Posted By

scuttleblurb

On

In

SAMPLE POSTS,[TRUP] Trupanion |

Comments Disabled

Looking at TRUP is like staring at one of those ambiguous images that could be both a rabbit and a duck, both a saxophonist and a woman’s face: we know that this is an insurance company, but we’re compelled to analyze it as a data-driven subscription service.

Of course, all responsible insurers are data-driven and the recurring nature of premiums also make them subscription-like, but we don’t typically think of insurers as a subscription service in the same vein as a SaaS enterprise. We do for TRUP largely because its management team has diligently trained us to focus on SaaSy metrics. Some of this is just reframing vocabulary: “subscription fees” not “premiums”, “members” not “policyholders”, “Territory Partners” not “agents”.. Trupanion’s ignorance of the insurance industry lexicon – scarcely a mention of reserves, underwriting leverage, medical cost trends, book value – is so obtrusive as to almost certainly be by design (what fast-growing enterprise wants to be seen as a boring insurance company?).

But this is also the first insurer I’ve see that disaggregates retention by member cohort and discloses lifetime value to customer acquisition cost ratios. That’s not a knock on the company. The first principle to any recurring, subscription-like model, insurance company or not, is onboarding customers for far less money than those customers will generate in lifetime profits. With most of the stuff you buy – a haircut, an iPhone – there is little confusion about the value of the product to you. Insurance is a lot squishier because you don’t know at the time of purchase whether you’ll need it. For major categories of insurance – where the covered thing is monetarily significant and its cost readily determinable, as in the case of a car or house, or where it transcends monetary value, as in the case of your family’s health – we easily buy into the collective understanding that in any given year, the premiums from those on whom fortune smiles subsidize those on whom she frowns. We don’t feel like our rights are being trammeled when law mandates we buy such insurance or that we’re being bamboozled when our insurer earns an underwriting profit from this scheme. We’re risk averse and understand that peace of mind is worth paying for and that an insurer should be compensated for giving it to us. But dogs and cats?

While there’s no question that we treat our pets far more humanely than we used to and that pets have graduated from the status of mere property, they still don’t occupy the same sanctified hemisphere as humans and we’re far from consensus on the range of seriously unfortunate health outcomes that we should be willing to prepare for. If you ask your friends about pet medical insurance, as I did, you’ll likely find that only a few have it, maybe half think it a reasonable purchase and the rest may outright scoff. Rather than pay $50 for a Trupanion policy with a 10% deductible, why not just put $40 in the cookie car every month as a sort of pet health savings account? If I’m shelling out $600 this year for a Trupanion policy and eat 10% of the costs, I need to think there’s a 20% chance of at least $6,000 in medical emergencies in the next 12 months for the policy to be “worth it”. [to put that in context, treating hip dysplasia for a Golden Retriever can cost anywhere between $2,000 (if diagnosed early) and $5,000 (if diagnosed late and a hip replacement is required)].

Of course, the decision to purchase insurance can be an emotional one that goes beyond sterile expected value calculations, and the more importance you place on your pet’s life and comfort, the less willing you are to roll the dice…but the point is that on the surface, it’s not entirely clear to me pet owners feel they need insurance for their pets. But can they be made to think they need it? There’s some evidence to believe that they can: the number of pets covered by Trupanion has compounded by 25%/year since 2011 to over ~360k and nearly 85% of members renew their policies every year…and half the lost profits of those who don’t renew are offset by existing members who insure more pets or refer their friends. The proselytizing efforts begin with the 40,000+ vets staffed at the 28,000 vet hospitals across North America (20,000 of which are independently owned and operated) who deliver ~54% of TRUP’s new members and from whom pet owners seek trustworthy guidance. [According this recent Motley Fool interview[1], Trupanion’s CEO claims that when vets recommend Trupanion to their clients, 1 in 4 people enroll.]

Sometimes oblique coverage restrictions, annual payout caps and long waiting periods for covered treatments are buried in fine print; other times, the insurance company and the vet charge based off different fee schedules, with the pet owner paying for the entire procedure out-of-pocket based the vet’s fee schedule only to be reimbursed weeks later by the insurance company using a lower “usual and customary” rate [which is based on fees charged by other physicians in the surrounding area for the same procedure]. A vet probably won’t be blamed for not proactively recommending pet medical insurance, but pushing a policy that culminates in an expensive “gotcha” moment is poison. Trupanion attacks these causes of friction and confusion by:

1/ pricing off the cost of care. Trupanion carefully estimates the cost of medical care across 1mn+ dimensions – species, breed, zip code, deductible, age – and simply tacks on 30% to arrive at the policy price paid by the pet owner…so, a pet owner is basically paying a 30% premium above expected medical costs to rid herself of cost uncertainty. Trupanion then pays out 90% of the vet’s invoice, with no limits per claim or illness. So, it doesn’t matter if one vet charges $2,000 and a rival vet across the street charges $1,000; Trupanion will cover 90% of the eligible treatment cost in both cases. Assuming Trupanion has accurately estimated the cost of care, in aggregate, 70c of every premium dollar Trupanion collects goes to paying vet invoices;

and

2/ re-directing reimbursement flow (in progress). With traditional pet insurance, the patient covers the entire vet invoice upfront and then hopes the check that arrives from the insurer in 2 weeks will reimburse her for the “right” amount. While most of Trupanion’s claims are still paid via check, they are increasingly routed through Trupanion Express, in which Trupanion pays the vet 90% of the bill directly, thereby taking the burden of up-front payment away from the consumer. Express can be integrated into practice management software so that an invoice is immediately shot over to Trupanion, who wires the requested funds into the vet’s bank account in less than 5 minutes. The number of vet hospitals with Express installed has grown from 89 in mid-2014 to 500 in 2015 to ~1,300 today, with over 30% of vet invoice dollars channeled through Express, on its way to 95%+. No other competitor in the space is even bothering to pursue a similar direct payment scheme.

These two changes largely lift the confusion attending discrepant pricing schedules and alleviate the strain of what in some cases could be an enormous immediate upfront payment for the pet owner, followed by an anxiety-ridden reimbursement interval. The member knows his out-of-pocket burden from the get-go and will not be financially surprised down the line. And because a Trupanion member need not wrestle with the financial uncertainty of costly medical care, she spends twice as much on vet services over her pet’s life than an uninsured pet owner…and the vet can simply focus on recommending the best treatment, without also stressing over the owner’s ability to pay.

Even so, considering the history of disappointing experiences with pet medical insurance, it’s no wonder that winning over vets has proven a laborious process. It can take 3-5 visits for a Territory Rep to even get her first meeting…so, if the TR is making 1 visit every 6 months, we’re talking years. Trupanion makes close to 100,000 face-to-face vet visits every year, with 200 hospitals per territory visited every 60 days (with touch frequency now increasing with impending account manager build out), and even after hammering away at vet conversion for nearly a decade in the US, the company still has significant work ahead: against a universe of 25,000 addressable hospitals in the US, only 8,100 are actively recommending Trupanion today, a figure that is growing by ~500-600 hospitals/year. Competitors, on the other hand, continue to take a direct-to-consumer approach, carpet bombing their territories with online marketing to create awareness, which in the absence of vet buy-in has not proven very effective.

Building trust is a time consuming process that requires TRs to persistently contact vets, who must then observe positive customer experiences firsthand. These relationships cannot be bought, but must be earned over time: a vet hospital will not compromise a pet owner’s continuing business for referral fees and besides, Trupanion does not offer kickbacks of any kind to vets for referring patients. You may be surprised to know that with the exception of VPI Nationwide, the largest player in the space with 40% share (vs. #2 Trupanion with 20%), other competitors like Healthy Paws and Pet Plan don’t underwrite the policies they sell. Trupanion’s conceit is that by owning all links in the chain – from sales to underwriting to claims processing to customer service – and forgoing reinsurance, it can provide insurance at a ~20% lower cost than peers. These savings are used to cover a greater proportion of claims costs – 70% of premiums at Trupanion vs. closer to 50% for peers – enabling a “no-fuss” payments experience that induces greater satisfaction from pet owners (who remain Trupanion members for longer) and buy-in from vets (who feel comfortable enough to recommend Trupanion to new clients).

Of course, sustainably profiting off a cost-plus model and credibly delivering on the promise to immediately cover 90% of whatever invoice requires precise, granular insight into the cost of pet acquisition and medical care. Over 17 years since inception, with data from 1.5mn+ claims and over 500,000 invoices/year, Trupanion has amassed cost and retention experience across 1mn+ category permutations…so, for instance, the company understands how the claims experience of a 5-year old bulldog in zip code 11201 differs from that of a 3-year old Shih Tzu in 60047 and can price the two pets accordingly. There are no short cuts to this process. The time required to build claims experience and flesh out statistically significant patterns at such a granular level is a steep learning curve that even a well-funded competitor cannot easily surmount. Although VPI Nationwide has been around longer than Trupanion, their dataset is less robust because they don’t price their policies with nearly as many observations (zip code, for instance) as Trupanion, nor do they cover congenital and hereditary conditions. [to be clear, Trupanion doesn’t cover pre-existing conditions either, but unlike other insurers, it doesn’t refuse coverage on all future illnesses arising because of pre-existing conditions].

Still, while data may be a competitive advantage in the early stages of penetrating a market niche, I’m not sure this in itself constitutes a real moat. Data has to be proprietary, valuable, and part of a self-reinforcing process (data network effects) for it to count as a sustainable edge. There’s a reason why you never hear insurers tout data as a unique advantage…there are diminishing returns to data as the relationship between price and insured risk doesn’t change all that much for granular exposures and eventually becomes common knowledge.

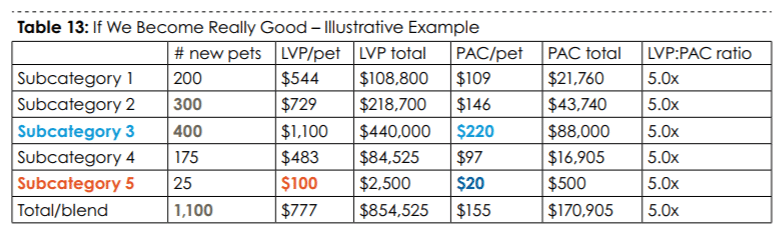

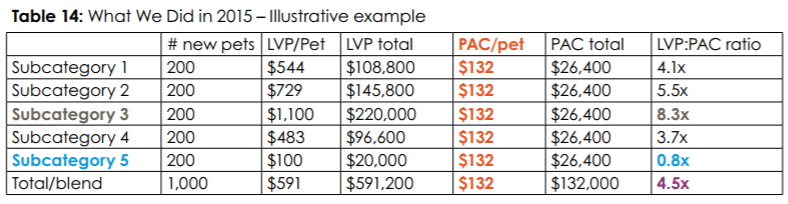

(the Lifetime Value of a Pet (LVP) to Pet Acquisition Cost (PAC) ratio that Trupanion reports every quarter is the blended output of explicit LVP:PAC targets across a slew of subcategories. So, while the lifetime value of, say, a 2-year old cat in Manhattan with a $1,000 deductible will differ from bulldog puppy in Pittsburgh with no deductible, Trupanion can toggle pricing and acquisition spend to get iteratively closer to a common IRR across subcategories, with no cross-subsidization between them. Ideally, the table would look something like this…

Not. quite. there. yet…

…

(Tables 13 & 14 from Trupanion’s 2016 Annual Letter)]

Meager pet insurance adoption rate in North America (< 2% of ~180mn dogs and cats) compared to certain Western European countries (25% in the UK, 50% in Sweden), is an oft-touted part of the bull case. Of course, one wonders why, when pet insurance has been available in America since at least the mid-80s, the disparity exists in the first place? I don’t really know. But one reasonable-sounding explanation I’ve heard is that in Western Europe, pet insurers launched by first winning over vets and those vets then pushed the product to consumers…whereas in the US, insurers started by asking “what price will pet owners pay for this thing called ‘pet insurance’?” and then reverse engineered a product without consulting the vets, yielding something that both consumers and vets hated.

In any case, it doesn’t really matter. I think we just want to see that the method to driving category adoption is sound. In an embryonic market, it’s up to pioneering companies to create the category. Pet medical insurance is so nascent in the US that although Trupanion continues to claim share – there are around 20 brands that make up the pet insurance space, but 2 players, VPI Nationwide and Trupanion, account for 60% of the insured pets – it does so in a market that, against the broader population of insurable pets, barely exists. Rather than look to foreign countries for cues, it seems better to just make a judgment call on whether a) the value proposition for vets makes sense, b) the company has the will and wherewithal to push the ball forward, and c) the product, when discovered and used by the end consumer, solves a real need (including a need the consumer previously didn’t even know she had). a) and c) are tied at the hip since, as previously discussed, vets will only pitch Trupanion if the pet owner perceives benefit. While I harbor doubts about the intrinsic value to a pet owner, those personal reservations are trumped by nearly a decade of data strongly supporting the claim that yes, pet insurance is becoming a thing in the US. As born out over many cohorts, the average life of a Trupanion member is around 6 years…

…during which period the company pulls 20c in variable profit from every incremental premium dollar, reinvesting most of that into acquiring new pets…

….at compelling lifetime values translating into huge IRRs, leveraging sales & marketing and fixed expenses along the way.

The IRR math works roughly as follows: on average, Trupanion pays $175 to acquire a pet and recognizes premiums of around $53 for that pet each month over 71 months. That 53 bucks is whittled away like so:

Monthly premium: $53

Vet invoices: ($37) [70% of the $50 premium]

Variable expenses: ($5)

Contribution profit: $11 [20% of premiums. The Lifetime Value of a Pet (LVP) is computed off this figure]

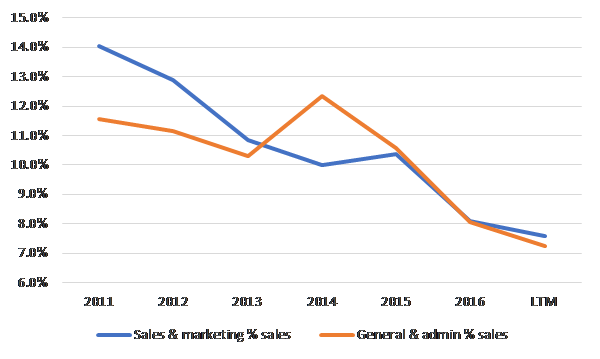

After adding back sales & marketing, Trupanion’s trailing 12 month EBITDA margin after stock-comp is ~8%, implying fixed costs of ~12% of premiums [20% contribution margins less 8% EBITDA margins ex. sales and marketing], so 60% of contribution profits are being consumed by fixed operating costs at the moment.

But at scale, which management pegs at ~700k pets (vs. over 360k today growing low/mid-teens y/y), the company thinks it can do 15% adjusted operating margins excluding the cost of adding new pets. When we back off 1%-2% for stock comp, it’s maybe more like 13%. Given the degree to which Trupanion has leveraged its cost structure over the last 6-7 years, I find this claim credible.

And so, at scale…. .

Fixed expenses: ($3)

Capital charge: ($0.6) [8% x (monthly premium divided into a premium:surplus ratio of 6x)]

Profit/pet/month: $7 [13% of premiums]

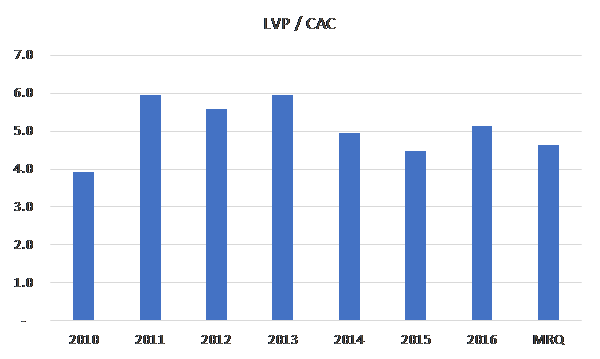

In other words, the company is generating ~$520 in profits over the average lifetime of a member, around 3x the cost to acquire that member. The cash flow streams over ~71 months impute a 65% IRR. Alternatively, at a 15% discount rate, the present value of cash flows over of a subscriber’s life is ~$330, nearly twice the cost of acquisition. Imputing attractive unit economics, of course, requires a sufficiently wide LVP-PAC spread. The $175 pet acquisition cost that I am using assumes the current LVP/CAC of 4.5x, where it has roughly been for the last 5-6 years. This figure would have to decay to below 2.5x before the NPV of pet acquisitions turns negative (i.e. destroys value).

But I see no reason to expect such a draconian deterioration and in fact, it’s possible that as the company further densifies its markets with vet allies, layering on radio and TV spend may even boost conversion from vet recommendations, as has been true thus far in Trupanion’s mature markets where half or more of vet hospitals actively recommend Trupanion.

Given the unit economics and the runway, it’s not hard to see how things can get interesting [though whether they can get interesting enough to buy the stock at today’s valuation is an entirely different question]. Assuming today’s annual PAC spending of ~$15mn/year grows by a few million per year and even assuming LTV/CAC deflates to below 4x, I can get to just over 800k enrolled pets in year-7, around 12% growth per annum. Absent some “silver bullet for cost effective accelerated organic growth” (company’s words), management seems determined to fund its expansion entirely with internally generated profits.

Applying a pre-PAC scale margin of 13% to implied revenue gets us to around $70mn in pro-forma EBITDA, which, assuming reinvestment, will be growing by low-teens, providing still more ammo for pet acquisition. With 800k enrolled pets against a universe of 180mn dogs and cats in North America, Trupanion will still not have even nicked the surface of its potential…so, still be plenty of opportunity to deploy maybe 40%-50% of pre-PAC EBITDA into onboarding pets at 40%+ IRRs. In theory at least. What you’ve just seen is the rabbit. But what about the duck?

After all, this is still an insurance company and balance sheet strength reigns paramount. But is it and does it? Trupanion’s underwriting leverage – premiums to surplus ratio, a measure of how much underwriting risk you are assuming relative to the capital you hold – is greater than 6x [Trupanion does not reinsure its risk, so subscriptions = gross premiums = net premiums]. Whether this exceeds the standard of prudence depends on the nature of risk being insured. Typically, a ratio greater than 3x is considered unusually aggressive for a P&C underwriter and an insurer with significant high-severity natural catastrophe exposure will keep it closer to 1x. Health insurers, in contrast, will underwrite 7x+ their surplus. In my experience, growth and conservative underwriting are hardly ever simultaneously executed well together, and if this were a run-of-the-mill P&C underwriter, Trupanion’s thin capital base would probably be reason alone to pass.

But I think Trupanion is a different animal. The risks covered under pet medical insurance are bite-sized and absent a major, widespread health contagion, uncorrelated. Agglomerating hundreds of thousands of claims results in a more predictable range of experiences from year-to-year at the population level than most traditional P&C exposures and with far less tail risk too. Given the highly granular, uncorrelated nature of the insured risks, catastrophe is a remote risk. The company’s exposures are also short-tailed, meaning that claims-triggering events are readily apparent and the costs from those events accurately estimable and paid soon thereafter: over 90% of the company’s reserves as of 3q17 are related to activities incurred in 2017 and close to 95% of claims paid over the last year was related to business underwritten in the same year. Only a miniscule amount of claims incurred and paid relate to prior years. [one negative consequence to premiums heading out the door to pay claims almost as soon as they come in is that Trupanion doesn’t benefit from “float” income as a typical insurer does].

Compare this to the “long-tail” risk of asbestos, where the health consequences from exposure remained latent for many years and claims were still being paid more than decade after policies were originally underwritten…that is, people were getting silently screwed by asbestos during the coverage period; the insurance companies didn’t know it at the time and so didn’t properly reserve for it.In contrast, the short-tail nature of Trupanion’s risk means that its best guess about claims cost and frequency is rapidly (in)validated and any deviations can be dynamically accommodated through price adjustments. While Trupanion won’t hike a member’s monthly subscription fee based on her pet’s individual medical condition, it will do so if the average cost of care for all pets within the same sub-category rises, so systematic pricing errors are quickly rectified. Steering the ship is 48-year old founder, CEO, and ~8% owner Darryl Rawlings, who has a good story about how his parents’ experience about not having the money to remedy a life-saving procedure for his childhood dog, prompted him to start Trupanion 10 years later (maybe too good a story?). In any case, I highly recommend reading his annual letters, which are refreshingly exorcised of hygienic corporate bullshit and lay out Trupanion’s operating strategy with a useful degree of granularity. Darryl seems authentically enthusiastic about this pet insurance mission and appears to “get” how value is created…it’s hard to imagine a diversified underwriter/bank/savings institution like Nationwide pursuing this opportunity with the same single-minded vigor.

[MCO – Moody’s] The Self-Reinforcing Standards Moat

Posted By

scuttleblurb

On

In

SAMPLE POSTS,[MCO] Moody's Corp |

Comments Disabled

Moody’s is a Nationally Recognized Statistical Rating Organizations (NRSROs), a title bestowed by the SEC on a handful of credit rating agencies, the top 3 of whom act as an oligopoly in the US debt ratings gambit. As you well know, Moody’s (and S&P and Fitch) fell into disrepute during the last financial crisis when its ratings on vast swaths of corporate and securitized paper proved worthless, its grossly conflicted issuer-pay model laid plainly bare. But testament to the company’s resilient business model, and toothless fines and regulatory censures notwithstanding, Moody’s Investor Service (“MIS”, the credit rating agency side of the business that constitutes ~2/3 of revenue and ~85% of EBITDA) has thrived since the crisis, compounding revenue and EBITDA by 10% and 15%, respectively, since 2009 and generating more of each vs. the 2007 peak:

MIS segment, $ millions

2007

2009

LTM

Revenue

1,780

1,218

2,550

EBITDA

1,021

543

1,555

% margin

57%

45%

61%

Over the last 100+ years since its founding, Moody’s ratings – derived from a consistent framework applied across 11k and 6k corporate and public finance issuers, respectively, in addition to 64k structured finance obligations – have become the veritable benchmark by which market participants, from investors to regulators, peg the credit worthiness of one debt security against another. NRSRO ratings underpin the risk weightings that banks attach to assets to determine capital requirements, dictate which securities a money market fund can own, and, in ostensibly surfacing the credit risk embedded in fixed income securities, make it easier for two parties to confidently price and trade, enhancing market liquidity. I was a research nerd in the bond group at Fidelity just prior to and during the crisis. It’s hard to overstate just how tightly Moody’s and S&P (and to a lesser degree, Fitch) ratings were stitched into the fabric of our ratings and compliance infrastructure and the day-to-day workflows of analysts and traders on the floor.

Because of such industry-wide adoption, a debt issuer has little choice but to pay Moody’s for a rating if it hopes to get a fair deal in the market: an issuer of $500mn in 10-year bonds might pay the company 6bps upfront ($300k), but will save 30bps in interest expense every year ($15mn over the life of the bond)….and each incremental issuer who pays the toll only further reinforces the Moody’s ratings as the standard upon which to coalesce, fostering still further participation. This feedback loop naturally evolves into a deeply entrenched oligopoly. In terms of total ratings issued, S&P and Moody’s are at the top of the heap. There are actually 10 NRSROs, but unless you work in credit, you’ve probably never heard of most of them (Egan Jones anyone?)

The government’s determination of NRSRO status is premised on “whether the rating agency is ‘nationally recognized’ in the United States as an issuer of credible and reliable ratings by the predominant users of securities ratings” (per this SEC report[2]), which criteria itself is in part tautologically attributable to the government’s NRSRO designation in the first place. And when things go horribly wrong and these ratings are shown to be the reactive measures that they are, the agencies simply appeal to freedom of speech protection under the First Amendment.

This is a really hard business to screw up. Who wants to rock the boat? Certainly not the staid management team at Moody’s, which thrives on 5 year plans, formulaic capital allocation policies, and farcically granular guidance that plays to the myopic expectations of sell-side model tweakers (though I give management props for expensing stock comp in its adjusted profit numbers). You will never see Moody’s carve out an “Other Bets” P&L for new innovations. Day One will always be yesterday. [If watching Sundar Pichai saunter on stage to fulsome fanboy applause against jubilant theme music from Fitz & The Tantrums provokes reflexive eye-rolling, then do yourself a favor…watch the 2016 Moody’s Investor Day webcast and take refuge in the sterile quietude of a generic albescent conference room where every cough and throat clear is awkwardly amplified against the AV projector’s fan’s sad whir.]

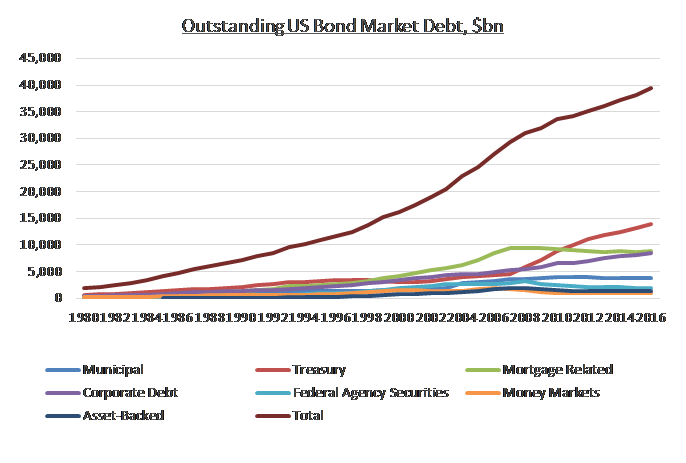

MIS’ 2016 revenue was about 60% transactional (tied to new debt issuance) and 40% “recurring” [per 10K: annual fee arrangements with frequent debt issuers, annual debt monitoring fees and annual fees from commercial paper and medium-term note programs, bank deposit ratings, insurance company financial strength ratings, mutual fund ratings], a mix that has been reasonably stable during the quiescent issuance environment of the last 5-6 years. Debt issuance in the US, which constitutes nearly 2/3 of MIS revenue, can be choppy from year-to-year….

Source: SIFMA

…but the overall stock of debt has been steadily growing…

Source: SIFMA

…so, as you might expect, MIS’ recurring revenue has served as a reliable anchor during stormy issuance periods.

MIS segment, $ millions

Revenue

Transactional

Recurring

2007

1,204

576

2008

591

614

2009

612

606

2010

800

605

2011

903

666

2012

1,173

714

2013

1,281

779

2014

1,372

875

2015

1,419

902

2016

1,430

930

LTM

1,616

934

Still, recurring profits did little to cushion the punishing issuance swoon during the last recession. Revenue from corporate and structured finance bond issuance declined 26% and 53%, respectively, from 2007 to 2008, forcing a ~$575mn revenue decline that translated into a $450mn EBITDA hit.

MIS segment, $ millions

Revenue*

EBITDA

2007

1,780

1,021

2008

1,205

632

2009

1,218

603

2010

1,405

685

2011

1,569

804

2012

1,887

991

2013

2,059

1,116

2014

2,248

1,277

2015

2,304

1,307

2016

2,340

1,255

LTM

2,550

1,555

* excludes a negligible amount of “other”

non-ratings revenue

We don’t know the profit split between transactional and recurring profits (and I don’t even know if such a determination is possible since labor is the biggest component of SG&A and allocating the cost of an analyst’s time between new issuance and maintenance work feels like arbitrary hair splitting). But, I think we can confidently say that non-recurring revenue per dollar of new issuance is way larger than recurring revenue pulled from each par dollar of the rated installed base, and so big swings in transactional revenue have a disproportionate impact on profitability…though, keep in mind that heavy debt issuance in a given period adds to the stock of outstanding debt and thus the monitoring fees earned in future periods.

Given the lofty contribution margins attached to new issuance, the prospect of a reversal has been a source of trepidation for me. Transactional revenue growth has proceeded at a strong, though not torrid, 12% pace over the last 6-7 years as issuers have seized on a stubbornly low rate environment to refinance debt and add leverage to their balance sheets.

Meanwhile, outside a commodity-driven hiccup in 2016, high yield default rates are well below the historic average (which should give you pause if you believe in cycles and mean reversion).

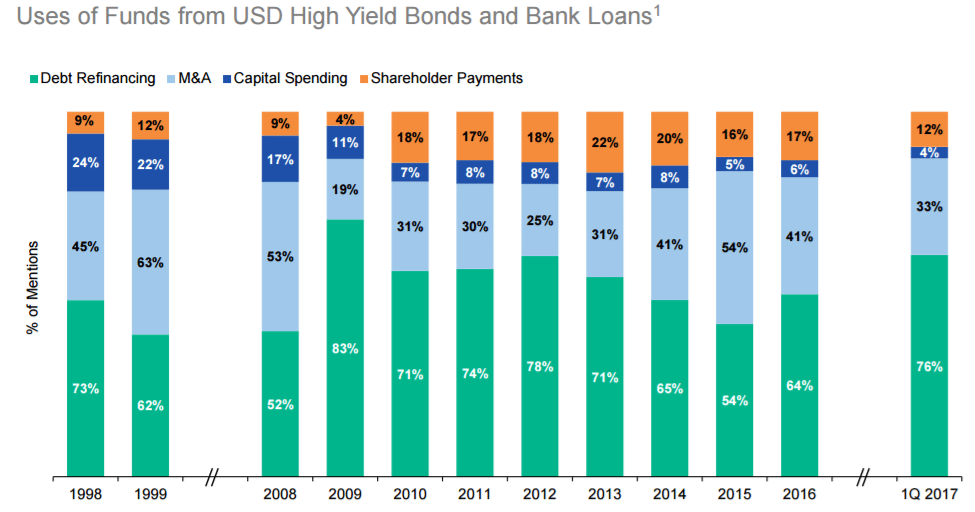

[Aside: the below exhibit, which breaks out the uses of funds from high yield bond and bank loans, is interesting in its own right. In the late 1990s, 20%-25% of companies that raised funds cited internal investment as a reason for doing so vs. just a mid-single/high-single digit percentage today.]

I’m being unhelpfully obvious when I say that credit conditions feel toppy. But even if mean reversion is impending, 2008/2009 seems an inappropriate analog since not only is the catalyst driving systemic financial concerns that loomed so large back then less relevant today, but also a significant chunk of the company’s pre-2008 profits came from its reckless rubber-stamping of toxic asset-backed securities.

(MIS revenue, $mn)

2007

2008

2009

2010

Structured Finance

868.4

404.7

304.9

290.8

% change

-0.5%

-53.4%

-24.7%

-4.6%

Non-Structured Finance

911.5

800.0

912.8

1,114.2

% change

18.8%

-12.2%

14.1%

22.1%

EBITDA

1,020.5

568.7

543.0

623.5

% change

4.8%

-44.3%

-4.5%

14.8%

Disaggregating MIS’ revenue streams per above, we see that outside of structured finance, the revenue declines were actually not sooo bad during the worst financial crisis in decades, thanks of course to issuance stoked by aggressive rate-deflating monetary policy measures. Structured finance grew from just $384mn in revenue in 2002 to $873mn in 2006 (an 18% CAGR) and was so profitable that even while non-SF revenue grew by 14% in 2009, overall MIS EBITDA still declined as SF revenue contracted by another 25% from 2008’s harrowing 53% decline. I don’t believe MIS has significant revenue streams tied to comparably negligent and profligate underwriting today, and would expect the profit hit from a cyclical correction to be far more muted.

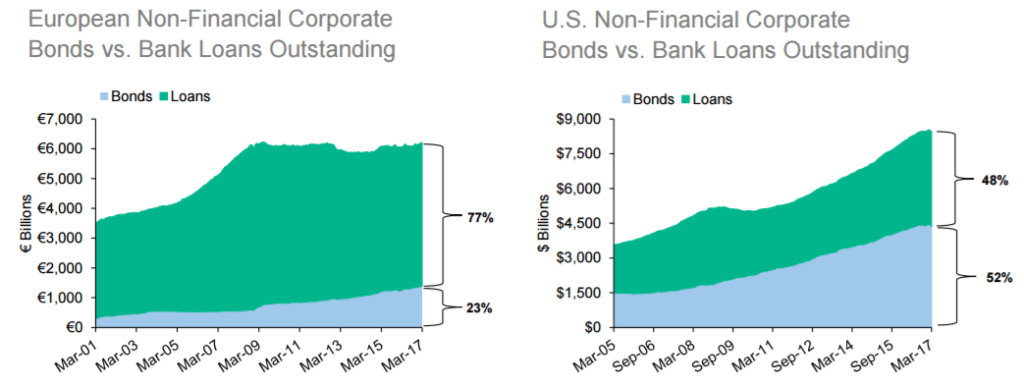

Also, due to the surge in 7-10 year paper subsequent to the financial crisis – MIS’ non-structured revenue increased by 17%/yr from 2008 to 2012 – the refinancing needs over the next 4 year period (2017 to 2020) are 30% greater than they were from 2013 to 2016, providing an intermediate tailwind to transactional revenue, though 1h17’s whopping 30% y/y growth in corporate finance revs is clearly testament to some pull-forward of refinancing needs. Debt issuance cycle aside, companies have been increasingly tapping the capital markets, rather than banks, for their debt funding needs. In Europe, bonds constitute just 23% of non-financial debt [bonds + bank loans] outstanding vs. 52% in the US, with the mix shifting in favor of bonds over at least the last decade.

Management thinks that disintermediation (+2%-3%) plus debt issuance prompted by global GDP growth (+2%-3%) plus pricing (+3%-4%) should sum up to around ~high-single/low double digit revenue growth through the debt cycle, which sounds reasonable to me and is consistent with the 9% revenue CAGR MIS has realized since 2011. And on top of that, there’s another 2%-3% contribution from Moody’s Analytics, MCO’s less good business segment that offers a range of risk management, research, and data products and services, and constitutes about 1/3 of revenue and 16% of EBITDA (corporate overhead is already allocated to business segments). Almost all of the ~$1bn that the company has spent on acquisitions (out of cumulative free cash flow of ~$8bn) over the last decade through 1q17 has gone towards bolstering MA, mostly small tuck-ins.

Then, on May 15, 2017, management announced the €3bn acquisition of Bureau van Dijk. Moody’s is spending 3x more on this one acquisition than it has on the sum of all previous acquisitions over the last decade. BvD is an Amsterdam-based company that aggregates data on 220mn private companies across a wide range of geographies and industries and makes it available in hygienic, organized form to 6k corporate and government customers. This acquisition will be “tucked into” RD&A [In 2016, about 54% of MA’s revenue came from “Research, Data, and Analytics,” which is really just an extension of MIS insofar as it realizes revenue by selling research and data (analysis on debt issuers, economic commentary, quantitative risk scores, etc.) generated in MIS. The quality of RD&A mirrors that of the ratings segment, with 95% retention rates driving hsd revenue growth (90% organic) from hsd pricing and volume since 2011], boosting its revenue by ~43% (and contributing ~8% to MCO’s total revenue). BvD does not own the data, but rather licenses it from 160mn obscure data providers in various jurisdictions before “cleansing” and standardizing it for subscribers who use it to, for instance, better assess credit risk, conduct M&A due diligence, set transfer pricing reporting policies and docs for multinationals, and identify potential B2B sales leads.

Management claims that this business benefits from network effects, by which I assume they mean that the license fees BvD pays to suppliers are pegged to the number of users of that data and so more users compel more suppliers to make their data available to BvD, which in turn draws more users. Going off the high-level historical financials provided by Moody’s, BvD has performed like a truly kick-ass asset, with revenue expanding at a steady 9% CAGR (all organic) over the last decade, growing every year right through the recession, and EBITDA margins expanding from 39% in 2006 to 51% in 2016. But great assets go for great prices. MCO is paying a lofty 12x revenue and 23x EBITDA at a time when its own stock traded at “just” ~14x at the time of announcement. €3bn is triple what private equity firm EQT paid for BvD less than 3 years ago. One might argue that if we extrapolate the last decade’s 12% annual EBITDA growth out 5 years (which might actually be reasonable given the seemingly predictable, consistent nature of the business) and apply estimated out-year synergies ($40mn revenue / $40mn costs), we’re looking at €295mn in 2021 EBITDA, which puts the multiple at ~10x, but even management concedes that it is reaching on valuation and falling short of their typical 10% cash yield target on this one. The revenue synergies seem fairly modest (14% of revenue, 5 years out) and sensible on the surface. For various reasons BvD has found it difficult to break into the US market (unlike regions outside the US, financial data on private companies in the US is sparse…plus, BvD who?) and still derives 3/4 of its revenue from Europe.

Moody’s can bundle BvD’s datasets into MA’s analytics products and sell a more robust bundle to its US customer base. [Notably, MA already feeds BvD’s data into the loan origination solution it sells to financial institution clients and some MA customers already use BvD data to drive their credit models] and cross-sell MA products into BvD’s customer base. Finally, BvD’s dataset on smaller, private companies gives MIS the opportunity to provide credit ratings to the underserved SME market, though this seems like a more distant aim. [Here’s a high-level summary of Moody’s business mix post-BvD; MA gets a nice margin lift and its EBITDA increases from ~17% of consolidated to nearly 1/4.]

(MCO LTM + BvD 2016, $ millions)

MIS

MA

MA+BvD

Revenue

2,550

1,272

1,560

EBITDA

1,555

290

438

% margin

61%

23%

28%

Still, most of management’s justifications – the acquisition reduces the volatility of the ratings business, is accretive to per share earnings, accelerates growth forecasts, gets the company access to new revenue opportunities like transfer pricing and tax planning that have little to do with the core ratings business – have jack to do with value creation and reek of generic Wall Street pandering. And while BvD’s business seems good enough on its own merits that I don’t think the acquisition will be grossly value destructive, it’s tough to credibly claim that much incremental value has been added at this lofty purchase multiple.

Outside of RD&A, there are two other business lines: 1) Enterprise Risk Solutions (11% of post-BvD revenue; risk management software and services…basically, financial institutions use Moody’s tools to create credit, market, and operational risk tables and make them available to their regulators; has grown revenue by ~11% organically over the last 8 years) and 2) Professional Services (4% of post-BvD revenue; financial training and certification, mid-single digit organic revenue growth since 2008….seems like a pretty mediocre business, but one which management insists is an important entry point to the customer). Taken as a whole, Moody’s Analytics is just “meh” compared to other data and analytics peers, in my opinon. Great analytics businesses tend to have self-reinforcing data feedback loops, which are not very relevant to MA.

[Here is what I wrote about Verisk: The company sits at the center of a network that procures data from a wide variety of sources on one side (claims settlements, remote imagery, auto OEMs, name your buzz word – smart cars, smart watches, smart cities) analyzes it, and spits out predictive risk and customer insights to their clients on the other (insurers, advertisers, property managers). The agreements through which a customer licenses VRSK’s data also allows the company to make use of that customer’s data, so essentially the customer pays Verisk for a solution that costs almost nothing for the company to deliver and Verisk gets to use that customer’s data to bolster the appeal of its own products, which improved solutions reduce churn and attract even more customers (and their data) in a subsidized feedback loop.]

Its solutions seem more akin to templated reporting and risk management to sate regulatory requirements than data-fueled machine learning algorithms to drive business outcomes. Management continuously talks about realizing synergies from tuck-ins and driving operating leverage, but the fact of the matter is that MA margins have gone nowhere for years and I think it’s fair to say that this side of the company has disappointed expectations. So, stepping back…nearly 80% of MCO’s pro-forma EBITDA comes from a ratings business that has long established itself as the de facto credit risk benchmark, relied upon by all significant players in the fixed income ecosystem. But while MIS is a structurally advantaged business that will continue heaping value over time, because 60% of MIS is high-margin transactional revenue tied to new issuance, it is also unavoidably cyclical, and conditions today seem about as good as they will get. Through the cycle, MIS is a steady high-single digit revenue / low-double-digit EBITDA grower generating prodigious free cash flow (30% of revenue converts to free cash flow). Most of it will be mechanically dedicated to buybacks and dividends, which is probably just as well since its tuck-in acquisitions have had little to show, and I suspect the same will be true of BvD. At $134, the stock trades at 18x/23x my estimate of pro-forma LTM EBITDA/cash EPS. The EBITDA multiple is about as high as it has been in decades (matched only in late 2005/early 2006) on what in retrospect will likely turn out to be cyclically peak earnings. Moody’s is a great business and is priced accordingly, though with a long enough time frame, a buyer will probably do just fine even at the current valuation.

[CPRT – Copart; KAR – KAR Auction Services] Copart is a Beast + Impending IAA Spin-Off from KAR

Posted By

scuttleblurb

On

In

SAMPLE POSTS,[CPRT] Copart,[KAR] KAR Auction Services |

Comments Disabled

Beneath the bustle of a used car lot lies a swarm of activity that few of us have ever seen, a thriving ecosystem of wholesalers, rebuilders, parts recyclers, insurers, and intermediators whose trading activities usher some vehicles to dealer lots for resale and others to repair shops or salvage auctions. Roughly 45mn used cars are sold in the US every year. 10mn+ of those are consumer-to-consumer private transactions that take place on eBay, Craigslist, and the like. The other ~30mn+ are captured by a fragmented base of over 40k used car dealerships (CarMax, Penske, Asbury, etc.) strewn across the country, 10mn of which are sourced through wholesale auctions…so, you might trade in your Chevy Bolt for a new Toyota Camry, but that Toyota dealer doesn’t want a Chevy sitting on the lot and so will sell that trade-in at a wholesale auction, through which the vehicle will find its way to a GM dealer. This being an auction market with two-sided network effects, wherein buyers attract sellers and sellers attract buyers, you will not be surprised to learn that value lopsidedly accrues to just two companies – KAR Auction Services, through its ADESA subsidiary, and Cox, through its Manheim subsidiary – who together process ~70%-75% of the market. This is not the only oligopoly in the auto value chain.

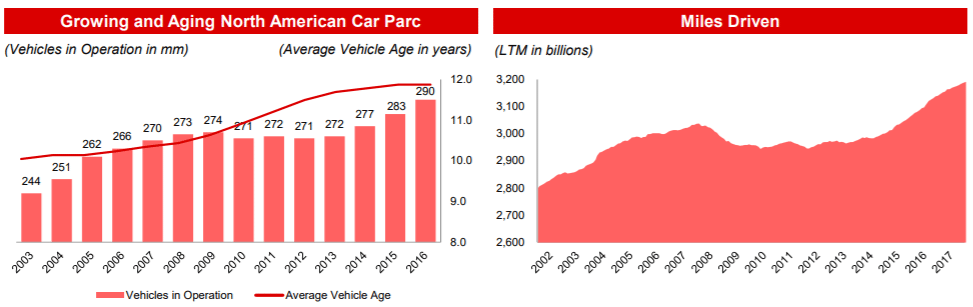

The salvage market is also an auction and, in the US, also dominated by two companies, Copart and Insurance Auto Auctions (IAA), who each have roughly ~40% share, with the next largest operator claiming just 3%. But unlike the whole car auction market, which is closely tied to transaction “flow”, salvage auto auctions are supported by the “stock” of outstanding vehicles, providing a stable source of volume as every year some reasonably predicable percentage of the ~280mn cars on US roads get into accidents and sometimes those accidents are serious enough that the cars involved must be pulled off the road entirely. Around ~13mn are removed from the fleet every year(1), of which 4mn are siphoned to salvage auctions that are more likely than not operated by either Copart or IAA. Insurers bring 80%-85% of the cars that run through these auctions, though no single customer accounts for more than 10% of Copart’s revenue.

The other side, the buyer side, is more fragmented: sometimes dealers or repair shops buy the whole car and rebuild it, sometimes they dismantle it for parts and, in the case of LKQ, sell those parts to collision repair shops, who buy from LKQ to appease cost conscious insurers directing huge repair volume to shops using less expensive recycled parts for damaged cars. I’ve heard LKQ described as a business with low entry barriers, but actually, it can be quite difficult to replicate the scale advantages of a disciplined distributor with relatively superior local route density. Tens of thousands of mom-and-pop collision and mechanical repair shops receive unexpected service requests that must be expeditiously handled. Under pressure from insurers, who account for 85% of car repairs and who expect rapid and cost effective service, shops will buy from distributors that can most rapidly deliver the broadest range of SKUs with the shortest lead times at the lowest price, so clustering facilities in such a way that they can be economically loaded with inventory from a regional hub and also near customer premises, affords scale advantages.

Logistics/distribution-type companies with the loftiest returns – Fastenal, MSC, Old Dominion, Copart, Rollins – strongly bias towards organic growth and small tuck-ins relative to peers who undertake splashy “strategic” or “platform” acquisitions. High return stalwarts expand by methodically adjoining adjacent service territories to an existing, heavily utilized logistics base. As I wrote in a prior post:

“FAST is a prime example of how disciplined incremental expansion into adjacent product and geographic space can build to significant competitive advantages over time. In the Company’s case, we see this along three different vectors: 1) geography – from its Midwest origins the company expanded into nearby surrounding territories, building local market density that offered scale advantages in distribution and higher service levels at lower cost to customers; 2) product – FAST leveraged its existing strength in fasteners to expand into non-fastener maintenance and supply; 3) business model – the company is now building on its legacy distribution and store network to offer onsite customer service at a cost that most competitors can’t match.”

Expanding incrementally and leveraging local incumbency is not the path that LKQ has taken. The company has grown its revenue base from less than $1bn in 2006 to over $10bn today largely on the back of acquisitions. It has done 260 of them since its founding in 1998, pushing its presence beyond North America to the UK and continental Europe; beyond recycled auto parts to aftermarket products and accessories distribution for specialty vehicles (RVs and trucks). I don’t know this company intimately well, but its growth strategy feels rather unwieldy, its operational discipline wanting. EBITDA margins in North America, its most mature segment, have expanded by just 80bps over 5 years while European margins have declined. A bull might claim that its profitability profile is distorted by acquisitions, especially in Europe, and that those margins are really expanding on a “look through” basis, but I could just as easily argue that a key source of value extraction in logistics roll-ups comes from layering incremental demand atop existing infrastructure and routes, so margins should be trending persistently higher, roughly concurrent with the tuck-ins themselves.

Rollins, which regularly funds mom-and-pops with internally generated free cash flow; shuts down those acquired branches; and consolidates their customers onto existing routes, has seen its EBITDA margins inflate by over 300bps since 2012 on low/mid-single digit organic growth that is comparable to LKQ’s North America segment. LKQ boasts #1 share in a variety of international markets, but the company purchased that distinction, and as auto parts distributors and the insurers who dictate repair flow operate locally, what is the synergy that LKQ brings to these far flung territories? In its hypothetical pro forma acquisition scenario slide, management claims it is buying companies at just under 5x year-2 EBITDA (8x trailing)…and yet the company’s consolidated returns on invested capital, at ~10%, are unimpressive and have gone nowhere for 14 years. Nor are the low-teens EBITDA margins in North America, the most mature and highest margin segment, indicative of what is typically delivered by a dominant, best-of-breed distributor with massive scale advantages. Auto insurers are a pretty consolidated bunch, with the top 10 accounting for 70% of written premiums. They are offsetting claims cost inflation by pressuring repair shops to use recycled parts that sell for half the price but are nonetheless just as reliable as OEM replacement products, a significant demand tailwind for distributors of recycled salvage parts.

LKQ’s high single digit national marketshare is many times larger than the next largest distributor – competitive differentiation derived from scale economies is relative; it is usually better to have 5% share of a market whose second largest player accounts for just 1%, than to be one of ten players who each have 10% – and so bulls have argued that LKQ is favorably positioned in a static Porter’s 5 Forces framework against the 10s of thousands of defenseless, commodified, and fragmented collision and mechanical repair shops that comprise its customer base. But saying that LKQ has dominant share in North American parts distribution obscures meaningful nuance – i.e. a chain of repair shops may have negligible market share nationally but a dominant presence locally – and says nothing about the change in relative share. Insurance carriers are looking to streamline their claims operations and directing ever more repair flow to a limited number of service providers. This, combined with the growing complexity of auto repairs, which require shops to invest in costly specialized equipment and training, is in turn fueling consolidation among repair shops, whose ranks have dwindled from 65k in 1990 to around 30k today.

Since 2000, the proportion of repair volumes handled by multi-shop operations (MSOs) has gone from ~10% to nearly 40%. Against that context, LKQ’s national network may position it to win a growing share of broader distribution agreements from ever consolidated repair chains, but since the company would no longer be dealing with small mom-and-pops, its relative bargaining position is worse off. Nor does LKQ appear to have meaningful procurement leverage. Even as the largest buyer, LKQ does not comprise even 4% of the total cars sold through an auction industry that is run by just two players. And if you want to argue that LKQ has sourcing advantages outside of salvage, well, where is it? Gross margins have deteriorated over the last 7 years, from 44% in 2010 to 39% in the last 12 months. I don’t think LKQ is a bad company; it just doesn’t seem as sweet an opportunity as typically pitched, in my opinion.

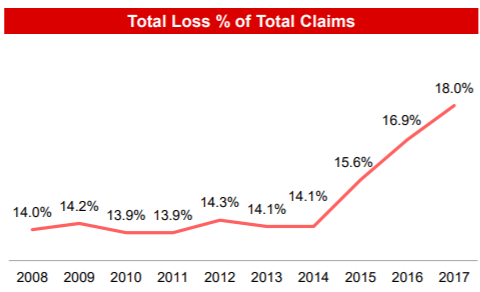

To the extent that the bull thesis rests on responsible international expansion and a favorable view on the broader trends driving accident rates, Copart and IAA seem like superior bets. About those trends. When a car gets into an accident, an insurer must determine whether or not the vehicle is worth saving. It does so by comparing the cost of repairing the car versus the amount it could recognize by deeming the vehicle a total loss and selling it at a salvage auction. So, if a car was valued at $10k before the accident and it takes $6k in repairs to restore the car to its “pre-accident value” and another $1k to supply the claimant with a rental while his car gets fixed, then the insurer will choose to send the car to salvage if it thinks it can get more than $3k for it at auction [that’s $10k less $6k less $1k], and repair the car otherwise. The proportion of cars deemed a total loss has been trending higher over the last several years, driving growth in salvage auction volumes:

[In the early/mid ’90s, the total loss % was more like 10%] For every 5 cars that get into accidents, 1 is sent to a salvage auction, where it might be claimed by recycler like LKQ who sells the parts used to repair the other 4. Ever year, cars are being decked out with more and more safety features and technology – airbags, crumple zones, computer systems, cameras, sensors, navigation systems – making them more expensive to repair and more likely to be deemed a total loss when involved in an accident.

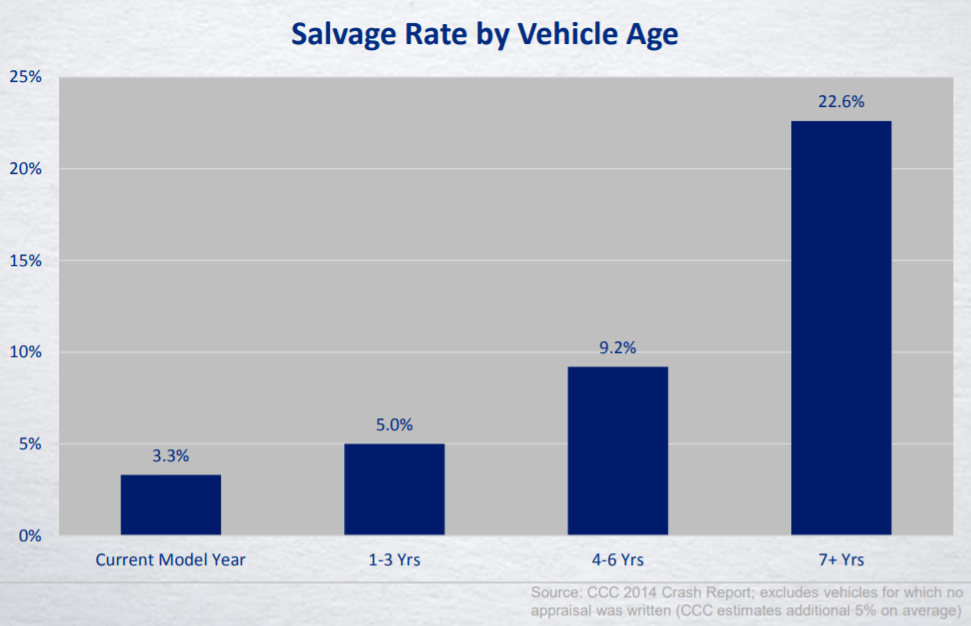

Moreover, mounting consolidation among repair shops, which attenuates LKQ’s bargaining power relative to its customers, conversely helps Copart and IAA, as these MSOs exert pricing power and exacerbate the rising the cost of repairs. Meanwhile, the demand for cheaper recycled parts, which acts as a significant tailwind for LKQ, also helps Copart and IAA as recyclers participate in salvage auctions to source totaled cars for parts inventory. Furthermore, the median vehicle age has gone from ~10 years a decade ago to ~12 years today while the percentage of really old cars in the car parc, those 11 years and older, have grown from 33% of the car parc to over 40%. Older cars are more likely to be salvaged because their repair costs make up a relatively high proportion of pre-accident value, all else equal.

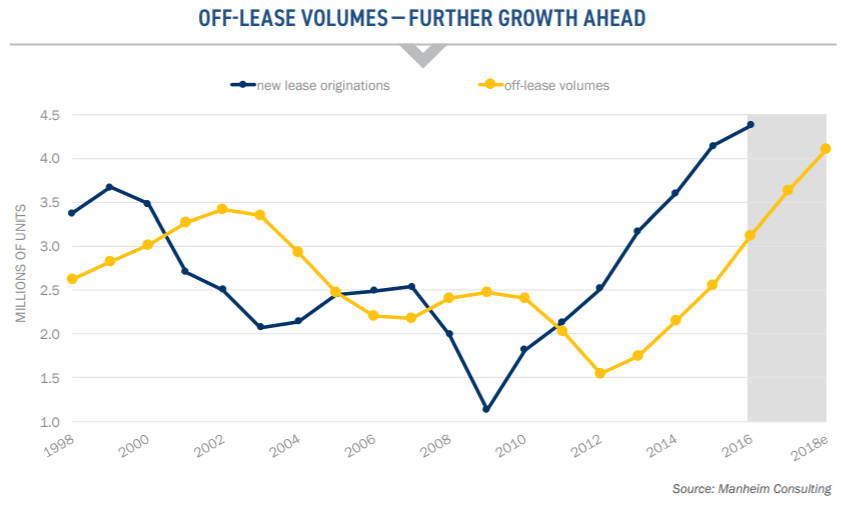

Total loss claims will be further buoyed to the extent that the impending deluge of vehicles coming off lease pressures used car prices (“pre-accident” values will be lower).

[At the end of its lease term, typically ~3 years, a car is returned to the captive finance company, who funnels it to either the wholesale or salvage auction market. The growing proportion of leased cars in recent years – in 2010, less than 13% of new car transactions were leases; today, that figure is over 30% – continues to provide some support to salvage volumes, but keep in mind that captive fincos are a subset of the less than 20% of Copart’s auction volume derived from non-insurance companies, so it’s not a huge deal(2)]

So, repair costs and salvage auction participation are both going up while, speculatively, used car values are probably going down. The diverging trends provide a happy tailwind for salvage auction activity.

On top of all that, the number of car accidents has been rising along with the number of cars on the road (and correspondingly, the number of miles driven)…

…and after a 15 year stretch during which the number of crashes per million driven miles declined, the crash rate has ticked higher in recent years, supposedly boosted by texting/emailing while behind the wheel: over 30% of respondents from an AAA Foundation for Traffic Safety survey reported texting while driving in the last 30 days; the National Safety Council claims that 1 in 4 crashes is influenced by cell phone use. But, even if this troubling trend proves to be a fluke that reverses, salvage volumes should still continue to grow as they have in past decades, when falling accident rates were more than offset by rising total loss frequencies (which latter are mainly a function of repair costs relative to used car prices, which I’ve already explained are trending higher).

You’ll notice that the constituent drivers of Copart’s revenue growth have naturally offsetting properties that promote growth even when times are bumpy for the auto industry as a whole. For instance, lower average used car prices, in isolation, are ostensibly bad since over half the company’s service revenue [fees charged to vehicle sellers and buyers] is correlated in some way to the selling price of the vehicle…but weaker prices also increase the proportion of repair costs to pre-accident values and makes it more likely that the a car will be totaled rather than repaired. In FY09 (ending July 2009), Copart’s service revenue shrank by less than 1% y/y, as higher salvage frequency and market share gains substantially counteracted the harrowing fallout of the last recession, including not just weaker used car prices, but the headwinds of dollar strength (around 30% of the cars at Copart’s auctions go to international buyers), commodity weakness, and a shrinking car parc. [Cars that are discontinued or built by manufacturers seeking bankruptcy protection, as occurred during the last recession, see their resale values impaired, which also helps salvage frequency.]

Still, looking past the cycles, we have to contend with the longer-term secular trend towards autonomous transportation. Where will pools of value accrue in what will surely be a dramatically transformed ecosystem of OEMs, mechanical parts suppliers, electronic component vendors, repair shops, dealers, etc., and what are the knock-on effects to parking lots, gas stations, urban planning, emergency room visits, and whatnot? I certainly don’t have the answers, but at least on the first question my best guess is that the hardware components enabling autonomy – sensors, LIDAR, cameras – will eventually be commodified and value will flow to those owning the mapping and autonomous driving software required to optimize routes and maneuver through surrounding environments. I’m less sure that excess profits accrue to those purely matching riders to cars because, notwithstanding the cross-side network effects between drivers and riders, the question of customer ownership is rendered fluid by the fact that the drivers (or, eventually, autonomous cars) are not captive and rider switching costs are low.

Mapping and autonomous software benefit from machine learning empowered data network effects – more traversed miles translate into more granular maps and driving scenarios that better utilize and make smarter, all the vehicles in a service fleet – so, a dominant ride-sharing service or autonomous car manufacturer today might bootstrap its way to a competitive advantage founded on maps and software. I don’t know. But 20 to 40 years from now, when fully autonomous vehicles can be readily beckoned in most major metros, there will surely be far fewer accidents than there are today (driver error accounts for 90% of all accidents)? They may get so good, in fact, that a lot of the expensive safety features found in cars today are obviated away. Both developments carry existential undertones for salvage auctions, whose volumes are influenced by both the frequency of accidents and the severity of damage (as measured by repair costs per damaged vehicle).

Copart’s management put out a presentation several years ago that in “skate to where the puck is” fashion, cited some surveys and expert opinions purporting that consumers are resistant to self-driving cars and that the skills of autonomous vehicles do not rival those of human drivers. In the same presentation, management pointed out that there are ~260mn cars on the road and, assuming a ~17mn SAAR and an average car life of 15 years, it takes a really long time for new technology to meaningfully penetrate the car parc. But autonomous vehicles will make a significant impact on accident frequency well before they take over the car parc as every fully functional autonomous vehicle lowers the odds of collision with several other vehicles. How long it will take before we get to a point where this starts to matter is, of course, an open question. With respect to salvage auction volumes, we may be in a sweet spot today where technology is making cars more complicated and expensive to repair and safer for drivers who do find themselves in an accident, but is not yet good enough to materially reduce the frequency of accidents that is at least partially attributable to the modern day scourge of smartphone addiction…and, I can see this state of affairs persisting on the 5-10 year time frame that is relevant to me (and many of you). As long as that’s the case, salvage volumes will likely continue plodding along at a high-single digit rate of growth – fueled by a low-single digit growth in claims, a growing proportion of which result in total losses due to rising repair costs – and value will continue migrating to the two largest players, Copart and IAA, who together share 80% of the US market.

Both companies have built up scale advantages over 35 years that would be very difficult to replicate. [IAA got into the salvage vehicle business in 1982, the same year as Copart. It went public in 1991, grew through a series of acquisitions, was acquired by private equity in 2005, and together with ADESA was merged into KAR auction services in 2007. IAA is now in the process of being spun-off of KAR.] An insurer tries to minimize its claims costs by either minimizing repair costs on the cars it saves or by maximizing the salvage proceeds for those it deems a total loss. The latter is best achieved by creating competition among a large base of potential buyers, who in turn seek a reliable source of supply across a broad range of models…buyers attract sellers and sellers beget buyers in the feedback loop characteristic of marketplaces.

Way back in the day, Copart’s salvage auctions were conducted locally, so if you wanted to bid, you’d have to drive to the physical auction site and position yourself among a throng of other buyers before a gavel-dropping, magaphoned auctioneer (“going once, going twice…”). This meant that buyers and sellers were sourced from a tight radius (~150 miles) and that the cross-side network effects were geographically confined. But the boundaries of the auction have expanded, thanks in large part to internet enabled bidding. [Beginning in fy04 (ending July), Copart embarked on a journey to conduct all its auctions in online. These virtual auctions are split into two phases. In phase 1, which starts 3 days before the “real”, live auction, buyers submit the maximum price they are willing to pay for a vehicle and Copart’s system incrementally bids up to that price on behalf of the buyer, who receives an email if he is topped. The winning bid in phase 1 sets the starting price in phase 2, when bidders compete in a real time virtual auction environment.] Online auctions have made it far more convenient for buyers from faraway locations to participate, regardless of weather conditions, resulting in more competing offers from buyers, higher realized prices for sellers, and indirectly, more revenue for Copart, whose transaction fees are partly tied to vehicle selling prices. Today, nearly half of Copart’s auctioned vehicle volumes are sold to buyers residing outside the state where the vehicle is being auctioned [30% to out-of-state buyers inside the US; 20% to international buyers].

To be fair, KAR, which runs both physical and online auctions, disputes the notion that running purely digital auctions delivers higher selling prices, contending that online auctions cannot replicate the action and excitement being there live, in person. Yet, half of IAA’s vehicles are sold to internet buyers. While this is well below the over 80% of salvaged vehicles that receive an internet bid – implying that the topping bid more often than not comes from someone on the ground – the realized selling price would likely have been lower without incremental demand from the online channel. And virtual bidding brings other benefits besides: it takes out the operating and capital expenses required to run live auctions (though these are somewhat offset by the incremental IT expenses required to run auctions online), allows buyers to bid in multiple auctions simultaneously, and speeds up auction sales since, as described in the brackets above, some of the price discovery occurs in the preliminary phase leading up to live action.

While bidding may be just as easily done online as in person, having a physical presence still matters a lot because of transport costs. Copart relies on third party haulers to move damaged vehicle from the towing company to one of its ~200 storage facilities (or “yards”) and to then take the car from the yard to the buyer. Too few sites will result in obstructive crowding at existing locations and higher transport costs, which get passed down as higher transaction costs to buyers and sellers, making the venue operator less competitive relative to someone with more locations. A dense yard network helps in cost effectively sourcing damaged vehicles…and the more vehicles you have running through your auction, the more bidders you will attract, and the better returns you will earn on yard investments(3). It also allows Copart to strike regional and national supply agreements with insurance companies. These two instantiations of scale – the lower unit costs of operating a network of physical yards and the network effects of an auction – have reinforced one another for over 35 years, producing a system that supports 1mn vehicle searches/day and attracts 44mn bids/year to find homes (or graveyards, as the case may be) for over 1mn damaged vehicles. [Besides the fees that it takes from both the buyer and seller in each transaction, Copart also offers various ancillary services. One of these services is a salvage estimation tool called ProQuote that leverages the millions of data points it has gathered through its auctions – including make, model, year, severity of damage, season, scrap metal prices, and proximity to ports – to arrive at ever more accurate predictions of how much a damaged vehicle would get in an auction, allowing insurance companies to make wiser repair vs. salvage choices…so, data network effects are a third kind of relevant scale, albeit of much smaller importance].

Management has moreover complemented these scale advantages with operating discipline and thoughtful capital allocation. Rather than pulling an LKQ – levering its balance sheet and spraying capital at far flung markets – Copart has taken a more measured approach, investing around a quarter of its free cash flow into acquisitions over the last decade to infill existing markets and gain toeholds internationally, bolstering those new geographies with tuck-ins and organic development. Because Copart’s online auction format produces a globally distributed buyer base, when the company lands in a new market, it brings with it 750k registered members from around the globe, such that, as management put it, “when we open up in a market like the UK, we start selling motorcycles in the US.” This is different from a distributor like LKQ, whose scale economies are predominantly local. Copart’s International EBITDA margins are still below those in the US (30% vs. 39%), but the key point is that margins have trekked steadily higher, from just 23% in FY14 (when management first broke International out as a separate segment) and will continue doing so as the company densifies these markets and scale economies kick in.

Eventually, I don’t see why margins in Copart’s international markets – UK, UAE, Bahrain, Oman, Brazil, Spain, India, Ireland, and most promisingly, Germany – can’t rival those of the US. You could even make the case that the relative value proposition that Copart offers is stronger in continental Europe. The European market differs from the US in that insurers there reimburse policyholders only for the diminished value of the damaged car. It’s up to the policyholder to sell the total loss vehicle in order to recover the rest. With Copart’s model, the policyholder is reimbursed for the insured amount and can replace his damaged vehicle right away; the insurer takes on the responsibility of placing the car in auction, but, if recent auction results are any guide, realizes a higher return relative to existing remarketing methods; and the buyer, who often had to wait up to 3 weeks to know if his bid was accepted, now gets a steady, reliable flow of inventory. Everyone wins. It is then perhaps no wonder that the number of participants and unique bidders per auction are higher in Germany now than they are in North America, despite the former market’s relative immaturity.

And then there are the buybacks, which are lumpy and sporadic, as they should be. Included in Copart’s share repurchase history are two big Dutch tender offers – one in 2011, in which it retired ~14% of its share count and another in 2015, where it took out another ~11% – executed at prices that were a fraction of where they are today (~$10 in 2011 and ~$19 in 2015, split-adjusted vs. the current share price of $56), at earnings multiples significantly below current levels [management did not tender any shares in either of these auctions]. That the company hasn’t repurchased any of its shares in fy17 or year-to-date should perhaps tell you something about how appealing Copart stock is at 34x trailing earnings 🙂 A formidable scale-based competitive advantage supported by a responsible expansion plan has produced enviable returns on capital: EBITDA (no add-backs, no bullshit) has increased by $255mn over the last 7 years through fy17 on incremental gross capital of $845mn; pre-tax returns on gross capital have averaged around ~24% since fy11 with modest variation.

Finally, while stressing the importance of values and culture is eye-rollingly platitudinous, I can’t help but look back to 2005 and applaud CEO Jay Adair’s response (Jay was President of Copart at the time) to a question posed by a model-tweaking analyst who could think of nothing better than to wonder whether Hurricanes Katrina, a disaster that killed nearly 2,000 people and displaced 400,000, offered an opportunity to implement price hikes (4):

“I’m not going to have that discussion. It’s not Copart’s style. I wouldn’t do it. In a situation like this where an area has been so negatively impacted…So in this kind of situation, these major carriers are doing everything in the world they can to service their client base. I have to do everything I can to service them. I just don’t think it’s appropriate to even think of hitting them with trying to make a profit on this. I could not hit them with a price increase, I couldn’t do it.”

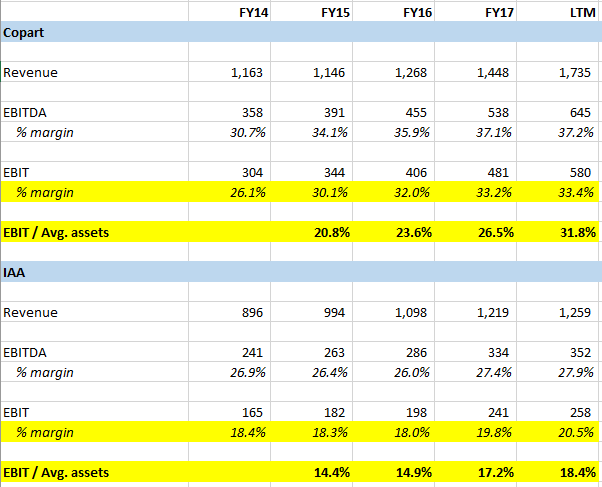

Does this answer give me the fuzzies? Naturally. I admit, I’m a sucker for this kind of stuff. But treating your customer well in hard times also happens to be sound long-term business (obviously). Before departing, I thought it might be helpful to put Copart side-by-side with IAA, as the gaping valuation disparity between Copart and KAR Auction Services – 21x EV/EBITDA for Copart vs. 11x (EV+capitalized rent)/EBITDAR for KAR, which, unlike Copart, predominantly leases rather than owns its facilities – seems interesting given IAA’s impending spin. Here is a high level view of Copart’s financials vs. IAA:

There are several important caveats. First, Copart and KAR have different fiscal year ends and I was too lazy to align their numbers. Doesn’t matter. The point is that Copart generates higher pre-tax returns than IAA on a similar revenue base [you can go back to FY16 when Copart generated the same amount of revenue as KAR does today and see that Copart’s returns were still higher].

Second, as I previously alluded to, IAA mostly leases its facilities while Copart mostly owns. KAR’s management claims that its rent expense comes to around 12% of revenue, which would account for all the margin differential, but can this be right? KAR’s total lease expense in 2017 was ~$164mn, which is indeed around 12%/13% of IAA’s revenue, but of course KAR is much bigger than IAA and includes a whole car auction segment, ADESA, which accounts for ~1/2 of KAR’s revenue and segment EBITDA. Surely some of KAR’s lease expense should be allocated to ADESA (or AFC, the company’s floorplan financing segment). But, let’s just say that rent is around 6% of IAA’s revenue. Even if we add those 6 points to IAA’s margins and generously make no reconciling adjustment to assets, IAA’s pre-tax ROA still falls short of Copart’s. Moreover, IAA’s margins don’t include any allocation of KAR’s corporate overhead, which is meaningful at around 15% of total segment-level EBITDA. Also, in the above table, I included all of KAR’s EBITDA add-backs except for stock comp and did not do likewise for Copart (in fact, refreshingly, Copart’s management doesn’t even disclose an Adjusted EBITDA figure). Finally, compared to IAA, Copart has a much higher mix of international business, which (for now) generates only ~15% ROA vs. 30%+ in the US, so comparing IAA to Copart USA only exacerbates the returns disparity. So, there does appear to be some kind of structural advantage or operational discipline in play at Copart that is lacking at IAA.

I thought maybe IAA’s cost structure included temporary cost bloat from acquired companies, but that doesn’t appear to be the case, as nearly all recent acquisitions and most of KAR’s goodwill is related to ADESA. We’ll get more clarity on what IAA looks like as an independent entity when the Form 10 comes out, but for now when I allocate corporate overhead according to revenue, I get around $300mn in EBITDA. This doesn’t deserve to trade at Copart’s 23x multiple (heck, that multiple isn’t exactly cheap for CPRT), but nor does KAR’s 10x multiple seem entirely fair.

Footnotes (1) vs. 17mn new cars that enter the fleet every year.

(2) Another subset includes cars from municipalities and charities. These cars tend to be really shitty, low value ones that nonetheless take as much time and land to sell as a higher value insurance car, so management has been pulling back on this supply channel.

(3) As you might expect, a new yard may to some degree cannibalize an existing one (and present a headwind to same store sales growth), but the trade off is well worth it if you can fill up both yards and do so with lower unit towing costs. For this reason, growth in same store yard sales, which management stopped disclosing several years ago, can be a misleading measure of financial health.

(4) In natural disasters, Copart bears upfront the outsized costs transporting a huge number of damaged cars, many of them high value, to its facilities, which temporarily depresses margins until those cars are liquidated in auction months later, whereupon margins get a lift. Net-net, hurricanes help Copart’s profits.

scuttleblurb business update (2020)

Posted By

scuttleblurb

On

In

Business updates,SAMPLE POSTS |

4 Comments

I recently did an interview with my friend @LibertyRPF[3]. It will serve as a substitute for my 2020 year-end review since it contains everything I wanted to say (and more).

With permission from @LibertyRPF, I have reproduced the interview below. You can access the original here[4].

Interview with David Kim a.k.a. Scuttleblurb

𝕊𝕡𝕖𝕔𝕚𝕒𝕝 𝔼𝕕𝕚𝕥𝕚𝕠𝕟 #𝟙

Scuttleblurb[5] is one of my favorite sources of investing/business information, and its creator, David Kim[6], is one of my favorite people I’ve met online (we haven’t met in person yet, but I hope to fix that someday… hurry up, Pfizer!).

As a writer, he’s who I want to be when I grow up.

He dives deep into companies and industries, but not in the typical way of many financial writers: He’s not trying to pitch you, he’s not starting with a conclusion in mind that he’s trying to justify by cherry picking info. He immerses himself in a business for a while and then reports what he finds about industry dynamics, management quality, unit economics, competitive advantages, how historical developments have made things the way they are today, etc.

He’s more ‘Magellan writing about his voyages’ than ‘salesman trying to get you to buy that shiny Dyson’…

His pieces often conclude on some shade of gray, without a clear call to action or price target, but I like that. It’s how the real m’f’kin’ world works.

Enough from me, let’s go to David (I’m in bold):

Hi David, thanks for doing this, I really appreciate it! I know you must have your hands full between the piles of transcripts and 10Ks and the new twins.[7]

Thanks back. I very much enjoy your eclectic newsletter. It’s one of the first things I read in the morning. I also appreciate that we’re doing this interview in writing, which I much prefer to speaking.

I don’t want to assume that everybody reading this already knows you and reads your stuff, so could you start by telling the reader who you are, what’s your background and how you got to where you are now, and what’s your day job these days?

These days I write the scuttleblurb blog[5] and manage a small fund. Prior to doing either, I was a research analyst at a L/S equity hedge fund.

The reason I started scuttleblurb is that I had just launched a fund with no prospective investors and my wife Maria and I needed a way to pay the bills. I write research notes as part of my investment process, and I put those notes online hoping people would pay to read them. Very few did.

So it was mid-2017 and we were stuck. scuttleblurb was going nowhere. My big idea for getting people to discover and then pay for my work was sending personalized emails and handwritten letters (really) to fund managers and analysts, with coupon codes and free trials and such. I spent a few thousand bucks advertising on marketfolly, which worked all right, but otherwise scuttleblurb got no traction. Maria and I just had our first baby and we were scraping by on her teaching salary plus income from a condo I was renting out as we weighed my non-existent career options. Then you somehow discovered my blog [Finding stuff is what I do! -Lib] and tweeted a link to one of my posts. Then so did @Bluegrasscap[8], @Intrinsicinv[9], and a few others.

I didn’t use Twitter at the time. I had a zombie account with like 40 followers that I barely touched. So you can imagine my surprise when the blog started to gain followers on this geeky community I had never heard of called FinTwit. I kept writing, people kept tweeting my posts, and here we are. I estimate that more than 70% of my subscribers have come from Twitter word-of-mouth. I’m so grateful for FinTwit. This community lifted me on its shoulders when things looked utterly hopeless. I honestly get a little choked up thinking about it.

What fascinates me most is your research process. You do such a good job, I’m curious what techniques I may be able to learn from you, though I suspect that there are no real tricks, just lots and lots of reading, asking questions and then tracking down answers, figuring out what is most important to focus on, etc… Can you describe what the research process is like for one of your long posts or series of posts?

Like every analyst, I read SEC filings and transcripts, Google, watch relevant YouTube videos, talk to management (usually IR), and do the same for competitors and anyone else of note in the ecosystem.

I write up every company that sparks my interest, whether I find the company an attractive investment opportunity at the time or not. I recall you mentioning that you research companies that speak to you regardless of how pricey they are and then keep those companies on a watchlist so that you’re ready to pounce when valuation approaches something reasonable. I’m the same way.