generates 122% of year 1 revenue in the second year, 143% in the third. That doesn’t resolve the lifetime value question since those retention and gross revenue figures may be sustained by ongoing promotions. Also, that BetMGM sees most of its acquired customers churn off in the first 4 months before leveling off – a progression that seems more realistic to me – makes me skeptical of Draftkings’ claims (or at least its presentation of those claims).

BetMGM sometimes trots out this exhibit to demonstrate their strong competitive position across OSB and iGaming:

But what’s more interesting to me is how wildly market share shifts from month to month based on the relative promotional cadence of each participant. To be fair, a bunch of states have legalized gaming over the past year on a low starting base, so a player who gets the jump in a handful of new jurisdictions by bombing new gamblers with promotional offers can quickly find themselves taking meaningful national GGR share even if their competitors do a good job retaining existing customers. Even at a state level, a similar low base effect may be at play. In New York, Caesar’s Digital debuted this year with absurdly generous promotions (see Andrew’s post) to win 41% of GGR, only to see its share fall to 15%-20% as soon as it cut back on marketing. But given how nascent the New York OSB market is, Caesar’s may still find itself losing share even as it retains GGR from existing customers if most of the incremental GGR is picked off by competitors who continue carpet bombing the market with promos. Like let’s say in the first few months of launch, state GGR grows to $10 against an addressable potential GGR of $100, with Caesar’s claiming $4. Caesars can retain all $4 of GGR after it pulls back on marketing and still see its market share reduced to 20% if DraftKings and FanDuel promo their way to winning 80% of the next $13 of state GGR. In short, share volatility may be less indicative of an unhealthy market than an early one.

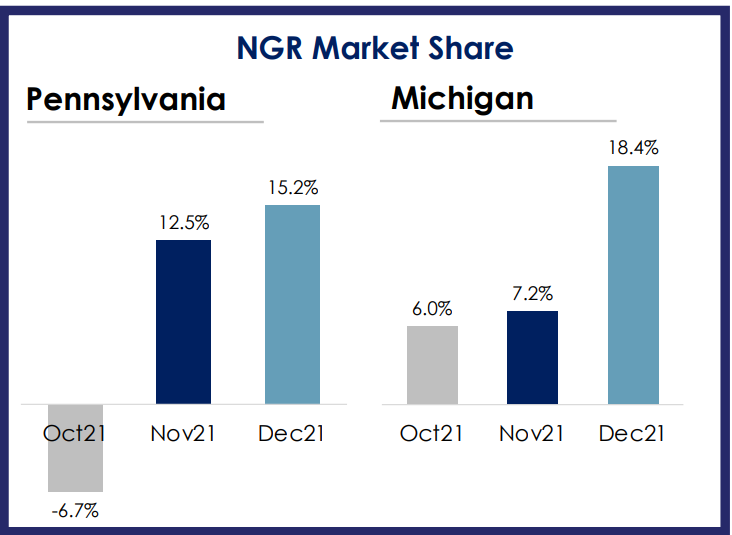

It’s worth noting that if customer retention sucks, GGR may be a misleading measure of sustainable share because it doesn’t subtract promotions, which latter can be so high that they comprise the bulk of GGR – for instance, in 1q22, Caesars Digital reported negative $53mn of net revenue (as Caesar’s admitted, ”we were more aggressive than we needed to be out of the box”). PENN Entertainment, who has excoriated its spendthrift peers, likes to point out that it has grown share on a Net Gaming Revenue (NGR) basis with a far more abstemious marketing diet.

Source: PENN Entertainment

But this is misleading in the opposite way because PENN’s NGR share will naturally grow in the short-term if everyone else is busy depleting their own NGRs with big upfront promos. And if acquired customers really do retain (and gamble) at high rates without much incremental marketing, then PENN will lose NGR share as state markets saturate and DraftKings, etc. taper off their splashy promos. Notably, since it dramatically curtailed CAC, pulling hundreds of millions that it planned to spend on marketing, Caesars claims that its national handle share has remained steady at around 15%, so maybe it’s had some success leveraging its loyalty program and physical properties to build loyalty with online gamblers.

To me, the most compelling sign that all this promotional spending may earn a return after all is that DraftKings is consistently seeing positive contribution profits (gross profits minus advertising expenses) in states 2 to 3 years after entry, suggesting that promotional costs do indeed taper off as as the number of remaining customers left to acquire shrinks…which of course would only be possible if existing customers didn’t need to be re-engaged at the same cost over and over again. In 2018, its first year in New Jersey, DraftKings reported $10mn of contribution losses on $21mn in revenue; in 2021, they generated $68mn of contribution profits on $239mn of revenue (28% margins). Between 2018 and 2019, DraftKing launched in 5 states. 4 of them were profitable by 2021 and the 5th is expected to be by the end of this year. The 2-3 year ramp to profitability has been observed by BetMGM and Caesar’s as well, with the former realizing contribution profits in just 6 months in Michigan.

So the idea is that digital operators have reported horrendous consolidated losses over the past year because the upfront losses from seeding new, legalized markets are overwhelming the contribution profits from the few, early launch markets of 2018 and 2019. With online gaming now available to most of the addressable US population, the profitability picture is poised to flip around this year and next as the contribution profits from current legalized states more than offsets promotional launch costs in the relatively few remaining states who haven’t yet authorized online gaming but will. BetMGM expects to be EBITDA profitable by the end this year; DraftKings and Fanduel towards the end of 2023 (though with SBC such a huge cost add-back for DraftKings, does it really count?). The precise path of margin improvement is confounded by the timing of new state launches – for instance, marketing and promotional costs from a California launch will absorb profits that would otherwise have been realized from existing states. But at maturity, digital operators expect to generate margins that are comparable to retail casinos.

For this to materialize, Tier 1 operators need to somehow acquire and engage customers in a cost advantaged way. As is true of any consumer facing app, engagement means having a responsive app with compelling content. Some operators might start by renting third-party gaming platform from Kambi or GAN. But to enable differentiated experiences, like variations of in-play betting and personalized gaming, all the majors have or are on their way to fully integrating their tech, with DraftKings acquiring SBTech, PENN Entertainment acquiring theScore as they transition off Kambi, FanDuel leveraging the tech platform of their parent company, Flutter, and BetMGM doing the same with their 50% owner, Entain. Everyone licenses content from IGT, Scientific Games, and Evolution through revenue share agreements but they also seem intent on pushing exclusive first-party games. As of April 2021, 5 of BetMGM’s top 10 titles were created in-house by Entain and Entain content accounted for 25% of BetMGM’s YTD GGR. PENN’s Barstool Casino gets 20% of its handle from in-house games, which it expects to grow to 50%. BetMGM estimates that in-house technology alone provides a 7% to 12% margin advantage over those who rely on third-party platforms.

The Tier 1s can also acquire gamblers at lower cost by piggy backing on existing assets. DraftKings and Fanduel converted their dominant share in daily fantasy sports into dominant share in online sports betting. PENN Entertainment hopes to lure the 20 to 40 year old audiences of popular sports media properties, spending more than $2bn for Barstool Sports and theScore. MGM and Caesars, with rewards programs that boast 35mn and 65mn members, respectively, can cross-promote across online and offline properties. BetMGM players enrolled in MGM Rewards and redeem points from their online play for discounted room rates or concert tickets or whatever at MGM’s regional or Vegas casinos. MGM reports that BetMGM is the largest source of new MGM Rewards enrollees, with over 43% of Rewards sign-ups now coming from BetMGM compared to 33% a year ago. Once ensnared in the MGM ecosystem, sports betters can be cross-sold iGaming and vice-versa. Where iGaming and OSB are allowed, MGM reported in 1q that 44% of online bettors engaged in both. Omni-channel players are acquired at just 30% of MGM’s average CPA and are predicted to be nearly twice as valuable as single-channel players. Finally, in states where they run physical casinos, MGM and Ceasars aren’t burdened with fees9[32] that pure online operators like DraftKings and Fanduel must pay to land-based operators in order to gain market access. BetMGM believes this provides a 6 to 7 point margin advantage.

Of course, none of these advantages prevent a newcomer from nuking the market with sloppy promos and destroying everyone’s unit economics for a while, though whether they can do so profitably without the scale of current Tier 1s is another matter. There is no reason for a gambler to download apps from no-name Tier 2 operators with no offline complements and inferior content and gameplay experiences, except to take advantage of one-time promos that are unlikely to prove sustainable. ESPN, rumored to be breaking into OSB, has the brand and audience to leapfrog into Tier 1 contention, but they will be starting years behind incumbents who have the tech, mindshare and, at least for MGM and Caesars, an irreplicable physical presence and rewards program. Plus, Disney is already burning billions on their DTC efforts. Do they want to burn billions more scaling OSB at a time when shareholders are whinging about cash flows?