Capital Allocators with Ted Seides, Ep. #32 (Paul Johnson and Paul Sonkin – The Perfect Investment)

“Fama says that an efficient stock is one where the market incorporates all available information. So, there are 3 major parts of that: the information has to be properly disseminated and the second is that it has to be processed without any systematic bias, and then the third is that it has to be incorporated into the stock price. [Processed without systematic bias] depends on the diversity of the shareholder base and then the independence of the shareholder base. So, if either of those two break down, then you have a systematic bias. And that’s two of the three areas where behavioral bias really enters into the equation. And then it has to be expressed in the stock price. And things that could prevent it from getting to the stock price, it could be that people are unwilling or unable to trade. So in terms of unwilling, it’s when you get a case like 2009 where people are afraid to put capital to work. They know it’s cheap but they are afraid of putting capital at risk. Or they’re unable to trade. And that could be because the stock is a market cap and it’s too illiquid, so if you don’t have a sufficient number of people that can express their opinions, you end up with a mispriced stock price.

On the [Processing piece], lack of diversity is when everyone’s thinking the same way – that’s a bubble or a panic. Independence is something different, where people are diverse but when they go to express their opinion, then they’re collectively influenced by some external…so, a good example would be Herbalife stock, when Bill Ackman did his presentation. You might have had diversity in the shareholder base in that people had a lot of different estimates in terms of what it was worth and then what they did was they set aside their estimate and adopted Ackman’s view and sold the stock. So, that’s really the lack of independence where they adopt someone else’s view. Diversity is kind of different because that’s when everyone is thinking the same way independently. So, one example we’ve been toying around with is imagine if you asked 1,000 portfolio managers what Amazon was worth. You might get a number like $600. Now, if you said to them, are you willing to put money on that – buy the stock or short the stock – there are a lot of people that aren’t willing to short the stock because of the risk, so the only people in the market are the ones that think it’s worth north of $1,000. So, you don’t really have diversity in the shareholder base because there’s a whole segment that’s not participating…

Just because a stock lacks diversity or independence, that doesn’t mean the price is wrong. So, we’re not saying that Amazon is mispriced, we’re just saying that the crowd is not very diverse. So, if an event happens that challenges the crowd’s view, this stock’s going to move hard and violently and we see that with growth stocks over time, if the growth breaks, there’s nobody there on the other side balancing it. You don’t have a diverse group. All of a sudden, everyone that owns it owns it for the growth, growth is no longer there. They exit. The next trade has to be somebody who sees value but at a much lower price.

10 Year Futures (vs. What’s Happening Now)

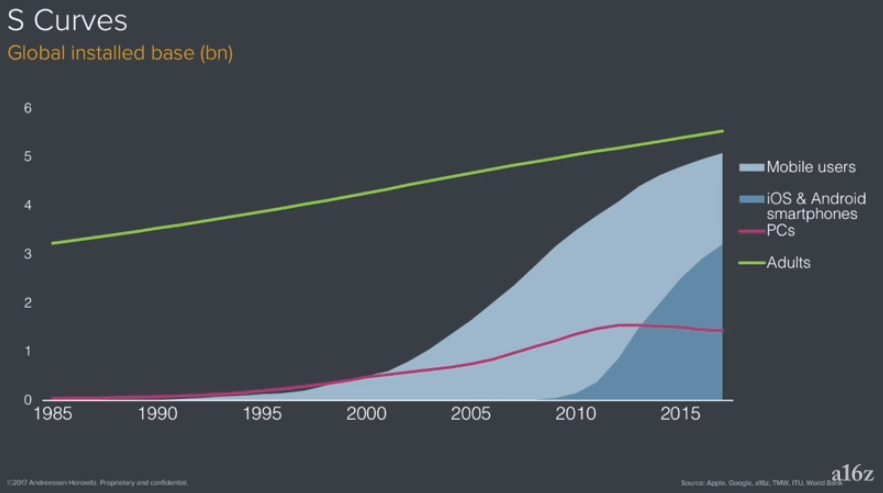

Benedict Evans:

“What you see with each of these curves is that they start slowly and then they reach a point when they explode and then they kind of slow down again and get a bit boring…as we get to the stable and mature part of each of these curves, we start talking about what we can build on top of them. So, talking about mobile now feels like talking about mobile in 2004, 2005, 2006. On PCs, we talked about search and social, on smartphones, we talk about ride sharing, Instagram, Instacart and deliveries. We talk about what we can build on the platform rather than the platform itself…

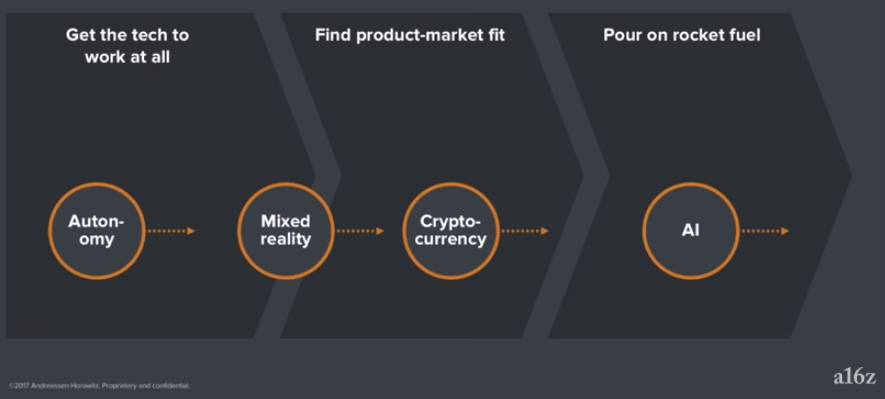

You kind of have three phases at the beginning of the S-Curve. You have the period where the tech doesn’t quite work at all but you think it will, then you’ve got the period where you’ve got it sort of working but you don’t have product-market fit, and then there’s the point when it explodes and you’re pouring on rocket fuel. So, we have 4 S-Curves today that are at various stages of that process…

AI: when I talk about enabling layers, I think a great analogy here is relational databases. Relational databases emerge in the late ’70s and early ‘80s, and they allow you to say ‘show me all customers in this zip code’ for the first time. Before that if you wanted to ask a question like that that was an engineering project and somebody would have to go spend a couple of weeks building it. Databases were not built with that kind of structure in mind.

And the fact that relational databases meant you could ask those questions meant that databases went from being record keeping systems to just replace paper filing cabinets to being business intelligence systems, and that enable all sorts of things. Most of all, of course, it enabled billion-dollar companies. So, we got Oracle. Then, we got SAP and SAP is not just a database, it’s an ERP system and SAP means that you could move your supply chain to China. And so, SAP changes what companies are and how you can run a company. And then by the 1990s, pretty much every enterprise software company is a relational database, but nobody looks at CRM or Success Factors and says ‘well, that won’t work because Oracle has all the database’. Rather, what happened is it’s an enabling layer that enables new things but enables them in all sorts of new companies…

That is the best way to think about machine learning…so, you can take a dataset and machine learning will let you find patterns. And those patterns could be all sorts of things. They can be cats and dogs, they can be different delivery routes, they can be fraudulent behavior on the network.

Finding patterns becomes a generalizable solution. So, ‘is there a cat in this picture’ becomes the same kind of question as ‘which customers are going to churn’ or ‘is that car going to let me merge’…that’s to say, you find lots of different questions and you also find things in the data that you didn’t know were there, the unknown unknowns…

When you start looking at a new enabling technology, the first demos that you see and the first things that are built with it are just expressing the capability but they’re not everything that you’re going to do with it…and so the same thing with machine learning now…what is it conceptually that we can automate with machine learning?…so, you have this pile of data where you know there’s patterns but you can’t sort it with a computer and you don’t have 100k interns to go through that data. Well, now you do. This is what automation always does, it gives you a massive multiplier effect. A steam engine doesn’t replace one horse, it gives you 1,000 horses. Machine learning doesn’t replace one person, it gives you the capability to do what you could have only done if you had 1,000 of those people before.

Cyptos: there’s sort of two ways to be at the beginning of the S-Curve. The first of those is that the technology doesn’t quite work yet, it’s not quite a product yet. And that’s where autonomy is now, it’s also where mixed reality is now, it’s also where smartphones were in 2006. The other way…is that the technology works, but we’re not quite sure what we should do with it. And that’s where HTML and the web were in 1994, it all worked fine…but it wasn’t quite clear what you could do with it and how useful it would be and what it would mean if everyone on earth was using it. And that’s pretty much where cryptocurrencies are today…

What is it that crypto automates? Well, it automates…trust. And so if you think about the process of this, money has been in the cloud in some way for centuries. So, we moved gold into banks and banks in the 18th century were basically the cloud except they had no backup, and then we moved the gold onto paper and we moved the records into punchcards and into mainframes and into databases. We changed it into a record but then we didn’t do anything with the record.

And so as we look at cryptocurrency, we start thinking about two parts of this. One of them is a distributed part, you have a database where you can put things without needing a central authority. But the other thing is that database can do stuff and the records in that database can do things and mean things that were not really possible with any previous way of storing this information.”

The Knowledge Project (2/27/17; Naval Ravikant on Reading, Happiness, Systems for Decision Making, Habits, Radical Honesty)

“I would say that the biggest such change was when I was younger, I really, really valued freedom. Freedom was one of my core, core values. Ironically, it still is. It’s probably one of my top three values, but it’s a different definition of freedom. My old definition was freedom to, freedom to do anything I want. Freedom to do whatever I feel like, whenever I feel like. Now I would say that the freedom that I’m looking for is internal freedom. It’s freedom from. It’s freedom from reaction. It’s freedom from feeling angry. It’s freedom from being sad. It’s freedom from being forced to do things. I’m looking for freedom from internally and externally, whereas before I was looking for freedom to […]

Another example of a foundational value is I don’t believe in any short-term thinking or dealing. Let’s say I’m doing business with somebody and they think in a short-term manner with somebody else, then I don’t want to do business with that person anymore. I think all the benefits in life come from compound interest, whether in money or in relationships or love or health or activities or habits. I only want to be around people that I know I’m going to be around with for the rest of my life. I only want to work on things that I know have long-term payout.

Another one is I only believe in peer relationships. I don’t believe in hierarchical relationships. I don’t want to be above anybody and I don’t want to be below anybody. If I can’t treat someone like a peer and if they can’t treat me like peer, then I just don’t want to interact with that human […]

All the real score cards are internal. The sad thing is we sit there, like jealousy. Jealousy was a very hard emotion for me to overcome. When I was young, I had a lot of jealousy in me. By and by, I learned to get rid of it. It still crops up every now and then. It’s such a poisonous emotion because, at the end of the day, you’re no better off, you’re unhappier, and the person you’re jealous of is still successful or good-looking or whatever they are. The real breakthrough for me, was when I realized, at a personal, fundamental level, the problem with these kinds of podcasts is I can give glib answers all day long, but you have to discover your own personal answer. Your personal answer is going to be different than mine. It’ll speak to you.

The one that I discovered that spoke to me was the day I realized that all these people that I was jealous of, I couldn’t just cherry-pick and choose little aspects of their life. I couldn’t say I want his body, I want her money, I want his personality. You have to be that person. Do you want to actually be that person with all of their reactions, their desires, their family, their happiness level, their outlook on life, their self-image? If you’re not willing to do a wholesale, 24/7, 100% swap with who that person is, then there is no point in being jealous.”

Code Media (2/14/2018; Analyst Michael Nathanson on where media is headed)

Michael Nathanson

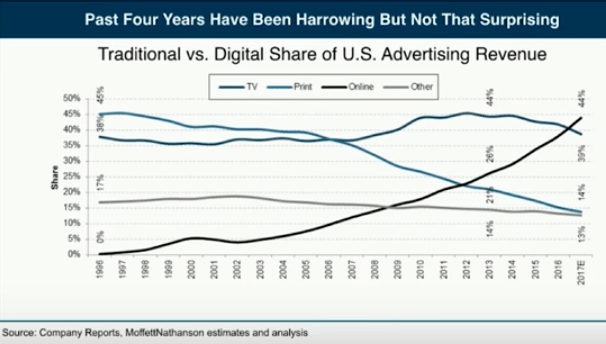

“Over the past 4 years [from 2013 to 2017], the FANG stocks have added $1.4tn of market cap. At the same time, the media industry, the content network industry, the studio industry, has lost about $40bn of market cap.

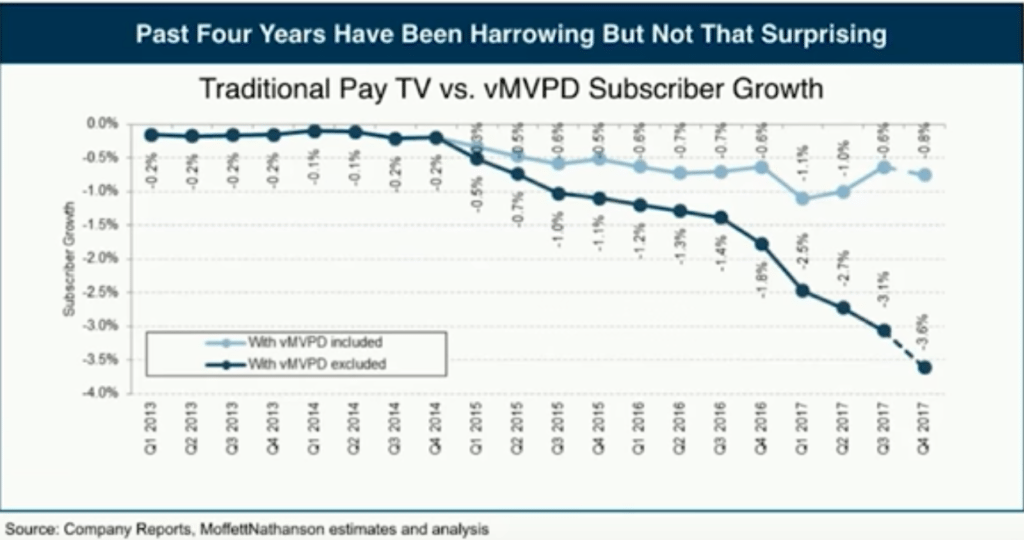

This is one of the most important slides we have at our firm that looks at the pace of cord cutting. Anytime we write a note that says ‘cord cutting’ we get like 1,000 reads…it’s everyone’s favorite topic, but it’s actually kind of complicated because there’s two kinds of cord cutting. If you look at that dark blue line that’s falling pretty rapidly, that’s the rate of cord cutting for traditional distributors. So that’s Comcast, Charter, Dish, DirectTV…so that’s declining at 4%…and we think in 2018, it gets worse…

But, there’s something called the virtual MVPDs, that’s Hulu, YouTube TV, Sling, DirectTV Now…if I added the growth we see at those places, 4mn subs by the end of 2017, we think the rate of change is +/- 1%….we see a two-speed world. If you are only tied to traditional distributors, you’re looking at -4%/-5% rate, if you’re lucky enough to be carried by those virtual new distributors, you’re looking at -1%.

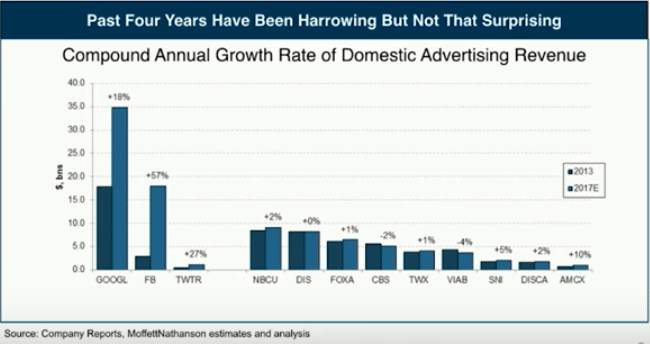

Now, this is more worrying to me. Over the past 4 years, Google’s advertising growth has grown by a CAGR of about 18%. So Google was twice as big as NBC Universal’s advertising base 4 years ago, now their 4x as big as NBC’s advertising base. Facebook has grown by an annual growth rate of 60% over the last 4 years, Twitter’s grown by 27%. Facebook was at one point almost as big as Viacom’s advertising rate, now it’s 4x as big…

In a healthy economy, in a non-recessionary cycle, we’re looking at 0%-2% annual advertising growth rate for traditional media companies, and that’s truly worrying.

TV for the most part has held in really, really well…up until recently. 2017 was the first year in which digital advertising was a bigger segment than TV advertising.

What’s happening is that digital has done an amazing job on long tail, SMB, direct response. Facebook said a couple years ago that 25% of their advertising base [come from] their top 100 advertisers. Why does that matter? If you asked CBS or NBC, the top 100 advertisers are about 60% of their ad base. What Facebook and Google have done is they’ve monetized the long tail of non-brand direct response dollars and have done it at a great, great rate.

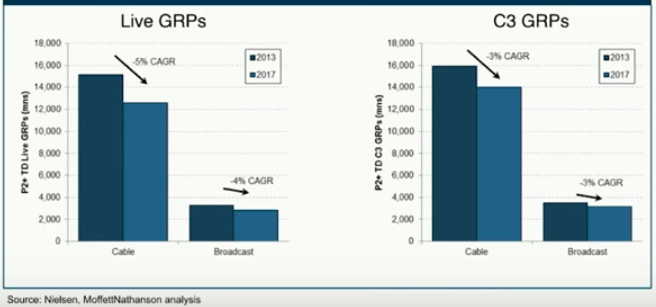

…why you’re getting that soft advertising story in TV is that the ratings just aren’t there.

(the growth of SVOD – Amazon, Netflix, Hulu)

So last year Netflix spent $6.3bn on their P&L buying content, mostly television. Their going to move to film, they’re making 80 films this year. When you look at their P&L this year, it’s $7bn-$8bn of content spending, on a cash basis it’s $10bn-$12bn of content spending. When you line that up with the biggest conglomerates, it’s quickly passing Time Warner, it’s bigger than Fox. They’re reaching a size of investment spending that really challenges linear scripted networks. Now when I back off sports, you could argue that their spending on content’s actually bigger than everyone else but NBCU in 2018.

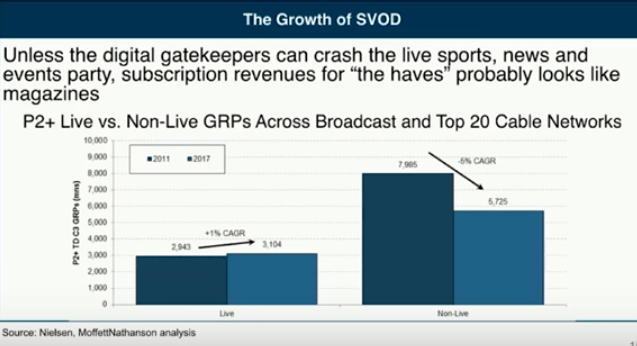

The viewing of live content over the last 7 years (below) has essentially been flat. On the flip side, the viewing of non-live content is down by a CAGR of 5% and that’s accelerating in 2017.

The only products out there that are capturing a high percentage of Americans in one fell swoop is live sports. Our view is that the only advertising play that’s going to be valuable long-term is this live reach of live sports…having this type of unduplicated live reach is why the dollars have not come out of TV yet.

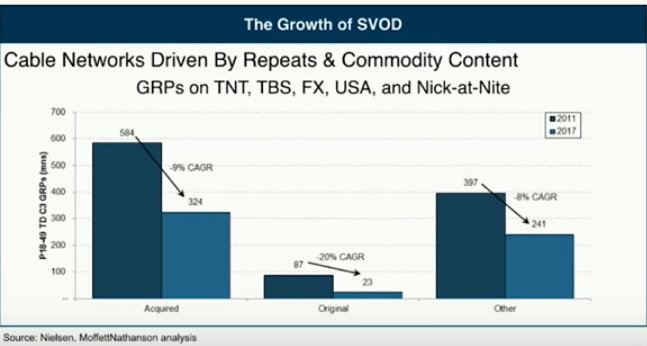

Cable networks driven by repeats and commodity content are in trouble (TNT, TBS, FX, USA, and Nick-at-Nite)…at some point networks that are built on repeat content are going to see big erosion and in fact, that’s what’s happened.

(virtual MVPDs and escalation of affiliate fees)

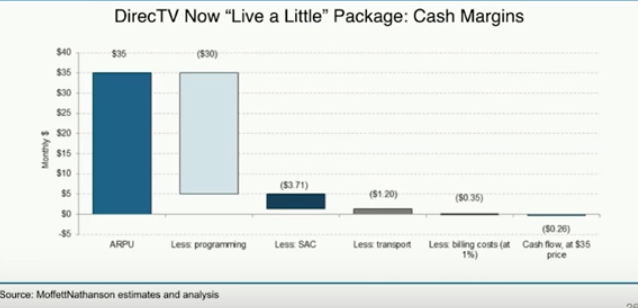

The only problem we see is this…when we do the math on skinny bundles – sports and news stripped down to $35-$40 – our math says there’s no profit there. So you’re getting this profitless growth on the distribution side…

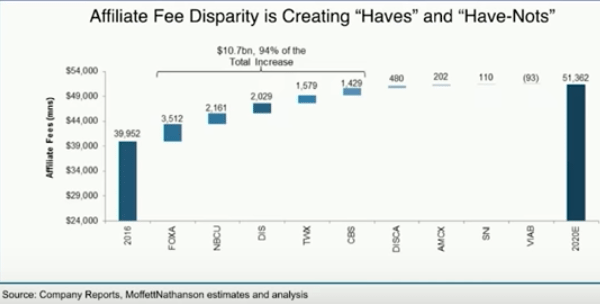

…now making it worse in the future is that the networks they’ve chosen to be the bedrock of those virtual services – Fox, NBC, Disney, Time Warner, CBS – is pretty much where all the growth in that affiliate fee bucket is…the growth rate for their affiliate fees is 9% in aggregate. If you’re a virtual network, you have a $35 price point, but your cost of goods sold is going to be inflating at a very, very high rate, so at some point you have to decide whether you raise your pricing, which could limit your growth or you absorb it as a loss leading product.

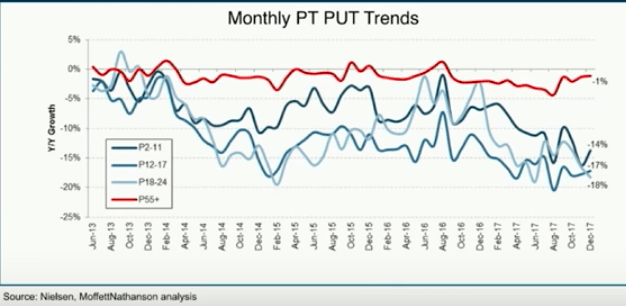

PUT – People Using TV. “Did you use TV today”. If you’ve got a network built on 55+, you’re not seeing the same level of decay as these younger networks.

(Film)

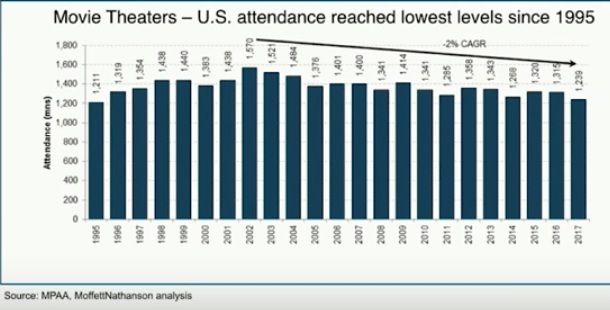

Not a surprise that the physical bit of video has fallen from $16bn to $6bn…but what I’m here to tell you is the growth of the digital format – electronic sell-through, video on demand – is starting to slow. We once thought that could add back the decline of physical. It’s not happening. The bulk of [the physical DVDs] that are bought are from Target, Wal Mart, Best Buy, and it’s just a matter of years before those companies start downsizing their carrying of physical product. So we’re very very worried about the back-end monetization of the film business. And that’s going to lead to more premium VoD….2017 was the worst box office year we’ve seen since 1995 and as Netflix spends more money to make better and better movies, as premium VoD windows start opening up, we see pressure on the theatrical side of the business.

In the short run what you’re seeing is consolidation at a rapid pace. Fox-Disney happened out of nowhere. Time Warner-ATT out of nowhere. Scripps-Discovery, quickly…people are trying to find cost synergies, scale against distributors, trying to find some ways to the consumer with enough library of content.

Blockchain Innovation (10/20/17; How RedHat is Quietly Transforming Enterprise Blockchain with Rich Feldmann)

Rich Feldmann

“So, first on Red Hat. Red Hat is the worldwide leader in open source technology for the enterprise and a lot of the early block chain start-ups were…forming their own open source community projects to develop a distributed ledger either for the cryptocurrency side or for use in the enterprise. So, we got a lot of invitations to come and have conversations with ‘how can Red Hat help me form a sustaining open source community effort and then once I do, can you help me with governance and licensing’. These are all areas that Red Hat was founded on, so it was a natural. So, for about 6 to 8 quarters, those were the nature of the conversations that we had.

Roll forward to today, we have an in-market offering that we call Blockchain-as-a-service that builds on some of the other capabilities that are already in market…blockchain has board level attention at Red Hat and we are putting resources behind it.

What Red Hat’s interest in the blockchain space is distributed ledger use cases for the enterprise. We’re not investing a whole lot of time and energy in cryptocurrency side…so you made mention of the consortiums, Hyperledger (150+ members) and Ethereum Alliance (over 200 members), there’s a few others like Dockchain in the healthcare space, there’s similar ones that are being spun up in Europe and Asia, and I would say virtually all have come to Red Hat and said…’would you be interested in running a support model around my distributed ledger’…while Red Hat sees this as a strategically important initiative, at the current time we don’t have plans to release a Red Hat Enterprise blockchain.

What…are the challenges to getting blockchain or distributed ledgers more broadly accepted, the consortium efforts are a wonderful one and we are members of the Hyperledger consortium, we’re looking at the Ethereum Alliance, but in order [to get] broad based acceptance, eventually we believe that somebody’s going to need to step up and provide a governance model and support model. That’s not Red Hat today. What we do believe is that any distributed ledger…all need to run on a supported enterprise infrastructure, so that’s a supported operating system, being deployed in a cloud or hybrid environment….so what we announced about 6 months ago was a hybrid cloud offering called blockchain-as-a-service with our good partner BlockApps.

If Red Hat’s strategy is not to release Red Hat Enterprise blockchain, what is Red Hat’s strategy? It’s really about providing an enterprise ready platform for you to run your distributed ledger application on…So what we announced, which is something that Microsoft had previously announced with BlockApps, the worldwide leader of what’s known as Blockchain as a service, it’s a way to quickstart a PoC, in a 6 to 12 week project you can spin up your use case, develop it on an application, develop a set of APIs, and develop a small, working application. What Red Hat has done is taken from just a PoC capability to an enterprise ready capability by integrating it with our PaaS offering, which is called OpenShift, so that when clients get ready to go from PoC to production systems, they’re already deployed on those enterprise ready systems […]

Probably smart contracts are the ‘X’ factor, the killer app in distributed ledgers for the enterprise, and smart contracts are now being integrated, they’re a core part of the Ethereum stack and they’re now being integrated into Hyperledger as well, and some of the other distributed ledgers for the enterprise. From an infrastructure perspective, that’s the killer app. What is the killer app from a use case perspective, I don’t think there’s one…

Where we find success is deploying distributed ledger technology behind the firewall that doesn’t require 500 parties to agree on a technology standard…let’s do something like think about a large financial institution that does a general ledger consolidation, and all the steps in the process that occur along the line, whether you’re a subsidiary or a branch of a bank, you’ve got to consolidate your financial statements over say 500 or 5,000 different entities…Now today, with the OCC and everyone that’s looking over your shoulder, you’ve got to report who made changes to that data all along the line. So, that kind of process, completely behind the firewall, under the control of financial institution, is something that lends itself very well to a blockchain or distributed ledger system […]

I’m talking to many large and small systems integrators, large and small ISVs that want to develop applications that will sit on top of a distributed ledger technology. My view is that in the fullness of time, what is a distributed ledger? It’s a database, it’s a data store where some component of the data, ownership, rights pass from one node to another.”

Executive Roundtable: Street Talk (11/9/17), Phocuswright Conference

Rachael Rothman, Sr. Analyst, Gaming, Lodging, and Leisure at Susquehanna Financial Group

(on hotel demand)

“I think we know from the industry-wide data that there is a definite shift to book direct…I would also just highlight that going back 30 years from hotel school, we always thought of brands as occupancy insurance and now that we’re getting 92 months into the recovery, I think you’re going to see that brand power come back into effect, and you’ve seen some of the hotel owners that have moved away from branded product and that relied on things like Expedia and Priceline actually suffer and underperform. And so I think it’s being proven out to the owners and to the operators that the brands actually are working and scale is working. Occupancies are at all time highs in the hotel industry, my stocks are at all time highs, and there are no signs [of] waning demand…there’s not a ton of pricing power but it isn’t a demand issue.”

(on hotels possibly filling the OTA gap on meta spend)

“They are unlikely to step in to fill that gap. I think historically that has not necessarily been a customer that they wanted. I view it as someone who’s pretty brand agnostic and price sensitive. I think what you could see though is some of the bigger brands stepping in with something like Instagram and Facebook and saying ‘hey Rachel, I see that you’re celebrating you’re 10-year wedding anniversary at the Ritz Carlton in Naples…how about next year you go to the Ritz Carlton Dana Point and you book today and we give you 20% off’. They already know I’m a loyal Ritz Carlton customer, they can see that I’m taking photos and interacting…and they can go direct to the customer with a targeted offer.”

(on alternative accommodations)

“First, there is some thought that it takes away pricing power on compression nights. So, that would be if you had SXSW in Austin, TX for example, historically maybe you could have raised your room rate by 30%, now you can only raise it by 10%. But, we also have to consider that Airbnb’s supply is flexible, meaning that people put their capacity on when rates are the highest and I personally am of the belief that Hilton and Marriott and their owners’ balance sheets are built for a recession. When we go into a recession, the Airbnb owners, many of them have extended themselves into having multiple properties and when they find that they can only rent that home for 30 bucks and it’s either $100 or 5 of their own hard labor hours to clean it, you’re going to see a lot of that capacity come off the market and I think it’s going to be the same balance sheet lesson that a lot of individual homeowners learned in the 2008 recession.”

(on loyalty discounts from hotel chains)

“I think it’s working, I think it’s a big deal…Expedia may be able to offer you a free flight or free whatever, what they can’t offer you is 9am check-in, 4pm check-out, free breakfast, unlimited free cocktails, any sort of amenity that any one of these hotel owners or operators can offer to their customers.”

Lloyd Walmsley, Managing Director, UBS

(on OTAs pulling back on meta)

“Priceline has been the most vocal about pulling back and they had spent a lot of money on trivago over the last 2 years and I think trivago was pushing pretty hard and you have a new management team come in and decide to take the strategy a little more aggressively. They had been funding a competitor in search channel so I think it makes eminent sense to try to reset that auction. Priceline has spent some money in TV historically but booking.com’s brand in all of our survey work has still lagged that of peers, so I think it makes sense to be building a brand…I think Google is going to continue to move further and further into the travel vertical and that poses obvious risks if you don’t have a strong brand.”

(on TV spending)

“[TV spending] makes the online spend more efficient. So, Google obviously has a quality score and the higher your click-through rate is the less you pay for ads. Kayak, when they were public, gave us enough disclosure as part of the IPO process that we could see when they started ramping their TV spend, in the first two years after they ramped their TV spend, the cost that they had to pay for their digitally acquired clicks was cut in half. I wouldn’t expect the same magnitude for a brand as big as booking.com but there are secondary benefits to being on TV.”

Eric Sheridan, Managing Director, UBS

(on loyalty discounts from hotel chains)

“Phocuswright put up a lot of their own data saying that loyalty rewards don’t actually drive as much velocity of shopping in travel. We’ve done consumer intention surveys that say similar things. The business market seems like it’s much more driven by loyalty rewards than the consumer marketplace…I would expect over time that the OTAs and maybe Airbnb explore loyalty and rewards.”

(on Amazon, Facebook, Google getting into travel)

“Amazon’s tried a couple times at this more in beta mode and never really gotten much further than that…I think that the inventory is so fragmented on a global scale that in order to achieve scale, I think it would take quite a long time to achieve the scale benefits that Expedia and Priceline have on the inventory side. We’ve always been fairly dismissive of the concept that Google will become an OTA. Google wants more of their partners’ marketing budgets by delivering more qualified leads and delivering more CPCs from it. So, from our view, Google’s always wanted to own more top-funnel than the actual bottom part of the funnel.”

Joint Interview with Expedia guys (Phocuswright Europe, 5/22/17), Phocuswright Conference

(on providing technology for hotels and being a “platform company”)

“The idea is pretty simple. We’ve proven that we can take the platform from our brand and power other brands very effectively in the OTA space and now the idea is to take the same platform and leverage it for hotel partners and allow them to access all the benefits of that technology…and the thinking is if we are improving the customer experience regardless of where the customer wants to book, be it on Expedia or hotels.com or on brand.com…that translates into more disposable income spent on travel. It should be good for the industry and if we power all these parts of the ecosystem, we’ll get a share of the revenue…hotels have needs for pricing, they need data to price correctly. We provide them access with competitive data, market demand, etc. so they can do their pricing, it can be a chain or individual hotel, we can provide data that a small hotel would not have access to to optimize their pricing.

Then, after they’ve done their pricing, they need to attract consumers to their website…we launched a product that allows them to spend their marketing to attract consumers from Expedia and hotels.com directly to their website, which was unthinkable a few years ago…and then the next step is powering their website to make it more effective and increase their conversion. We’re doing this with Marriott on vacations and Vacations by Marriott has grown tremendously…then after that you get to the guest experience, we’ve invested in a company called Alice in which we have a minority share which optimizes hotel operations. We also allow hotels to sign up more loyalty members…we did a test with Red Lion. Then we provide real time feedback to increase the customer satisfaction by treating problems that arise on property before customers write a review later on.”

Booking.com Executive Interview – Phocuswright India 2017 (3/13/17), Phocuswright Conference

Oliver Hua, Managing Director, APAC, Booking.com

“Three years ago we had less than 3,000 hotel partners in India. Now, today we have over 20,000. And the number of room nights per partner remains roughly steady…it’s pretty significant but we’re still in early stages of growth. We’re seeing high double-digit growth for multiple years now and we expect that to continue.

Our strategy in China is two-fold. We develop our own business, China is a major source market for us. The majority of APAC destinations – Japan, Korea, Thailand – are quite dependent on Chinese inbound. We have nearly a thousand people working in our call center in Shanghai. Then the second prong of our strategy is the partnership we have with Ctrip that evolved from a commercial partnership where they were a distribution partner for us into an equity partnership in which we invested pretty heavily into the company in 2014 and 2015…Ctrip has been leading industry consolidation in China, they’ve been rolling out new product and services…and the fact that they’re gaining share in the market is helping us as well because through them we just get a larger audience for our inventory. Our relationship with agoda, our sister company, is very similar to how we work with Ctrip in China. They are two separate brands that operate completely independently of each other.”

(on the long tail of properties)

“In Japan, it’s a well known fact that we have a situation where the market is essentially undersupplied from a traditional hotel accommodation perspective, and then you have a lot of long-tail properties that’s unoccupied because of the shrinking population. The demographic change and migration to large cities…you have a lot of apartments, short-term rentals that’s available for rent and that’s a market we’re definitely very much committed to. We actually have plenty of that type of inventory that’s available on our site for instant booking and immediate confirmation. That’s how we differentiate from other offerings. When you come to booking.com and you book a long-tail property, the customer experience is exactly the same as booking a traditional global chain hotel.”

a16z Podcast (10/28/17; B2B2C Business Models — Trick or Treat?)

Martin Casado

“One of the biggest mistakes I see is ‘listen, we’re working with system integrators, we’re working with MSPs [managed service providers] because they somehow think that’s going to give them reach to a bunch of customers, basically it never pans out…in mature markets it sometimes pans out, but in pre-chasm markets, I don’t think it ever does. [Pre-chasm meaning] there’s no market category, there’s no budget, the customer isn’t educated about what you’re doing. And the reason it doesn’t work out is because…a lot of the enterprise actually purchases from a reseller, not from the vendor directly…and the thing is [resellers] don’t have the salesforce to carry pre-chasm products. They’re good at distributing things where there’s a known budget, but if you’re doing something fundamentally new, there’s no way that a VAR can pitch, educate the customer, and so forth, so normally you have to create a pull-based market before you can actually engage partners.

In the enterprise, the two ends are the vendor, which creates the technology, and the customer, which consumes the technology. In a direct sales model, the vendor creates a sales team and the sales team shows up to the customer and manages that customer. So, let’s say you create a widget in a mature market, so the customer doesn’t have to be educated. And you’re able to get a general partner to sell it. One of the big problems is you don’t have a relationship with the customer. So much of enterprise dynamics come from renewals, expansions, and upsells. Often hyperlinearity in growth comes from expansions, so you actually have to have a relationship with the customer in order to do that. And so going that route is fraught with peril for startups. You are not the one that is actually bringing the product to the end customer…you don’t know what they want, you don’t know what they need, and you won’t have the leverage point to expand that sale […]

The biggest jump in operational complexity a start-up will ever do is when it goes from one product to two products. So, if you do introduce a second product, if you can align it with the same constituency, the same buyer, that’s the best…a natural response of start-ups of not having product/market fit is building another product, which I think is probably the worst thing you can do.

Over time, R&D pencils out as almost a fixed cost or super sublinear but sales scales linearly with people on the ground, so if you hire more sales people, they’re very expensive but to get more dollars you need more sales people. So, there’s this dream that you can have somebody else bare that cost for you…the problem is that the channel doesn’t have the salesforce to push what you’re doing…the lifecycle that normally works is the startup tries that, figures out that it doesn’t work, but maintains relationships with these channel providers. Start-up then builds a direct salesforce and creates awareness in the market and starts to sell it. Once you’ve started to sell it, you’ve actually created now a market and the market isn’t a product market but a market of services around your product. So I sell something to the enterprise just to do a proof-of-product, requires some implementation, and often companies will pay for that, and then after you’ve sold it, that requires professional services along with it. Once you’ve sold enough gear, those markets arise and now you have something you can incent a channel partner with….so now you actually have a market to incent them to invest in training, to get a relationship with the customer, etc.

It’s incumbent on the startup to create the market and once you’ve created the market, you have sufficient leverage to turn on the channel.”

Alex Rampell

“The other challenge with B2B2C is that if your C at the end is coming from the B in the model, then the two business models endanger one another. There’s a company called Yodlee, it’s been around for around 20 years, it’s a key part of the ecosystem for every fintech company that gets data from banks. So if you ever go to E-Trade and it says ‘log into your Bank of America account to wire funds’, that’s going through Yodlee. It turns out they get all of that information in aggregate and they have a different business model which is they sell anonymized aggregated information that they’re collecting from everybody, all the businesses they are working with Yodlee. If they do that too aggressively, it puts them at odds with their core, main business…you can go from being a symbiote [with your middle B] to a parasite or even an antagonist if you start doing things that are competitive with what they’re doing or hurt their primary business model.”

(when B2B2C works)

“I think Rakuten is a good example of this because if you are a bread merchant and there’s another meat merchant you can work with and you realize the meat merchant sells more meat and the bread merchant sells more bread if there’s one communal shopping mall for them all to work with, they don’t want the consumer to sign up directly, they want the consumer to sign up in that shopping mall. That’s highly symbiotic…there it’s Rakuten getting the end consumer, but those two intermediate merchants have an incentive for Rakuten to own that consumer because it makes the whole thing work.”

Podcast Blurbs [Larry Summers, Levered restaurant franchisees, Books vs. podcasts, Cramer on MongoDB]

Freakonomics Radio (9/28/17; Why Larry Summers is the Economist Everyone Hates to Love)

Larry Summers:

(On infrastructure)

“I think we’ve completely mismanaged infrastructure investment in the United States. It’s nuts that when interest rates are lower than they’ve been at any time in the last 50 years that we’re also investing less net of depreciation…it’s nuts that we have a regulatory apparatus that means that it took far longer to repair a single exit of the Oakland Bay Bridge than it did to build the entire Oakland Bay Bridge two generations ago. There’s a small bridge across the Charles River that I’m looking at outside my office. It’s about 300 feet long. It was under repair with a lane of traffic closed for 5 years. Julius Caesar built a bridge over the span of the Rhine that was 9x as long in 9 days. So, both on the quantity of expenditure and on the efficiency of the expenditure and the streamlining of the effort, there’s plenty of room for improvement.”

(On tax repatriation)

“We have $2.5 sitting abroad. Indulge me if you will in an analogy. Suppose you ran a library. Suppose you had a lot of overdue books from your library. You might decide to give the library amnesty so that people would bring the books home. You might decide to say that there will never be an amnesty and people better bring the books back because otherwise the fines are going to mount. But only an idiot would put a sign on the library door saying ‘No amnesty now, thinking about one next month.’ And yet, what have we done as a country? We’ve said to all those businesses with $2.5tn abroad that if you bring it home right now, you’ll have to pay 35% tax, but we’re talking about and thinking about and planning maybe we’ll have some kind of tax reform where that will come down.”

(On cost disease)

“…the Consumer Price Index for all products are set to be 100 in 1983. Well, if you look at the CPI for television sets, it’s now about 6. If you look at the CPI for a day in the hospital room or a year in a college, it’s about 600. In other words, since 1983, the relative price of this relative measure of education and healthcare as opposed to the TV set has changed by a factor of 100. That’s got a number of consequences. One is, since government is more involved in buying education and healthcare than it is in buying TVs, there’s going to be upward pressure on the size of government relative to the rest of the economy. Another is because there’s been far greater productivity growth in the production of TV sets than in the production of government goods, a larger fraction of the workforce is going to find itself working in the areas where there’s less productivity growth, like education and healthcare…if workers become much more productive doing some things and their wage has to be the same in all sectors, then there’s going to be a tendency for the price in the areas in which labor is not becoming productive, to rise. And that’s why it costs more to go to the theater relative to when I was a child, that’s why tuition in colleges has risen, that’s why the cost of mental health counseling has risen.”

Grant’s Podcast (10/11/17; Hamburger Helper)

John Hamburger (President of the Restaurant Finance Monitor):

“I’ve been following franchisees since the early ’80s, I actually was a franchisee back in the early ’80s. Restaurants used to get financed one by one, unit by unit, and you’d buy the land, you’d buy the building, you’d equip it, and you had to finance each of those transactions so you’d have a real estate loan and you’d have an equipment loan. And it took a long time and it was expensive and you thought really carefully about building restaurants. Today, the way the deal works is that there is a huge net lease market out there that likes to own restaurant real estate. So, franchisees over the last 5 to 10 years have decided that they can build more stores, own more stores, buy more stores if they don’t have their capital tied up in real estate. So franchisees, just like the franchisors, have adopted this quasi asset light model where the real estate in a lot of these franchise restaurant locations are owned by an investor. And that’s okay, it’s just that when you own real estate, you own it and can borrow against it. When you lease real estate, the rents go up every year and so over time, it cuts down on the operating margins of the franchisees.

What does it all mean? It’s allowed franchisees to get bigger. So you look at Yum Brands or Burger King, they’re relying on fewer and fewer franchisees to operate their system and where risk might possibly come in is that you’ve got fewer and fewer franchisees operating these restaurant around these countries. I’ve heard Restaurant Brands tell Burger King they’d like to have as few as 50 franchisees in the country. Well, you take 50 franchisees, you lever them up, it’s not like it was 10-20 years ago where in Burger King you had 600 franchisees and the majority of them owned their own real estate. It’s a very levered system, the way it’s currently configured. […]

What’s interesting about Carrols (Burger King franchisee), it’s a typical franchisee in the restaurant space, it’s a larger franchisee, it’s ranked around #4 in the country in terms of size, they’re doing a lot of what the large franchisees have done over the last 5 years. They’ve been able to borrow, they’ve been able to acquire other franchisees and build up their base of restaurants…but other franchisees have grown as well by buying up other franchise restaurants…how do they do that? They borrow and then they sell their real estate and lease it back, that’s how all of this stuff gets financed and it adds a lot of leverage to the franchisees.

The largest owner of [this real estate] are a number of REITs focused on the restaurant business, there’s Realty Income, there’s Spirit Realty. There’s also individuals, real estate developers, trusts, and one of the reasons they like owning this kind of real estate generally these leases are triple net, which means taxes, maintenance, and the insurance of those properties are taken care of by the tenant, so the rental income becomes an annuity to the owner, and this is a huge investment area in the US.

If I go back to the ’80s and ’90s, capital in the restaurant business came from the public markets. We had a run of IPOs in the 1980s and 1990s, that’s where most of the growth capital came from. Today, you have private equity funds instead of public investors driving the restaurant business. The public markets have changed where smaller companies…have been unable to go public. I think the last IPO in the restaurant business was 2015.”

Waking Up (10/6/17; The “After On” Interview)

Sam Harris:

“The numbers [of people who listen to the Waking Up podcast] are really surprising and don’t argue for the health of books, frankly. A very successful book in hard cover, you are generally very happy to sell 100,000 books in hard cover over the course of the first year before it goes to paperback. That is very likely going to hit the best-seller list, maybe if you’re a diet book you need to sell more than that, but if you sold 10,000 your first week, you almost certainly have a best seller. And in the best case, you could sell 200,000 or 300,000 books in hardcover, and that’s a newsworthy achievement. And there’s the 1/100th of 1% that sell millions of copies. So, with a book I could reasonably expect to reach 100,000 people in a year and maybe some hundreds of thousands over the course of a decade. So, all my books together now have sold, I’m pretty sure I haven’t reached 2 million people with those books. Somewhere between 1 million and 2 million.

But with my podcast, I reach that many people in a day. And these are long form interviews and sometimes standalone, just me talking about what I think is important to talk about for an hour or two, but often I’m speaking with a very smart guest and we can go very deep on any topic we care about. And this is not like going on CNN and speaking for 6 minutes in attempted sound bites and you’re gone. People are really listening in depth. […]

It’s a big commitment to write a book. Once it’s written, you hand it in to your publisher and it takes 11 months for them to publish it. Increasingly, that makes less and less sense. Both the time it takes to do it and the time it takes to publish it don’t compare favorably with podcasting. In defense of writing, there are certain things that are best done in written form. Nothing I said has really application to [novels], reading novels is still an experience you want to have, but what I’m doing in non-fiction, that’s primarily argument driven, there are other formats through which to get the argument out. I still plan to write books because I still love to read books and taking the time to really say something as well as you can effects everything else you do, it effects the stuff you can say extemporaneously in a conversation such as this as well. So, I still value the process of writing and taking the time to think carefully about things.”

Mad Money w/ Jim Cramer (10/25/17)

Jim Cramer:

“At the heart of every software application there’s a database. You need to have a system to organize, store, and process your files or none of this stuff works. So, for software developers, a lot of thought goes into picking the right database and with the rise mobile, social, cloud, datacenter, and IoT, a lot hinges on getting that choice right. For the longest time, there were just two types. You had relational databases that are basically unchanged since the 1970s, so developers need to spend a lot of time making sure modern software interacts properly with these rigid database structures from decades ago. They simply were not designed for the demands of modern software and they certainly weren’t designed for cloud.

Since the turn of the century, though, we’ve seen the rise of non-relational databases which tried to address these shortcomings. But the problem is that so much runs on old school relational databases, these new non-relational ones are only worth using in a small number of cases. Then you have non-relational databases that have become more popular recently and are widely used for big data and online applications…basically, they’re more flexible than the traditional model.

On the other hand, MongoDB does something different. The guys who created this company got frustrated by the available database options on the market, so they built their own platforms designed for developers by developers. The company has its own offering that they believe combines the best of both relational and non-relational databases. They use a document-based architecture that’s more flexible, easier to scale, more reliable, giving developers the ability to manage their data in a more natural way so they can more rapidly build, deploy, and maintain the software they’re working on. It works in any environment – the cloud, on premise, or even as some kind of hybrid which has become so popular – but more important, you can use it for a broad range of applications.

To get the word out, MongoDB offers a free, stripped down version of their database platform. You can just download it right off the website. That makes it easier for software developers to play around with the thing, if they decide they want advanced features, they can pay for any upgrade…The free version has been downloaded more than 10mn times just in the last year. Then they sign you up for a subscription and you start paying for the enterprise version or the cloud-based version. So far, MongoDB has more than 4,300 customers in 85 countries including some really well-known names, they’ve got Barclays, ADP, Morgan Stanley, Astrazenca, Genentech, and bunch of government agencies […]

How’s it work? Let’s use the example of Barclays. Like most financials, Barclays has invested a ton of money going digital in recent years. But the rigid nature of old school database technology made it really hard for them to add new online features that customers could use. And as more customers embrace mobile banking, the cost of running the mainframe kept rising, so Barclays brought in MongoDB in 2012 and it gave them significant performance improvements and a resilient system and major cost savings and the company’s in-house software developers have a much easier time developing features for digital banking.

How about the numbers? Well, MongoDB’s revenue growth has slowed a tad so far in 2017 but it’s still very rapid, up 51% y/y and that’s not much a deceleration from 55% in 2016. The customer base is growing like a weed. At the end of July, they had 4,300 customers, up from 3,200 in January and 1,700 at the beginning of 2016. And a total of 1,900 of these users come from MongoDB’s cloud offering even though it only came out in the summer of last year. The company has 71% gross margins, which have improved steadily over the last couple of years. But like many newly minted tech IPOs, MongoDB is not yet profitable…the key here is annual recurring revenue (ARR) because remember they use a SaaS business model and then the contribution margin…in 2015, customers who signed up that year generated $11.5mn in ARR but they racked up $24.3mn in associated costs, meaning the contribution margin was negative. By 2016 though, that same group of customers who signed up in 2015 generated $12.8mn in RR but costs only came in at $5.2mn, makes sense these guys had already been signed up, giving MDB a 59% contribution margin. 2017, it’s risen to 60%. Basically, as time goes on, customers become more and more lucrative because the real expense is signing them up.

Now there’s really just one thing that concerns me other than lack of profitability. Mongo competes with some real titans of the industry, I’m talking IBM, Microsoft, Oracle, AWS, Google Cloud, Azure for more modern databases.

Podcast Blurbs [Freewill, Jerks, Cramer on Switch]

“Companies started coming to [The Guinness Book of World Records] asking if we could fly someone out to their event. Companies and people were coming to Guinness wanting to break a record for publicity or to draw attention to themselves. They’ve gotten on to the fact that if they achieve a record title, they get a lot of press for it or shares on social media. Increasingly, they want to make it more of a marketing event, they want to invite one of our adjudicators and the usage of the logo. Guinness realized that they could charge for this, a lot. The price tag for a full service event starts at $12,000 and goes up over half a million…they do hundreds of events like this every year. […]

Guinness’ main customers used to be kids who were just fascinated by the people who were breaking the records and pushing the limits of what it meant to be a human. Guinness’ customers now are the record breakers themselves. If you pay Guinness enough money, they will help you figure out a record you can break and they will help you break it….Guinness is now in the business of selling record-breaking events.”

Mad Money w/ Jim Cramer (10/6/17)

Jim Cramer on Switch:

“As technology gets better and better we’ve seen a ridiculous explosion in the amount of digital information out there. Companies that want to know what’s going on need to keep track of tons of data. By some estimates, there are going to be 200bn smart devices connected to the web by 2020. Even now, the average person generates 3GB of data per day. We use the internet for everything and increasingly store data in the cloud, which means some datacenter somewhere is where it goes.

Your typical datacenter is just a gigantic building, it’s packed with networks, servers, and air conditioning equipment…but Switch is different. According to them, the kind of datacenter you need to run a low cost consumer service like Apple Music is just not the same as the kind of datacenters that work best for business critical data storage or highly complex work loads with highly sensitive and regulated information. Switch has actually patented their datacenter design, the layout and cooling systems allow customer to run more power through their machines. On top of that, Switch’s platform makes it easy for clients to rapidly deploy or replace technology infrastructure.

Switch’s revenue grew at a 17% clip in 1h17 and while that’s a bit of a deceleration from last year’s growth rate of 20%, it’s still pretty darn good. These numbers can jump around whenever Switch opens new datacenters. The key here is that 90% of their revenue is recurring. Switch’s gross margin came in at a rock solid 48.2% in the first half…Switch is actually, yes, profitable here. And while its operating margin jumps around a lot because of one-time fees, the fact is that it’s a pretty good business.

However…there are some issues we need to address. For starters, it’s got a complicated corporate structure. Before the IPO, Switch operated as a partnership. […] The partnership has now established a standard C-Corp including a holding company, Switch Inc., which is the stock that is now trading. Switch Ltd, the partnership, is now the sole asset of Switch Inc., which is a little troubling…The founder, Rob Roy, now has 67.7% of the voting power in Switch Inc. Public shareholders have less than 5%. It’s never a good thing when you have a multi-tiered ownership structure with the owners of the common stock being treated as second or third class citizens. It’s rarely a good thing when the people who own the asset are different from the people who control it…For example, because of Switch’s transformation, the insiders who used to own the whole thing are racking up some major tax bills, so Switch is helping to pay those taxes for them.

What else is problematic? The vast bulk of Switch’s sales, more than 95%, come from a single datacenter campus in Las Vegas…on top of that, Switch gets 38% of its sales from just 10 companies. Ebay alone accounts for nearly 10%. But the datacenter business tends to be pretty sticky. I’m not that concerned.

In 1h17, Switch generated $35.3mn in net income. To be conservative, let’s just double that for the fully 2017. So Switch is likely to make $70.6mn. But at $70.6mn, Switch will be growing at a 20.9% clip vs. last year’s numbers when you subtract one-timers…let’s assume that growth rate decelerates to 15% next year. With $81.1mn in net income divided by the share count and I’m estimating that Switch could earn 28c per share this year, 32c next year…that means it’s selling for 76x earnings and 66x next year’s numbers. Obviously that’s expensive. However, I think I’m low-balling…next year, Switch will start selling datacenter space at its new center in Atlanta and remember every time they’ve opened a new datacenter, their sales have immediately surged higher. It’s like a staircase. But even if Switch has an earnings explosion next year, it might be too expensive for me. Nvidia trades at less than 50x next year’s earnings. But Nvidia’s earnings are growing at a 41% clip.

On the other hand, Switch is the only pure play on the growth of datacenters out there. CoreSite, Equinix, Digital Realty are all REITs, which means they need to distribute all their income back to investors. In other words, they can’t invest as heavily in growth. That means Switch has scarcity value.”

Waking Up, Ep. #27 (Ask Me Anything)

Sam Harris:

“The distinction between voluntary and involuntary action is an important one. But it’s not one that requires a belief in free will to describe. There are things we do based on intentions that align with our goals and desires and consciously held purposes. And there are things that we do automatically or by accident. When looking at even my most voluntary behavior, I see no evidence of free will.

Let’s say you’re deciding whether to marry your boyfriend or not, it doesn’t matter how long you think about that. This could be the most deliberative decision of your life. What finally swings the balance between ‘yes’ and ‘no’ is in principle mysterious, subjectively, and is arising out of causes and conditions that you did not create. If you love this man’s smile, you didn’t create your love for it. You love it precisely to the degree that you do, you didn’t create his smile in the first place, you didn’t create it’s effect on you, you didn’t create that this is something you care about. And so it is with everything else that you like or dislike about this person. Your association with marriage, how important it is to you, how idealistic you are about it, how urgently you feel you have to enter into it, the advice you get from friends and family and its effect on you…all these dials are getting tuned by forces you can’t see, did not engineer, and cannot control. And even your moments of apparent control, well that just arises out of background causes that you can’t inspect and which are moving you to the precise degree that they are for reasons that are inscrutable.”

Very Bad Wizards, Ep. #77 (On the Moral Nature of Nazis, Jerks, and Ethicists)

Eric Schwitzgebel:

“In my view, a jerk is somone who culpably fails to appreciate the perspectives of other people around them, treating those people as tools to be manipulated or fools to be dealt with rather than moral and epistemic peers…it’s a kind or moral ignorance and epistemic ignorance. So you’re ignorant of what you owe to those people and you’re ignorant of what those people, when they differ from you in their opinions, what kind of validity they might have in their perspective that’s contrary to yours…I wanted to make it ‘culpable’ ignorance because I didn’t want it to be the case that babies are jerks.”

Podcast Blurbs [Small cap investing, Ackman on ADP, Cramer on Dexcom, Journalism]

“Back [when I started my career], the largest holders of these small cap stocks were traditional small cap value managers like the Royce Funds, Heartland, Gabelli, and when prices got out of whack, they were there to police the market almost like a market maker. But now when I look at the top holders, I see Vanguard, Dimensional, Blackrock. They are price insensitive investors…this is what’s going to be a significant contributor to small cap opportunities in the future.”

“Cycles vary between industries and businesses, so you got to be careful not to use a standard 5 to 10 year [when normalizing profits]. The Schiller P/E is 10 years. Well, 10 years could include 2 upcycles and 1 downcycle, so you’re not really normalizing. Or it could include 2 down and 1 up. I like to customize my normalization to the particular business or industry.”

“1993 to 2000, for most of that cycle, everything I touched turned to gold, it was unbelievable. 1993 to 1998, I mean I had just graduated from college, I was running trust money, $300mn, I couldn’t believe they had given me all this money to run and I was doing well. And then in 1996, I joined Evergreen Funds as a small cap value manager and the trend continued. […] It was the profit cycle and I had no idea. I was a young analyst and I thought I was a genius. But then of course the tech bubble hit and ‘wow’ that was a humbling experience, where I went from the genius to the idiot. That was a very difficult cycle. I’m most proud of 1999 because I lost 8%, I don’t know if you tried you could lose 8% in 1999 but somehow I did it because I ignored tech.

Bill Miller is right in that where you start can influence how you perceive yourself and how others perceive you. You think about the average age of an analyst or manager now, I would guess it’s 8-10 years maybe? And what’s the length of the cycle, 9 years? So it’s interesting, lots of the investors now running billions and billions, they’re in the same position I was in in the ’90s when I thought I could do no wrong and I was bullet proof. And that’s kind of scary. […] The losses that could occur in this cycle with where valuations are? If you just revert to normal valuations, you could lose half your capital in small caps.”

“Mutual Fund cash levels are at 3%. Meanwhile, there’s a survey that showed that 80%+ of portfolio managers believe stocks are as expensive as 2000. So, you have a huge conflict here…so, if they think stocks are overvalued and they start losing 10%-30% of their clients’ capital, I don’t know how they’re going to respond. I think because they know stocks are expensive, they’re going to be quicker to sell.”

“It’s been so long since we had a panic that when it does happen, it’s going to be so new to so many people, even people who are experienced, they haven’t seen it in so long. […] Everyone thinks they’ll be the first one out when the cycle ends, but if you’re running a billion of small cap money and the Russell 2000 drops 30%, I have news for you. You’re not getting out.”

“Another way I screen for stocks is I do role playing, where I’m trying to pretend I’m a relative return manager with a really big house, country club membership, etc. and running $1bn+ and then I think to myself, all right, I’ve got 10 very large consultant meetings next week – what do I not want to talk about? That is usually one of the best ways to be a contrarian. And right now where would you look? I would think you’re approaching the year-end performance panic…I think you might want to start looking at energy and retail. Those might be the two most embarrassing sectors right now for professional managers.”

“A lot of high quality value investors won’t even consider commodity companies because we’re taught in school and in all the great books that they’re bad businesses. But if I can buy natural gas in the ground for a dollar and it costs $2 to find and develop that or if I can buy an ounce of gold in the ground fully developed for $150/ounce and it cost $300/ounce to find and develop that, those are the kinds of things I’m interested in. I view mining businesses more from valuing a balance sheet…I want to buy the reserves for less than it costs to replace them and that has worked very well for me over time. Commodity stocks and other cyclicals are either extremely undervalued or extremely overvalued. […] but they need to have a good balance sheet, this is the key. You need a runway and you need to determine the appropriate runway…Tidewater had $50/share in book value and it went bankrupt.”

Mad Money w/ Jim Cramer (10/4/17)

Bill Ackman on ADP:

“Our new question for ADP is ‘why is it that ADP has lower employee productivity than all of their competitors.’ So, ADP generates $160k revenue per employee; the competitors average $224k. When you think about ADP, it has enormous scale vs. competitors, so if anything, they should have more efficiency.”

“25% of ADP competes directly with Paychex. Same size customer. So what we said to ADP was ‘Paychex has 41% pre-tax profit margins. But they’re largely an SMB company. ADP’s SMB segment, if it had the same margins as Paychex, it would mean the rest of their business has margins of 12%. And that makes no sense. So, clearly there’s a big opportunity.”

“We’re the third largest investor in the company by dollars spent. We’ve got a $2.3bn investment in the company and we own almost 9mn shares in the company so our interests are very much aligned with the other owners of the company. Look at all the directors on the Board. Our candidates haven’t even joined the Board yet [and they’ve] spent more money to buy ADP common stock for themselves than the entire Board has spent in the last 14 years.”

Jim Cramer on Dexcom

“We’ve talked about the benefits of Dexcom’s technology before, but in the last couple years the stock’s begun to stall. Then, last week the darn thing fell out of the sky, plummeting more than 30% in a single session…Dexcom’s problem is pretty straightforward. A week ago, we learned that Abbott Labs had received FDA approval for its new FreeStyle Libre Flash Glucose Monitoring System for people with both Type 1 and Type 2 Diabetes…In the old days, if you wanted to check your blood sugar levels, you had to prick yourself and draw blood with one of those finger sticks. With Dexcom’s system, you just wear a little sensor and get readings, but you still need to prick your finger twice a day to calibrate the machine. Abbott’s new system requires zero finger stick calibration…plus, you can leave Abbott’s sensor on your arm for 10 days, longer than Dexcom’s current system (although the same as the system the company hopes to launch later this year)…it got hit with substantial price target cuts from 6 different firms, and that’s how a stock goes from $67 to $45 in a single day.”

“First, why was this such a surprise? Wall Street expected that Abbott would have a harder time getting FDA approval or at least that it would take longer than it did. But with earlier than anticipated approval, Abbott has leap frogged Dexcom. Consider that Dexcom’s new system, which isn’t even out yet, still requires that you prick your finger once a day. However, maybe we should have seen this coming. Abbott’s Libre system was approved in Europe 3 years ago, it’s already being used by 350k people there. There aren’t many cases where a product works just fine in Europe but the FDA decides to reject it anyway. And remember, this is the Trump FDA, which means it’s very pro- business and less consumer safety. Second, was Abbott’s pricing strategy. They decided to be far more aggressive than anyone thought. Abbott’s system will cost $4/day, Dexcom’s will set you back between $8 and $10 per day, including the cost of hardware. And this is before any kind of insurance reimbursement for Abbott. Even worse for Dexcom, Abbott told us they already had 5 of the largest pharmacies lined up to sell the thing with distribution planned to start in December. This is brutal. Before Abbott’s system got approval, Dexcom’s system was pretty much the only player.”

“Even if Dexcom doesn’t lose tons of market share to Abbott, they’re going to have to get more promotional to keep that business, which means that the company’s excellent hardware margins are going to come down hard.”

“Dexcom’s product is actually better than Abbott’s…it’s more accurate and more reliable…[based on the] average relevant difference between the measurements from the monitors based on the readings you get from a blood test. Abbott’s system averages a 9.7% differential…Dexcom’s is more like 7.2%, sounds small but if you have diabetes the difference can matter. Plus, Abbott’s system can lead to a lot of false positives. Dexcom’s new system has also been shown to be more accurate than Abbott’s with no finger sticks at all. One reason why Abbott’s system is cheaper is because it takes a much more bare bones approach. One of the great things about Dexcom is that unlike Abbott’s system, their device gives you real time alerts or alarms, so if you fall asleep and your blood sugar gets too low, it’ll wake you up. […] With Dexcom submitting it’s new monitoring system to the FDA in the near future, I think the company might have a chance to turn things around. Plus, they’ve already partnered with Google to develop a cheaper, smaller system that requires no prick finger calibration, that’s expected next year.”

The Ezra Klein Show (David Remnick on journalism in the Trump era and why he hires obsessives)

David Remnick (Editor of the New Yorker)

[In 1998, when Remnick took over as editor, The New Yorker was losing money]. “With The New Yorker, the zenith of advertising was in 1967. The New Yorker, which was invented in 1925, really as an economic thing, just rode a postwar consumerist boom with the developing middle and upper middle class and all those ads. And the reason The New Yorker started publishing 3 part and 4 part series was not only on the literary and journalistic merit but also the need to have editorial matter running next to…this travel agent and that department store, and this started to change. Television became bigger, all these other media. People’s tastes changed. So, the zenith of advertising for The New Yorker was the last ’60s.

And thereafter, there was a rather slow slide down. It wasn’t perceptible. The New Yorker was independent, it was owned by the Fleischmann family and it still made a profit. The Fleischmanns began to care too late, I would say. And the Newhouses bought it, it was kind of on the brink, red and black, and then it was distinctly in the red for a good while. The question was how to change that. And Tina Brown did a lot of great things to arouse interest in the magazine…and advertising continued to go down, no matter what. It was very clear after a while to me, this is before tech even really boomed, that despite the tech advertising bubble and Red Envelope, that 1967 was not going to return. […]

We’re now in a situation where Google and Facebook own 2/3 to 3/4 of web advertising. Retail has changed in this country, there are more options…and there are only two ways to make money in this business. Advertising and what’s gently called consumers, meaning the readers, what they pay. And 25 bucks for 52 issues was crazy…all you’re paying for it is 50c? Less than one issue of the newspaper on the newstand at the time? So the proposition now is that for a subscription, for each week you might pay what you’d pay for a small cappuccino at Starbucks. And I really think that what we turn out on the web every day, what we publish in print and online immediately midnight Monday, is worth that at least. And our readers have agreed and we’ve been making a handsome profit for quite some time.

The happy coincidence is that our readers want what we do when we are at our best. The worst thing I can do, not only as a moral and journalistic proposition, is dumb the magazine down, but it would be the stupidest thing I can do as a business proposition. That’s [not] what our readers want. I don’t need consultants or polls to tell me that.”

“I was always the oldest guy at these early internet dinners or events, and I knew why I was invited, as the kind of editor of a ‘legacy’ media outlet, which of course the glint in the eyes of my younger brothers and sisters, was that I was soon to become like the stegosaurus itself, dead in a ditch. And there were certain truisms I would be hearing: 1) no one would pay for any content because information wants to be free, which was a misapplication of what that phrase meant; 2) nobody would read anything on the internet of any length. That was also an evangelical, hard truism that I was hearing all the time. And I was wrong about a lot of things, but those two things they were wrong about. People will pay for things that are extraordinary. People will read things that are great. It may not be 330mn Americans. […]

I remember once I was interviewing Philip Roth and he was deploring the state of fiction reading audiences. This was before he became, again, a best selling author. So he was in a kind of despairing mode. But to cheer himself up he said, ‘if you write a novel and only 5,000 people buy it and read it, that may seem depressing, but if all 5,000 people streamed through your living room and shook your hand and said “thanks for the 4 evenings that I spent reading this novel”, you would be brought to tears with gratitude.’…Look at the readership of The New Yorker. There’s a million now…1.25mn readers out of a country of 330mn people. But if I imagine them as Yankee Stadiums full of people, that’s a whole lot of people being absorbed in texts that are often enigmatic, complicated, take time to read. I am filled with gratitude.”

“To get a job [at Netflix] and to keep it, you have to accomplish great things. Here’s another slide [from Netflix’s presentation on its principles]…’We are a team, not a family. And we are a Pro sports team, not a kid’s recreational team.’ In other words, if they don’t need you any more or if the business changes, you will be cut. Don’t expect this to be a job for life…and Netflix lives by this philosophy, even in really good times. Like when Netflix started streaming movies and that took off […] Netflix was growing so fast, it was about to break the internet. Streaming online takes up a huge amount of data and Netflix just wasn’t equipped to deal with it if suddenly the entire country started streaming. Executives figured they had less than a year to fix this problem…so the executives decide they’re going to have to hire someone else to solve this problem and they did. They hired Amazon. They used Amazon datacenters and Netflix’s engineers [who made streaming happen in the first place] were not happy…the honest truth was, they were toast, there wasn’t going to be a role there for them.”

JCAP (9/8/17; Constantly Reinventing Yourself)

William Bao Bean (Managing Director of Chinaccelerator talking about Chinese tech companies)

“The end game for [payments in China] is ‘what percentage of the total spending for the entire country, non-enterprise, can I capture?’ And then you apply a fee to that and that’s the revenue opportunity. It’s huge, it’s massive, you cannot underestimate the amount of money that will be flowing through [TenPay and AliPay] because over time, all payment will go through payment platforms. They’re connected to the banks, the government wants to keep an eye on it, but they’re not looking to get in the way. […] So, all consumer spending – from your rent to your bills to buying a car – over time, will go through these platforms. We’ve seen in India something amazing with demonetization. India is going on mobile payments faster than China did…WeChat added 70mn bank accounts in 3 months…but in India, it’s happening even faster.”

“Online advertising [in China] has always been controlled by a small number of players. The large players like Baidu, unfortunately Baidu kind of missed mobile, so it’s down to Tencent and Alibaba. Sina and Sohu are kind of niche, small players at this point and I think Sina’s mostly within the Alibaba camp at this point. The advertising market is basically controlled by two companies. It was not transparent until about 2 years ago when Alibaba and Tencent launched programmatic trading and you saw the average click-through rate for the average Chinese banner go from 2% to 0.15%. Click-through rates were always historically high because they were historically all faked. The market is much more open now. The issue the traditional banner is that with a 0.15% click through rate, it’s just not very effective. So, you’ve see a very quick move to KOLs [Key Opinion Leaders – influencers and bloggers] because it comes down to trust.”

“KOLs are taking from traditional display but traditional display is still huge. Most of Alibaba’s revenue comes from search within the Taobao and Tmall platform and then Baidu has a lot of search revenue [from display]. But more and more money is going into social, native advertising (KOLs), that’s where a lot of the tech investing is going…the one company that continues to do well from the old days is Netease, they have great games and great execution and they’re actually much larger than Sina and Sohu at this point.”

“Social commerce is the norm in China whereas e-commerce is still the norm in the US and Western Europe, so I’d say the US and Western Europe are about 1.5-2 years behind China.”

“Chinese consumers are notorious for switching to new products. Something that’s massively popular one day, 8 months later could be in deep trouble. So you need to constantly be reinventing yourself if you want to stay competitive.”

“The key trend in [online travel] is that Chinese traveling habits have moved very quickly away from group travel…FITs [frequent independent travelers] are now the rule. The market is segmented quite heavily between luxury/independent/backpacker segments. There are many shoppers that use travel as an excuse to go abroad and buy lots of things. Chinese consumers represent 40% of total luxury consumption in the world, but over half of that occurs outside of China. […] many of the low cost trips are actually no-cost trips. The Chinese basically get a free trip to Thailand in return for being made to visit stores.”

“Booking.com has an unfair advantage that they understand online marketing very well globally. They’re very good at spending money efficiently. Unfortunately, the rules that apply globally do not apply to China.”

“There’s 2 ways to make money. There’s entertainment – games and then there’s commerce. Advertising leads to entertainment and to commerce, so we look at advertising as a subset of the other two.”

“Initial Coin Offerings, it’s a classic bubble. Usually you have people investing large amounts of money in products that have few or no users and little or no revenue…ICOs are even worse than that. You’ve got large amounts of money being invested in something where there is no product yet. It’s a white paper. And the product will only be released after they raise the money…so you’re going to have highly capitalized companies that don’t have product/market fit yet, and the value of these coins is based on the value of the platforms or services that they’re building.”