Pat Dorsey, founder of Dorsey Asset Management and formerly Director of Equity Research at Morningstar, recently pitched Workiva on the Invest Like the Best podcast (I have transcribed Dorsey’s remarks about WK in today’s Podcast Blurbs). At a high level: “And what they did is create a product that lets companies do SEC filings much […]

[WK – Workiva] From Point Solution to Platform

Posted By scuttleblurb On In [WK] Workiva | Comments Disabled[KMX – CarMax; CVNA – Carvana] Moat, Growth, and Competition

Posted By scuttleblurb On In [CVNA] Carvana,[KMX] CarMax | Comments DisabledWhen I Google “used car salesman”, here are the first images that appear. ‘nuff said. It required an electronics and appliance retailer with no car selling experience to be the change that consumers wanted to see in the car buying experience. In 1993, the now defunct Circuit City launched the first CarMax store, leveraging its […]

Quick Blurbs [Ryanair, Equinix, Interxion, Amerco]

Posted By scuttleblurb On In [EQIX] Equinix,[INXN] Interxion Holdings,[RYAAY] Ryanair,[UHAL] U-Haul,Quick Blurbs | Comments Disabled

[RYAAY – Ryanair] Anchor Post: [RYAAY – Ryanair] Low Cost Flywheel In mid-September last year, Ryanair announced that it would be cancelling 2% of its daily flights over the subsequent 6 weeks to free up aircraft and ensure punctual departure times for the other 98%. The press attributed this snafu, which inconvenienced 0.5% of Ryanair’s […]

[RHT – Red Hat] On A Bridge Between Clouds

Posted By scuttleblurb On In [RHT] Red Hat | Comments DisabledLet’s take it back to ’69. The Unix operating system was just conceived under Bell Laboratories, the vaunted research joint venture of AT&T and Western Electric. Protected by the strictures of a consent decree from 1956, which prevented its parent AT&T from commercializing technology that wasn’t related to telephony, Unix thrived as an open research […]

Blurbs [Media trends, Enterprise blockchain]

Posted By scuttleblurb On In Podcast Blurbs | Comments DisabledCode Media (2/14/2018; Analyst Michael Nathanson on where media is headed)

Michael Nathanson

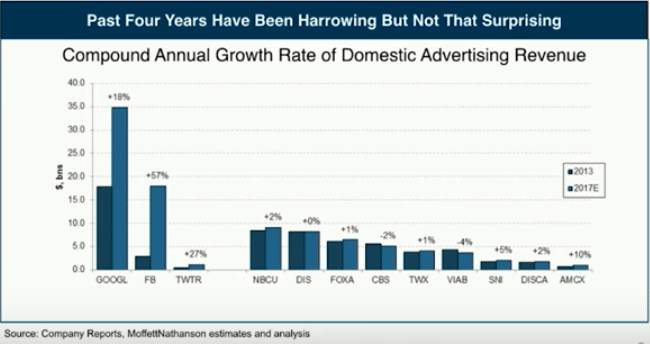

“Over the past 4 years [from 2013 to 2017], the FANG stocks have added $1.4tn of market cap. At the same time, the media industry, the content network industry, the studio industry, has lost about $40bn of market cap.

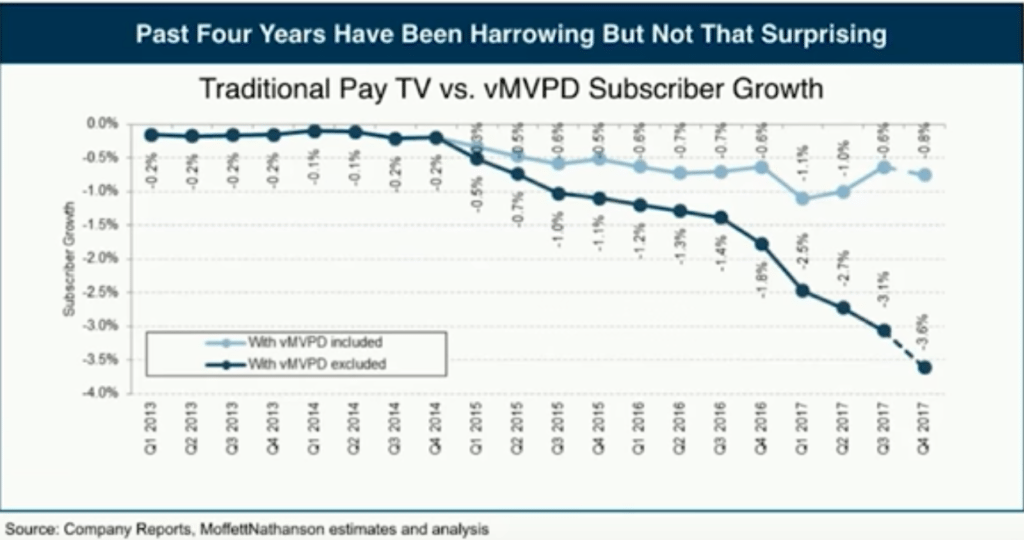

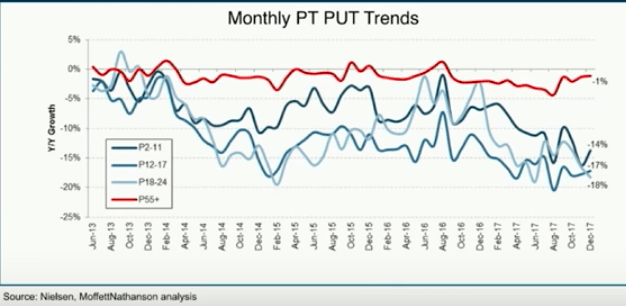

This is one of the most important slides we have at our firm that looks at the pace of cord cutting. Anytime we write a note that says ‘cord cutting’ we get like 1,000 reads…it’s everyone’s favorite topic, but it’s actually kind of complicated because there’s two kinds of cord cutting. If you look at that dark blue line that’s falling pretty rapidly, that’s the rate of cord cutting for traditional distributors. So that’s Comcast, Charter, Dish, DirectTV…so that’s declining at 4%…and we think in 2018, it gets worse…

But, there’s something called the virtual MVPDs, that’s Hulu, YouTube TV, Sling, DirectTV Now…if I added the growth we see at those places, 4mn subs by the end of 2017, we think the rate of change is +/- 1%….we see a two-speed world. If you are only tied to traditional distributors, you’re looking at -4%/-5% rate, if you’re lucky enough to be carried by those virtual new distributors, you’re looking at -1%.

Now, this is more worrying to me. Over the past 4 years, Google’s advertising growth has grown by a CAGR of about 18%. So Google was twice as big as NBC Universal’s advertising base 4 years ago, now their 4x as big as NBC’s advertising base. Facebook has grown by an annual growth rate of 60% over the last 4 years, Twitter’s grown by 27%. Facebook was at one point almost as big as Viacom’s advertising rate, now it’s 4x as big…

In a healthy economy, in a non-recessionary cycle, we’re looking at 0%-2% annual advertising growth rate for traditional media companies, and that’s truly worrying.

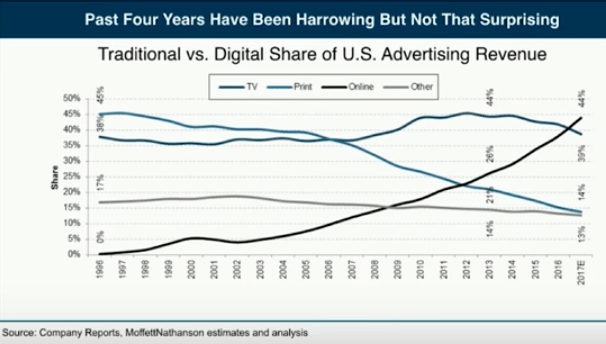

TV for the most part has held in really, really well…up until recently. 2017 was the first year in which digital advertising was a bigger segment than TV advertising.

What’s happening is that digital has done an amazing job on long tail, SMB, direct response. Facebook said a couple years ago that 25% of their advertising base [come from] their top 100 advertisers. Why does that matter? If you asked CBS or NBC, the top 100 advertisers are about 60% of their ad base. What Facebook and Google have done is they’ve monetized the long tail of non-brand direct response dollars and have done it at a great, great rate.

…why you’re getting that soft advertising story in TV is that the ratings just aren’t there.

(the growth of SVOD – Amazon, Netflix, Hulu)

So last year Netflix spent $6.3bn on their P&L buying content, mostly television. Their going to move to film, they’re making 80 films this year. When you look at their P&L this year, it’s $7bn-$8bn of content spending, on a cash basis it’s $10bn-$12bn of content spending. When you line that up with the biggest conglomerates, it’s quickly passing Time Warner, it’s bigger than Fox. They’re reaching a size of investment spending that really challenges linear scripted networks. Now when I back off sports, you could argue that their spending on content’s actually bigger than everyone else but NBCU in 2018.

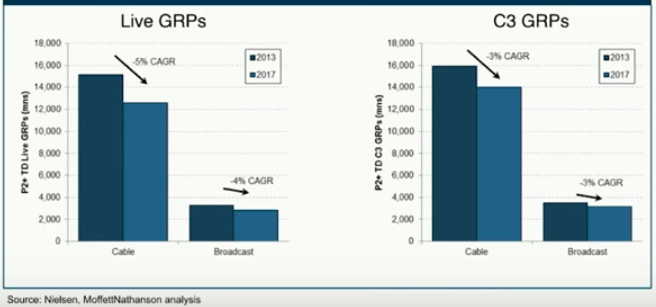

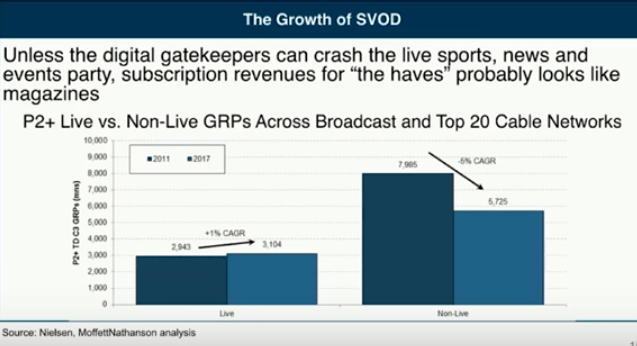

The viewing of live content over the last 7 years (below) has essentially been flat. On the flip side, the viewing of non-live content is down by a CAGR of 5% and that’s accelerating in 2017.

The only products out there that are capturing a high percentage of Americans in one fell swoop is live sports. Our view is that the only advertising play that’s going to be valuable long-term is this live reach of live sports…having this type of unduplicated live reach is why the dollars have not come out of TV yet.

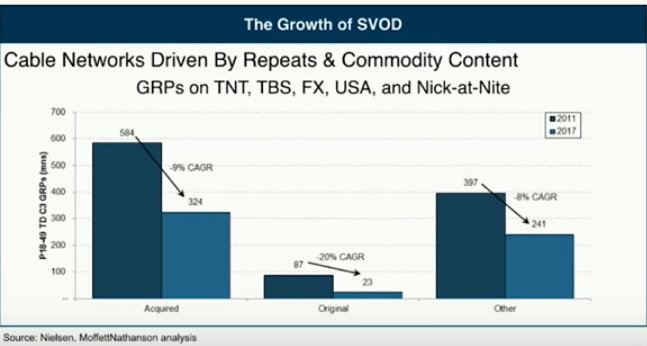

Cable networks driven by repeats and commodity content are in trouble (TNT, TBS, FX, USA, and Nick-at-Nite)…at some point networks that are built on repeat content are going to see big erosion and in fact, that’s what’s happened.

(virtual MVPDs and escalation of affiliate fees)

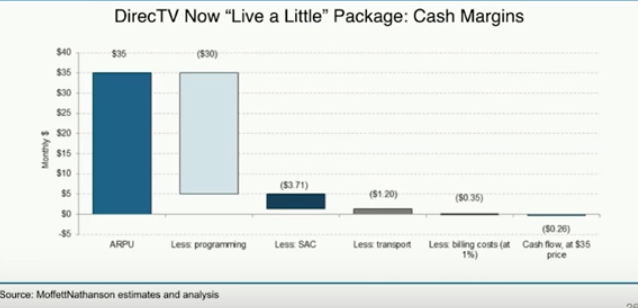

The only problem we see is this…when we do the math on skinny bundles – sports and news stripped down to $35-$40 – our math says there’s no profit there. So you’re getting this profitless growth on the distribution side…

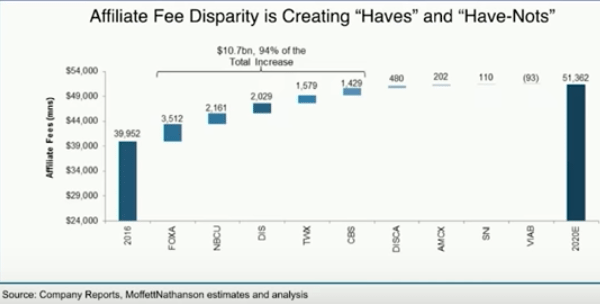

…now making it worse in the future is that the networks they’ve chosen to be the bedrock of those virtual services – Fox, NBC, Disney, Time Warner, CBS – is pretty much where all the growth in that affiliate fee bucket is…the growth rate for their affiliate fees is 9% in aggregate. If you’re a virtual network, you have a $35 price point, but your cost of goods sold is going to be inflating at a very, very high rate, so at some point you have to decide whether you raise your pricing, which could limit your growth or you absorb it as a loss leading product.

PUT – People Using TV. “Did you use TV today”. If you’ve got a network built on 55+, you’re not seeing the same level of decay as these younger networks.

(Film)

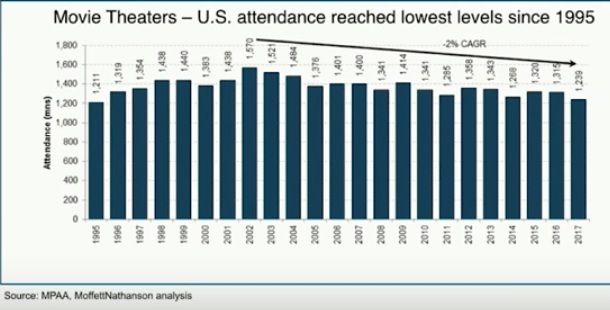

Not a surprise that the physical bit of video has fallen from $16bn to $6bn…but what I’m here to tell you is the growth of the digital format – electronic sell-through, video on demand – is starting to slow. We once thought that could add back the decline of physical. It’s not happening. The bulk of [the physical DVDs] that are bought are from Target, Wal Mart, Best Buy, and it’s just a matter of years before those companies start downsizing their carrying of physical product. So we’re very very worried about the back-end monetization of the film business. And that’s going to lead to more premium VoD….2017 was the worst box office year we’ve seen since 1995 and as Netflix spends more money to make better and better movies, as premium VoD windows start opening up, we see pressure on the theatrical side of the business.

In the short run what you’re seeing is consolidation at a rapid pace. Fox-Disney happened out of nowhere. Time Warner-ATT out of nowhere. Scripps-Discovery, quickly…people are trying to find cost synergies, scale against distributors, trying to find some ways to the consumer with enough library of content.

Blockchain Innovation (10/20/17; How RedHat is Quietly Transforming Enterprise Blockchain with Rich Feldmann)

Rich Feldmann

“So, first on Red Hat. Red Hat is the worldwide leader in open source technology for the enterprise and a lot of the early block chain start-ups were…forming their own open source community projects to develop a distributed ledger either for the cryptocurrency side or for use in the enterprise. So, we got a lot of invitations to come and have conversations with ‘how can Red Hat help me form a sustaining open source community effort and then once I do, can you help me with governance and licensing’. These are all areas that Red Hat was founded on, so it was a natural. So, for about 6 to 8 quarters, those were the nature of the conversations that we had.

Roll forward to today, we have an in-market offering that we call Blockchain-as-a-service that builds on some of the other capabilities that are already in market…blockchain has board level attention at Red Hat and we are putting resources behind it.

What Red Hat’s interest in the blockchain space is distributed ledger use cases for the enterprise. We’re not investing a whole lot of time and energy in cryptocurrency side…so you made mention of the consortiums, Hyperledger (150+ members) and Ethereum Alliance (over 200 members), there’s a few others like Dockchain in the healthcare space, there’s similar ones that are being spun up in Europe and Asia, and I would say virtually all have come to Red Hat and said…’would you be interested in running a support model around my distributed ledger’…while Red Hat sees this as a strategically important initiative, at the current time we don’t have plans to release a Red Hat Enterprise blockchain.

What…are the challenges to getting blockchain or distributed ledgers more broadly accepted, the consortium efforts are a wonderful one and we are members of the Hyperledger consortium, we’re looking at the Ethereum Alliance, but in order [to get] broad based acceptance, eventually we believe that somebody’s going to need to step up and provide a governance model and support model. That’s not Red Hat today. What we do believe is that any distributed ledger…all need to run on a supported enterprise infrastructure, so that’s a supported operating system, being deployed in a cloud or hybrid environment….so what we announced about 6 months ago was a hybrid cloud offering called blockchain-as-a-service with our good partner BlockApps.

If Red Hat’s strategy is not to release Red Hat Enterprise blockchain, what is Red Hat’s strategy? It’s really about providing an enterprise ready platform for you to run your distributed ledger application on…So what we announced, which is something that Microsoft had previously announced with BlockApps, the worldwide leader of what’s known as Blockchain as a service, it’s a way to quickstart a PoC, in a 6 to 12 week project you can spin up your use case, develop it on an application, develop a set of APIs, and develop a small, working application. What Red Hat has done is taken from just a PoC capability to an enterprise ready capability by integrating it with our PaaS offering, which is called OpenShift, so that when clients get ready to go from PoC to production systems, they’re already deployed on those enterprise ready systems […]

Probably smart contracts are the ‘X’ factor, the killer app in distributed ledgers for the enterprise, and smart contracts are now being integrated, they’re a core part of the Ethereum stack and they’re now being integrated into Hyperledger as well, and some of the other distributed ledgers for the enterprise. From an infrastructure perspective, that’s the killer app. What is the killer app from a use case perspective, I don’t think there’s one…

Where we find success is deploying distributed ledger technology behind the firewall that doesn’t require 500 parties to agree on a technology standard…let’s do something like think about a large financial institution that does a general ledger consolidation, and all the steps in the process that occur along the line, whether you’re a subsidiary or a branch of a bank, you’ve got to consolidate your financial statements over say 500 or 5,000 different entities…Now today, with the OCC and everyone that’s looking over your shoulder, you’ve got to report who made changes to that data all along the line. So, that kind of process, completely behind the firewall, under the control of financial institution, is something that lends itself very well to a blockchain or distributed ledger system […]

I’m talking to many large and small systems integrators, large and small ISVs that want to develop applications that will sit on top of a distributed ledger technology. My view is that in the fullness of time, what is a distributed ledger? It’s a database, it’s a data store where some component of the data, ownership, rights pass from one node to another.”

[CMPR – Cimpress NV] Scale Economies and Hard Realities, Pt. 3

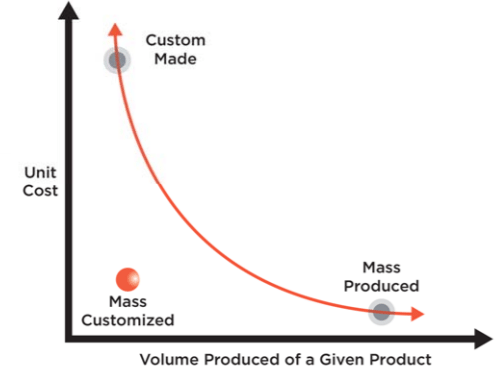

Posted By scuttleblurb On In SAMPLE POSTS,[CMPR] Cimpress NV | Comments DisabledCimpress is a fine business that has been in search of strategic direction for the last 6-7 years, groping for the right balance between value-added customization and low-cost production. These two sources of differentiation are often at odds because the scale economies required to claim a cost advantage depend on running lots and lots of volume across significant fixed costs, a process that is best suited for homogeneous products that share a common manufacturing base and process. You can imagine casting a single widget SKU over and over again. There are no incremental set-up costs from line changeovers. The assembly line just keeps humming as long as it can, spewing a stream of identical widgets onto a continuously flowing conveyor belt, the upfront cost of heavy equipment diffused over more and more manufactured units. At the other extreme, a stylist’s average cost per haircut stays roughly the same, whether he does 20 haircuts a day or 30. Of course, most jobs fall somewhere between these two poles. Cimpress (originally known as VistaPrint), which makes a variety of customized physical marketing materials – business cards, signage, apparel, gifts – for mostly micro business with fewer than 10 employees, claims that it can capture the benefits of both differentiation and low-cost (“mass customization”):

Source: Cimpress Business cards are a perfect use case for mass customization because from the customer’s perspective, a set of business cards, tatooed with a unique logo and font, is unique; but from Vistapint’s perspective, the core manufacturing process and materials required to produce them is essentially the same across all customers. And after its founding in 1995, Cimpress spent the first dozen or so years of its existence focused on paper-based products…business cards (where it remains dominant) postcards, brochures, presentation folders, data sheets, and the like, predominantly in North America. Volume brought scale, scale compressed average unit costs, profits from cost advantages funded VistaPrint’s strategy, which was to litter inboxes with cheesy marketing campaigns offering something like business cards or return address labels for free and drawing customers to the website, where they could then be cross-sold other products and bamboozled with exorbitant shipping costs on the check out page (after they’d already spent the time designing their items and were psychologically committed to the purchase).

Today, Vistaprint prints 6bn business cards a year, one for nearly every person on the planet. It can produce a pack of business cards in less than 10 seconds and fulfill the order in less than 2 minutes. No one else comes anywhere close to extracting the scale economies enabled by that kind of volume. Although paper-based marketing, including business cards, is in decline, the company’s Vistaprint segment is still showing high-single/low double digit organic growth as it continues to steal share from the tens of thousands of small manual operations that still account for most of the putative $30bn market opportunity [per management; computed as 60mn small businesses with fewer than 10 employees across North America, Europe, Australia, and New Zealand multiplied by $500 in annual marketing spend], leaving Cimpress, with just $2.4bn of total revenue, plenty of runway ahead.

But sometime in 2011, with revenue growth decelerating, management embarked on an aggressive M&A strategy. Since fy11 (fiscal year ends June), on top of ~$590mn in capex and capitalized software development, management has spent around $900mn buying 15 companies – ranging from a DIY website building (Webs.com) to a host of European print and design companies catering to graphics professionals (consolidated as the “Upload and Print” operating segment) – tangentially related to the core Vistaprint business by dint of their marketing orientation but otherwise diffuse in terms of product SKUs and addressable markets. And for this ~$1.5bn investment, Cimpress’ EBITDA (after stock comp) has grown by just $106mn, a 7% pre-tax return compared to management’s 10% hurdle rate for predictable organic investments in developed countries and 25% bogey for riskier investments in emerging markets. Now, one might argue that the cost structure is larded with growth opex that will eventually subside. But, we’ve also heard this line from management before, as it has fumbled its way from one strategy to the next.

The first course correction came in fy11, when management recognized that deep discounting, aggressive cross-selling, and cheap checkout tricks were compromising repeat purchase rates, diluting lifetime customer values, and attracting low quality customers looking for an easy deal…basically, a leaky bucket that required constant infusions of customer acquisition spend that management did not think was sustainable. And so, Cimpress made significant investments in packaging, product quality, and user experience on the site. It dramatically reduced what it charged customers for shipping, which at the time apparently made up a “very material portion of revenues”, and introduced less jarring discounts on more transparent list prices. These actions were meant to chase away the cheapskates who only cared about price, leaving the company with a more loyal and satisfied core more apt to repeat purchase. Didn’t really work. Despite some operational improvements – quality complaints, production throughput times, late deliveries all improved – organic revenue growth slowed from 22% in fy11 to 20%, then 12%, then 4% over the subsequent 3 years. Gross margins declined a bit, EBITDA margins declined a lot. Buyer repeat rates actually declined from 30% to 26%. Management’s initial expectations for $5 EPS (representing 20% annual growth over 5 years) and $2bn in revenue by fy16, would clearly not come to pass. That brings us to Act II.

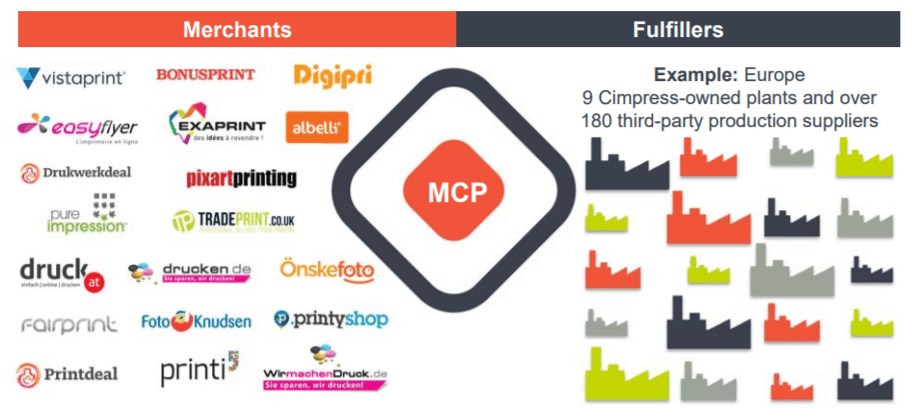

Sometime in fy13, the company embarked on an effort to disaggregate its tech platform into a set of software microservices appropriately named the Mass Customization Platform (MCP) as part of a broader effort to centralize all sorts kinds of functions – product management, order routing, fulfillment, commodities procurement – across its 20+ brands:

“…our vision for MCP is to be a constellation of modular, reusable and independently functioning software components and related services which is analogous to a well-organized set of interchangeable Lego blocks. This platform will sort millions of heterogeneous incoming orders into homogeneous specialized production streams which, thanks to the automated workflow and the regular repetitive production steps we can enable, will embody the principles of mass customization. Yet, the overall platform needs to remain reconfigurable and modular to ensure the relevance to a wide variety of applications….what we are doing is we are frankly trying to break the businesses which we bought, not just Vistaprint, but each of the individual companies we bought, into the component parts of the merchant, the customer-facing business unit with the brand and the fulfiller, and then to reconfigure all the IT systems so that those can…act as a routing layer between those.” – Robert Keane, Chairman and CEO (Cimpress Investor Day, 8/10/2016)

Management’s big idea was to create a matchmaking service that would pair the unique, specialized, and often small-sized manufacturing and fulfillment needs of its sprawling internal businesses (“merchants”) – some selling business cards to micro-businesses in the US, others serving graphic design pros in Europe who in turn serve micro-businesses – to its most cost effective option among a network of in-house and third party production plants and shipping/logistics providers. As the number of fulfillment partners joining the platform expanded, so too would the number of SKUs the company could offer, which in turn would attract still more fulfillment partners seeking production volumes to run through their specialized plants. Two-sided engagement would lift volumes flowing through Cimpress’ network, bringing procurement leverage to bear against service providers, equipment vendors, and commodities suppliers.

But just 5 months after promulgating this lofty vision during 2016 Investor Day, management conceded that this centralized model, which was intended to increase speed to market and production flexibility, had instead bogged down the company with complexity and bureaucracy. It announced plans to retreat back to a more decentralized organizational setup wherein production, fulfillment, and product management would be siloed once again by brand, though non-core corporate functions (finance, legal, major capital allocation), procurement, and the modularized technology platform would remain as shared services across banners. Now the thinking is that decentralization will unleash “entrepreneurial energy”, ensure accountability for results, and improve customer satisfaction. And that’s where we are today. Mistakes have been made, that much is clear. The company’s acquisition of DIY website builder Webs.com, one of it’s largest, seems particularly ill-conceived. Website building is a high gross margin business that pure-plays struggle to monetize because lofty customer acquisition costs eat up all the profits. But Cimpress believed it could do away with much of these advertising costs by cross-selling web services into its existing customer base, because in management’s own words “…a website is the same as a brochure, but it’s a digital version of that.”

But of course, a website is more than just another marketing tool that you toss into the shopping cart as you purchase signs and business cards; it’s increasingly the entire digital storefront and a critical system of record. The companies that do well in website building either own critical on-ramps like domain registration (Godaddy) or offer kick-ass functionality further up the stack, with sophisticated, friction alleviating technology and/or 3rd-party app integrations (Wix and Shopify). And there’s a reason why website builders don’t bundle business cards…not only are these offerings not a natural point of integration, but doing well in either area involves entirely different processes. I’m not rehashing Cimpress’ somewhat ignomonious capital allocation and strategy choices with snark (or I at least hope it doesn’t come across that way). On the contrary, I think it’s admirable that this management team at least attempts to take an earnest look at its shortcomings, fesses up to them, and experiments with new ideas. I bring this up just to frame the difficulty of growing through a continuous product introductions and simultaneously extracting scale economies.

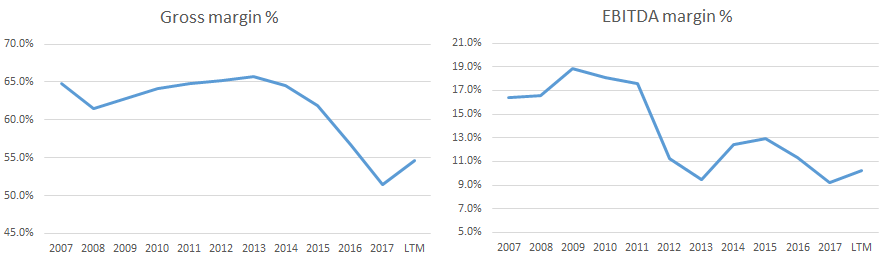

At one extreme, the company could have just stuck to business cards and closely related paper-based products, gaining a little more production leverage every year and steadily improving its gross margins…but growth would have inevitably slowed and then reversed as the market for business cards is in decline and Cimpress’ business card revenue growth has decelerated significantly over the last decade. But then, proliferating product categories to boost volume growth makes scale economies harder to come by. Through the acquisitions that now comprise its Upload and Print segment, Cimpress multiplied its SKU count by 300x, and the number continues to grow at a rapid pace. The scale benefits attending homogeneous manufacturing and fulfillment processes attenuate as you start offering different substrates and formats, and especially as you expand into banners, apparel, pens, magnets, and other trinkets made of entirely different materials, manufactured through a different process with different equipment in different countries. I think the company recognized this long ago, hence its emphasis on higher quality products to customers with better lifetime values; but I also think it’s fair to say that management underestimated how difficult it would be to reap the benefits of mass production over so many diverse product categories. Check out their margins over time…

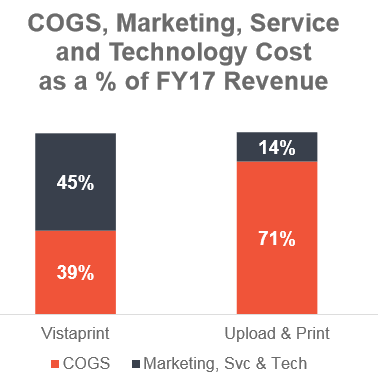

The nosedive in gross margins can be mostly explained by investment in design services and a mix shift towards Upload and Print, which has been growing faster than Vistaprint and is more dependent on outsourced production. But, this segment also has lower sales and marketing costs per order than Vistaprint and all else equal, the two segments should have comparable EBITDA margins…but those have declined considerably as well over the last decade, even as Cimpress has shown some sales & marketing and G&A leverage over time. I think this can be at least partly explained by shipping, which runs through gross profit. The company is loath and perhaps embarrassed(?) to reveal how much money it was making on shipping, but assuming average shipping price charged to the customer of $10 and an average order value (back when management still revealed this figure) of around $35, it was clearly significant.

I don’t imagine its own shipping costs have changed by nearly as much, and so providing relief to its own customers likely translates to a mostly direct gross profit hit. Also, losses from the “all other business units” segment, which houses speculative investments, emerging markets, partnerships, continue to grow, from -$9mn in fy16 to -$36mn LTM. Finally, digital products and services (Webs.com I assume?) has witnessed significant revenue declines. Except for maybe losses in emerging markets, which are still small and sub-scale, none of the above mentioned causes of margin compression will reverse, so the high-teens EBITDA margins of the mid/late 2000s are likely a thing of the past. Management does not deny this and, in the face of persistently declining margins, now directs investors to think instead about dollar profits, retention rates, and lifetime customer values, tacitly acknowledging that ever more of the scale benefits are shifting from production leverage to value-add per customer. Cimpress’ last 10-K (year ending June 2017) reveals 17mn customers served by Vistaprint, which means the number of unique customers hasn’t budged since fy14. However, Vistaprint’s revenue has grown by over 25% over that time, implying that revenue per customer has gone from $65 to around $80. Management does not break out gross profit or opex by business segment in its financials, but we do have this useful exhibit from the last Investor Day:

The buyer repeat rate, at between 30%-35%, is so low that one wonders whether the lifetime value of customers is really the right metric for management to focus on, but let’s just go with it. So if revenue per Vistaprint customer is $80, then it looks like gross profit per sub is close to $50. Assuming a 10% discount rate and that 35% of buyers make repeat purchases [I’m assuming it’s higher than the 31% rate the company disclosed for fy17] implies an LTV per customer of $73. Before the company went on its acquisition spree and it was just basically Vistaprint, the cost of customer acquisition was around $24, suggesting an LTV:CAC of ~3x. Once you factor in higher recurring costs of supporting today’s relatively higher quality customers, the ratio is probably closer to 2.5x(?), right at the cusp of acceptability. To put that in perspective, Trupanion is at ~4.5x, Godaddy is over 5x. [Founder and CEO Robert Keane writes the kind of letters that value investors just eat up, chock full as they are of Buffett-esque straight talk and verbiage. But I’ve actually found disclosure to be frustratingly inconsistent. For instance, up until fy14, the company provided metrics on average order values (AOV), order volumes, repeat customers, bookings per repeat customer, and other good stuff. They stopped regularly disclosing most of this in fy15, defending the move by maintaining that a metric like $AOV doesn’t provide much insight because there are so many businesses besides Vistaprint. Like, huh? Vistaprint still represents 65% of revenue, 80% of segment profits, and the majority of organic investments. And even if that weren’t the case, why stop disclosing the very data required to estimate lifetime value at precisely the time in the company’s history when it is explicitly targeting this metric?]

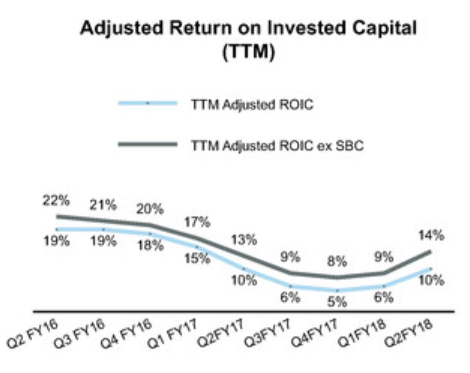

As mentioned earlier, Cimpress’ acquisitions and organic investments over the last 5-6 years appear to have impaired value, with returns on incremental capital falling short of capital costs, and over time, we see that the company’s returns have deteriorated rather markedly in even the last few years. And they are way below the the 30%+ returns the company was realizing before its spree. Meanwhile, over the last 5 years, organic growth has been cut nearly in half, from 20% in fy12 to ~10%/11% LTM.

[“adjusted” because the numerator excludes restructuring charges; acquisition related earn-outs, amortization, and depreciation; and impairments] But that hasn’t stopped valuation multiples from doubling over that period.

But perhaps I am throwing excessive shade. While I think Cimpress is a worse company than it was 5-10 years ago and its mass customization platform is maybe not quite what was promised, it’s still hard to imagine a competitor rivaling Cimpress’ scale advantages, and I think the company will continue taking enough share to deliver high-single/low double-digit organic revenue growth for the foreseeable future. Founder and CEO Robert Keane, who owns 10.5% of the company and owns the same number of shares as he did 7 years ago, has significant skin in the game. The company has retired nearly 30% of its shares over the last 7.5 years in the low-$40s. Using the high-end of management’s estimate of investments required to grow free cash flow by at least inflation, LTM mFCFE per share is around $8/share [1], so the stock trades at ~20x, which doesn’t seem too demanding a valuation given the company’s competitive positioning and growth opportunities. Cimpress recently reported an outstanding quarter across all reported segments, suggesting budding traction with its decentralization initiative. But I frankly have no idea if this inflection is sustainable.

Given the pronounced deceleration in core legacy business cards, where the engine of mass customization was applied beautifully for the first 15 years of the company’s life, diversifying into far flung SKUs may have seemed sensible at the time….they were squeezing less juice from scale economies but could compensate for that by moving upmarket, offering a value-added bundle proposition with a heavier service component. But in retrospect, shareholders would probably have been better off if management just maximized the hell out of lower organic growth and plowed excess capital – capital that could not be reinvested into core Vistaprint – into share buybacks rather than acquisitions. [1] Estimating relief under the new US tax law is tricky because the company already reallocates income across a sprawl of geographies to minimize its tax payments. Cimpress derives just 40% of its revenue from the US and over the past year paid just $40mn in cash taxes on $180mn in pre-tax cash profit, so I’m not so sure the new rule will meaningfully benefit the company.

[RP] RealPage

Posted By scuttleblurb On In [RP] RealPage | Comments DisabledIn 1998 RealPage Communications, an internet hosting service for the commercial and residential real estate industry, merged with Rent Roll, a provider of property management software, giving birth a few years later to the company’s flagship property management SaaS, OneSite. At a time when property managers were still awkwardly fusing disparate general purpose on-premise systems […]

[IDXX – IDEXX Labs] Priced to Win

Posted By scuttleblurb On In [IDXX] IDEXX Labs | Comments DisabledPeople love their pets. That’s obvious not merely in our impulse to anthropomorphize them but to increasingly care for them the same way we do human members of our families. American pet owners used to really only took their pets to clinics to treat obvious physical symptoms, but they’ve increasingly been hitting up the vet […]